Europaudvalget 2023-24

EUU Alm.del Bilag 214

Offentligt

Contribution ID: f91be203-0635-45f5-b7e2-4f725f5873da

Date: 21/12/2023 14:08:30

Targeted consultation on the implementation

of the Sustainable Finance Disclosures

Regulation (SFDR)

Fields marked with * are mandatory.

Introduction

The

Sustainable Finance Disclosures Regulation (SFDR)

started applying in March 2021 and requires financial market

participants and financial advisers to disclose at entity and product levels how they integrate sustainability risks and

principal adverse impacts in their processes at both entity and product levels. It also introduces additional product

disclosures for sustainable financial products making sustainability claims.

This targeted consultation aims at gathering information from a wide range of stakeholders, including financial

practitioners, non-governmental organisations, national competent authorities, as well as professional and retail

investors, on their experiences with the implementation of the SFDR. The Commission is interested in understanding

how the SFDR has been implemented and any potential shortcomings, including in its interaction with the other parts of

the European framework for sustainable finance, and in exploring possible options to improve the framework.

The main topics to be covered in this questionnaire are:

1. current requirements of the SFDR

2. interaction with other sustainable finance legislation

3. potential changes to the disclosure requirements for financial market participants

4. potential establishment of a categorisation system for financial products

Sections 1 and 2 cover the SFDR as it is today, exploring how the regulation is working in practice and the potential

issues stakeholders might be facing in implementing it. Sections 3 and 4 look to the future, assessing possible options

to address any potential shortcomings. As there are crosslinks between aspects covered in the different sections,

respondents are encouraged to look at the questionnaire in its entirety and adjust their replies accordingly.

Please note that::

we advise you to

save your draft reply regularly

by clicking on the “

Save as draft

” button on the right side of

1

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

we advise you to

save your draft reply regularly

by clicking on the “

Save as draft

” button on the right side of

the screen

some questions of this online questionnaire are displayed only when a specific response is given to a previous

question

in order to ensure a fair and transparent consultation process

only responses received through our online

questionnaire will be taken into account

and included in the report summarising the responses. Should you

have a problem completing this questionnaire or if you require particular assistance, please contact

fisma-

sfdr@ec.europa.eu

More information on

this consultation

the consultation document

the related public consultation

sustainability-related disclosure in the financial services sector

the protection of personal data regime for this consultation

About you

*

Language

of my contribution

Bulgarian

Croatian

Czech

Danish

Dutch

English

Estonian

Finnish

French

German

Greek

Hungarian

Irish

Italian

Latvian

2

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Lithuanian

Maltese

Polish

Portuguese

Romanian

Slovak

Slovenian

Spanish

Swedish

*

I

am giving my contribution as

Academic/research institution

Business association

Company/business

Consumer organisation

EU citizen

Environmental organisation

Non-EU citizen

Non-governmental organisation (NGO)

Public authority

Trade union

Other

*

First

name

Christine

*

Surname

Søby

*

Email

(this won't be published)

chso@ftnet.dk

*

Organisation

name

255 character(s) maximum

The Danish Financial Supervisory Authority (the Danish FSA).

3

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

*

Organisation

size

Micro (1 to 9 employees)

Small (10 to 49 employees)

Medium (50 to 249 employees)

Large (250 or more)

Transparency register number

255 character(s) maximum

Check if your organisation is on the

transparency register

. It's a voluntary database for organisations seeking to

influence EU decision-making.

*

Country

of origin

Djibouti

Dominica

Dominican

Republic

Libya

Liechtenstein

Lithuania

Saint Martin

Saint Pierre and

Miquelon

Saint Vincent

and the

Grenadines

Luxembourg

Macau

Madagascar

Malawi

Malaysia

Maldives

Mali

Malta

Marshall Islands

Martinique

Mauritania

Mauritius

Mayotte

Samoa

San Marino

São Tomé and

Príncipe

Saudi Arabia

Senegal

Serbia

Seychelles

Sierra Leone

Singapore

Sint Maarten

Slovakia

Slovenia

Solomon Islands

Please add your country of origin, or that of your organisation.

Afghanistan

Åland Islands

Albania

Algeria

American Samoa

Andorra

Angola

Anguilla

Antarctica

Antigua and

Barbuda

Argentina

Armenia

Aruba

Australia

Austria

Azerbaijan

Ecuador

Egypt

El Salvador

Equatorial Guinea

Eritrea

Estonia

Eswatini

Ethiopia

Falkland Islands

Faroe Islands

Fiji

Finland

France

4

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Bahamas

Bahrain

Bangladesh

French Guiana

French Polynesia

French Southern

and Antarctic

Lands

Mexico

Micronesia

Moldova

Somalia

South Africa

South Georgia

and the South

Sandwich

Islands

Barbados

Belarus

Belgium

Belize

Benin

Bermuda

Bhutan

Bolivia

Bonaire Saint

Eustatius and

Saba

Bosnia and

Herzegovina

Botswana

Bouvet Island

Brazil

British Indian

Ocean Territory

British Virgin

Islands

Brunei

Bulgaria

Burkina Faso

Burundi

Cambodia

Gabon

Georgia

Germany

Ghana

Gibraltar

Greece

Greenland

Grenada

Guadeloupe

Monaco

Mongolia

Montenegro

Montserrat

Morocco

Mozambique

Myanmar/Burma

Namibia

Nauru

South Korea

South Sudan

Spain

Sri Lanka

Sudan

Suriname

Svalbard and

Jan Mayen

Sweden

Switzerland

Guam

Guatemala

Guernsey

Guinea

Guinea-Bissau

Guyana

Haiti

Heard Island and

McDonald Islands

Honduras

Hong Kong

Hungary

Nepal

Netherlands

New Caledonia

New Zealand

Nicaragua

Niger

Nigeria

Niue

Norfolk Island

Northern

Mariana Islands

North Korea

Syria

Taiwan

Tajikistan

Tanzania

Thailand

The Gambia

Timor-Leste

Togo

Tokelau

Tonga

Trinidad and

Tobago

5

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Cameroon

Canada

Cape Verde

Cayman Islands

Central African

Republic

Chad

Chile

China

Christmas Island

Clipperton

Cocos (Keeling)

Islands

Colombia

Comoros

Congo

Cook Islands

Costa Rica

Côte d’Ivoire

Croatia

Cuba

Curaçao

Cyprus

Czechia

Iceland

India

Indonesia

Iran

Iraq

Ireland

Isle of Man

Israel

Italy

Jamaica

Japan

North Macedonia

Norway

Oman

Pakistan

Palau

Palestine

Panama

Papua New

Guinea

Paraguay

Peru

Philippines

Tunisia

Turkey

Turkmenistan

Turks and

Caicos Islands

Tuvalu

Uganda

Ukraine

United Arab

Emirates

United Kingdom

United States

United States

Minor Outlying

Islands

Jersey

Jordan

Kazakhstan

Kenya

Kiribati

Kosovo

Kuwait

Kyrgyzstan

Laos

Latvia

Lebanon

Pitcairn Islands

Poland

Portugal

Puerto Rico

Qatar

Réunion

Romania

Russia

Rwanda

Saint Barthélemy

Saint Helena

Ascension and

Tristan da Cunha

Uruguay

US Virgin Islands

Uzbekistan

Vanuatu

Vatican City

Venezuela

Vietnam

Wallis and

Futuna

Western Sahara

Yemen

Zambia

Democratic

Republic of the

Congo

Denmark

*

Field

Lesotho

Saint Kitts and

Nevis

Zimbabwe

Liberia

Saint Lucia

of activity or sector

6

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Accounting

Auditing

Banking

Credit rating agencies

Insurance

Pension provision

Investing

Investment management (e.g. hedge funds, private equity funds, venture

capital funds, money market funds, securities)

Financial advice

Administration of benchmarks

Providing of ESG data and/or ratings

Structuring/issuance of securities

Market infrastructure operation (e.g. CCPs, CSDs, Stock exchanges)

Social entrepreneurship

Other

Not applicable

*

Please

specify your activity field(s) or sector(s)

The Danish Financial Supervisory Authority (the Danish FSA) is part of the Danish public administration.

*

To

which category do you mainly belong or do you mainly represent:

I am a financial market participant as defined in Article 2(1) of the Sustainable

Finance Disclosure Regulation (SFDR)

I am a financial adviser as defined in Article 2(11) of SFDR

I am both a financial market participant as defined in Article 2(1) of the SFDR

and a financial adviser as defined in Article 2(11) of SFDR

I am another type of financial undertaking that does not fall under th definition

of financial market participant of the SFDR

I am a non-financial undertaking

I am a non-professional investor

I am a professional investor

I am a national authority or supervisor

I am an NGO

I am an ESG data and/or ratings provider

7

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

I am a benchmark administrator

I am an academic

My organisation is none of the above

The Commission will publish all contributions to this targeted consultation. You can choose whether you

would prefer to have your details published or to remain anonymous when your contribution is published.

Fo

r the purpose of transparency, the type of respondent (for example, ‘business association,

‘consumer association’, ‘EU citizen’) country of origin, organisation name and size, and its

transparency register number, are always published. Your e-mail address will never be published.

Opt in to select the privacy option that best suits you. Privacy options default based on the type of

respondent selected

*

Contribution

publication privacy settings

The Commission will publish the responses to this public consultation. You can choose whether you would like

your details to be made public or to remain anonymous.

Anonymous

Only organisation details are published: The type of respondent that you

responded to this consultation as, the name of the organisation on whose

behalf you reply as well as its transparency number, its size, its country of

origin and your contribution will be published as received. Your name will not

be published. Please do not include any personal data in the contribution itself

if you want to remain anonymous.

Public

Organisation details and respondent details are published: The type of

respondent that you responded to this consultation as, the name of the

organisation on whose behalf you reply as well as its transparency number, its

size, its country of origin and your contribution will be published. Your name

will also be published.

I agree with the

personal data protection provisions

Would you be available for follow-up questions under the contact information

you provided above?

Yes

No

Section 1. Current requirements of the SFDR

8

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

The EU’s sustainable finance policy is designed to attract private investment to support the transition to a sustainable,

climate-neutral economy. The SFDR is designed to contribute to this objective by providing transparency to investors

about the sustainability risks that can affect the value of and return on their investments (‘outside-in’ effect) and the

adverse impacts that such investments have on the environment and society (‘inside-out’). This is known as double

materiality. This section of the questionnaire seeks to assess to what extent respondents consider that the SFDR is

meeting its objectives in an effective and efficient manner and to identify their views about potential issues in the

implementation of the regulation.

We are seeking the views of respondents on how the SFDR works in practice. In particular, we would like to know more

about potential issues stakeholders might have encountered regarding the concepts it establishes and the disclosures it

requires.

Question 1.1 The SFDR seeks to strengthen transparency through

sustainability-related disclosures in the financial services sector to support

the EU’s shift to a sustainable, climate neutral economy.

In your view, is this broad objective of the regulation still relevant?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

9

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.2 Do you think the SFDR disclosure framework is effective in achieving the following specific

objectives (included in its

Explanatory Memorandum

and mentioned in its recitals):

Note: In this questionnaire we refer to the term ‘end investor’ (retail or professional) to designate the ultimate beneficiary of

the investments in financial products (as defined under the SFDR) made by a person for their own account.

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

Increasing transparency towards end investor with regard to the

integration of sustainability risks

Increasing transparency towards end investor with regard to the

consideration of adverse sustainability impacts

Strengthening protection of end investors and making it easier for

them to benefit from and compare among a wide range of financial

products and services, including those with sustainability claims

Channelling capital towards investments considered sustainable,

including transitional investments (‘investments considered

sustainable’ should be understood in a broad sense, not limited to

the definition of sustainable investment set out in Article 2(17) of

SFDR)

10

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Ensuring that ESG considerations are integrated into the

investment and advisory process in a consistent manner across

the different financial services sectors

Ensuring that remuneration policies of financial market participants

and financial advisors are consistent with the integration of

sustainability risks and, where relevant, sustainable investment

targets and designed to contribute to long-term sustainable growth

11

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

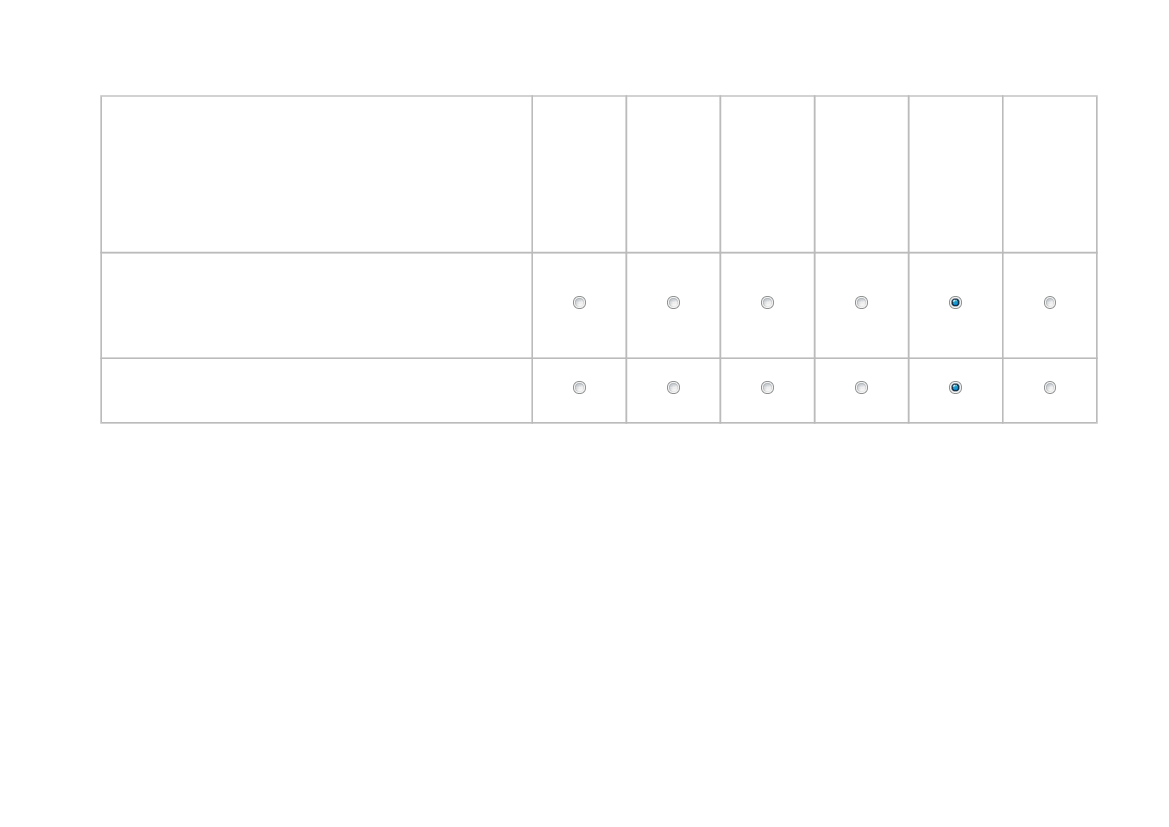

Question 1.3 Do you agree that opting for a disclosure framework at EU level

was more effective and efficient in seeking to achieve the objectives

mentioned in Question 1.2 than if national measures had been taken at

Member State level?

1 - Totally disagree

2 - Mostly disagree

3 - Partially disagree and partially agree

4 - Mostly agree

5 - Totally agree

Don’t know / no opinion / not applicable

Question 1.4 Do you agree that the costs of disclosure under the SFDR

framework are proportionate to the benefits it generates (informing end

investors, channelling capital towards sustainable investments)?

1 - Totally disagree

2 - Mostly disagree

3 - Partially disagree and partially agree

4 - Mostly agree

5 - Totally agree

Don’t know / no opinion / not applicable

We are seeking the views of respondents on how the SFDR works in practice and the impact it has had.

12

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

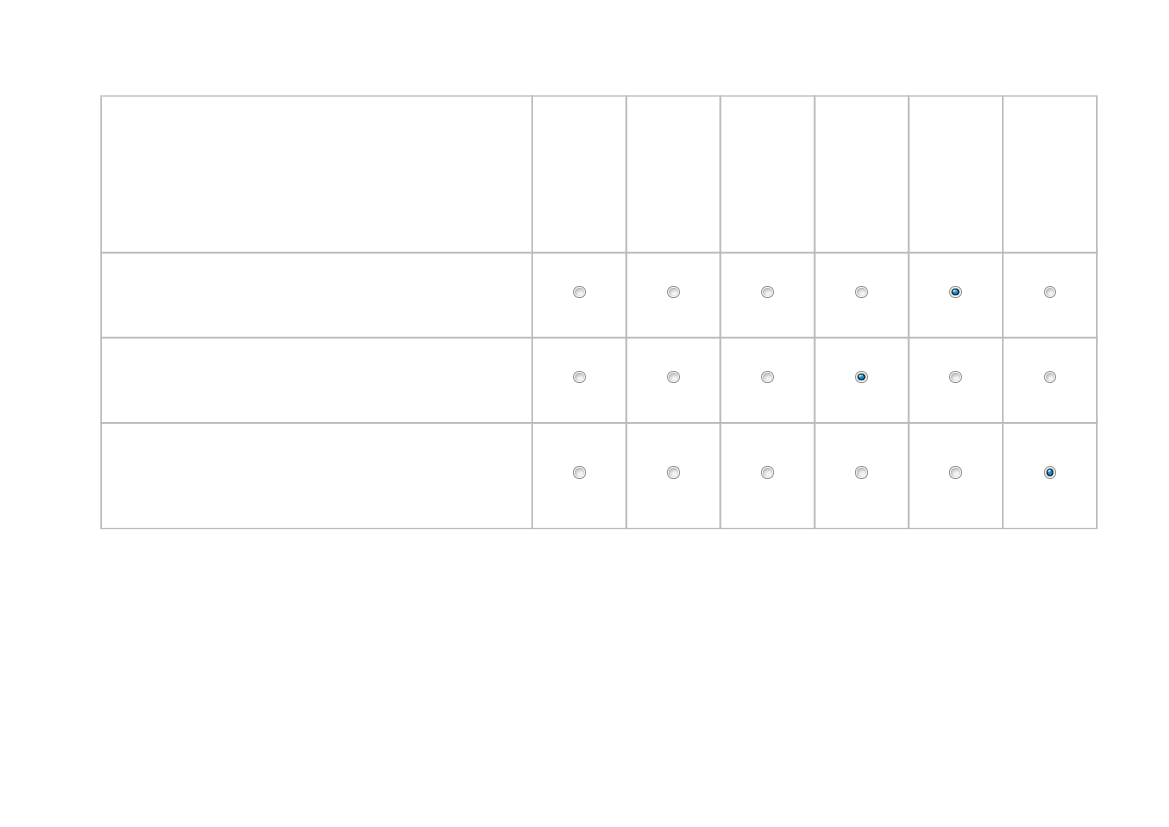

Question 1.5 To what extent do you agree with the following statements?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

The SFDR has raised awareness in the financial services sector of

the potential negative impacts that investment decisions can have

on the environment and/or people

Financial market participants have changed the way they make

investment decisions and design products since they have been

required to disclose sustainability risks and adverse impacts at

entity and product level under the SFDR

The SFDR has had indirect positive effects by increasing pressure

on investee companies to act in a more sustainable manner

13

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

We would also like to know more about potential issues stakeholders might have encountered regarding the concepts

that the SFDR establishes and the disclosures it requires.

14

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.6 To what extent do you agree or disagree with the following statements?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

Some disclosures required by the SFDR are not sufficiently useful

to investors

Some legal requirements and concepts in the SFDR, such as

‘sustainable investment’, are not sufficiently clear

The SFDR is not used as a disclosure framework as intended, but

as a labelling and marketing tool (in particular Articles 8 and 9)

Data gaps make it challenging for market participants to disclose

fully in line with the legal requirements under the SFDR

Re-use of data for disclosures is hampered by a lack of a common

machine-readable format that presents data in a way that makes

them easy to extract

There are other deficiencies with the SFDR rules (please in text

box following question 1.7)

15

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.7 To what extent do you agree or disagree with the following statements?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

The issues raised in question 1.6 create legal uncertainty for

financial market participants and financial advisers

The issues raised in question 1.6 create reputational risks for

financial market participants and financial advisers

The issues raised in question 1.6 do not allow distributors to have

a sufficient or robust enough knowledge of the sustainability profile

of the products they distribute

The issues raised in question 1.6 create a risk of greenwashing

and mis-selling

The issues raised in question 1.6 prevent capital from being

allocated to sustainable investments as effectively as it could be

The current framework does not effectively capture investments in

transition assets

The current framework does not effectively support a robust

enough use of shareholder engagement as a means to support the

transition

16

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Others

17

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Please provide any additional explanations as necessary for questions 1.5,

1.6 and 1.7:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

In terms of any “other deficiencies with the SFDR”, we believe the framework could be strengthened further

through:

- A clear definition of transition investments/products at level 1.

- A further specification on the use of EU climate benchmarks in, respectively, active and passive investment

strategies for, respectively, “Article 8” and “Article 9” SFDR products.

- Setting minimum requirements for "E/S characteristics" or replacing it with a minimum percentage of

sustainable investments for "Article 8" SFDR products.

- Setting further and explicit requirements for DNSH, good governance and social contributions. This could

be supplemented by a “social framework” in SFDR to complement the EU taxonomy.

Disclosures of principal adverse impacts (PAIs)

There are several disclosures concerning PAIs in the SFDR. As a general rule, the SFDR requires financial market

participants who consider PAIs to disclose them at entity level on their website. It also includes a mandatory

requirement for financial market participants to provide such disclosures when they have more than 500 employees

(Article 4). The

Delegated Regulation

of the SFDR includes a list of these PAI indicators. These entity level PAI

indicators are divided into three tables in the Delegated Regulation. Indicators listed in table 1 are mandatory for all

participants, and indicators in tables 2 and 3 are subject to a materiality assessment by the financial market participant

(at least one indicator from table 2 and one from table 3 must be included in every PAI statement).

Second, the SFDR requires financial market participants who consider PAIs at entity level to indicate in the pre-

contractual documentation whether their financial products consider PAIs (Article 7) and to report the impacts in the

corresponding periodic disclosures (Article 11). When reporting these impacts, financial market participants may rely on

the PAI indicators defined at entity level in the Delegated Regulation.

Finally, in accordance with the empowerment given in Article 2a of SFDR, the Delegated Regulation requires that the

do no significant harm (DNSH) assessment of the sustainable investment definition is carried out by taking into account

the PAI indicators defined at entity level in Annex I of the Delegated Regulation.

In this context:

18

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

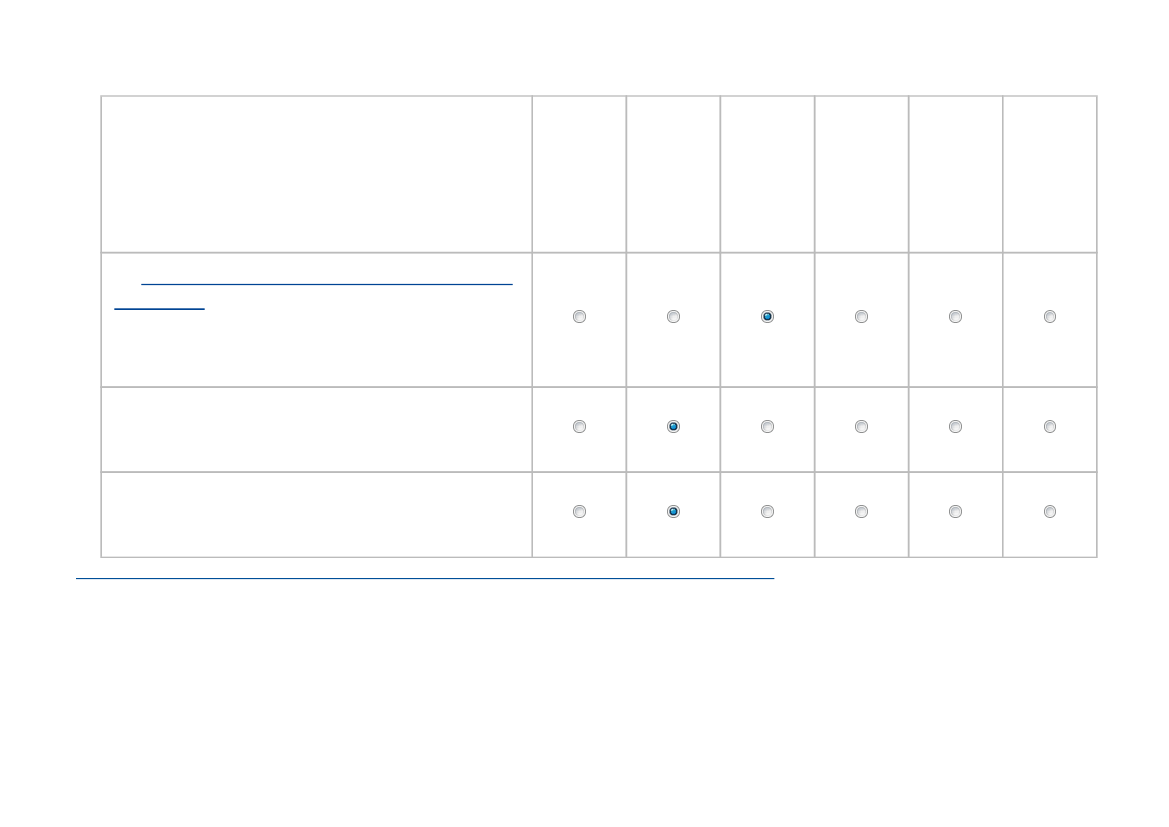

Question 1.8 To what extent do you agree with the following statements about entity level disclosures?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

I find it appropriate that certain indicators are always considered

material (i.e. “principal”) to the financial market participant for its

entity level disclosures, while having other indicators subject to a

materiality assessment by the financial market participant

(approach taken in Annex I of the SFDR Delegated Regulation)

I would find it appropriate that all indicators are always considered

material (i.e. “principal”) to the financial market participant for its

entity level disclosures

I would find it appropriate that all indicators are always subject to a

materiality assessment by the financial market participant for its

entity level disclosures

19

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.8.1 When following the approach described in the first statement

of question 1.8 above, do you agree that the areas covered by the current

indicators listed in table 1 of the Delegated Regulation are the right ones to

be considered material in all cases?

1 - Totally disagree

2 - Mostly disagree

3 - Partially disagree and partially agree

4 - Mostly agree

5 - Totally agree

Don’t know / no opinion / not applicable

20

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.9 To what extent do you agree with the following statements about product level disclosures?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

The requirement to ‘take account of’ PAI indicators listed in Annex

I of the Delegated Regulation for the DNSH assessment, does not

create methodological challenges

In the context of product disclosures for the do no significant harm

(DNSH) assessment, it is clear how materiality of principal adverse

impact (PAI) indicators listed in Annex I of the Delegated

Regulation should be applied

The possibility to consider the PAI indicators listed in Annex I of

the Delegated Regulation for product level disclosures of Article 7

do not create methodological challenges

It is clear how the disclosure requirements of Article 7 as regards

principal adverse impacts interact with the requirement to disclose

information according to Article 8 when the product promotes

environmental and/or social characteristics and with the

requirement to disclose information according to Article 9 when the

product has sustainable investment as its objective

21

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Please provide any additional explanations as necessary for questions 1.8,

1.8.1 and 1.9:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

- We support alignment of SFDR with CSRD/ESRS, also in terms of a potential materiality assessment/test

in PAI reporting.

- In terms of the use of PAI in the DNSH test, it could be further highlighted that all the mandatory PAI

indicators must be used, and add a requirement for FMPs to disclose the thresholds and criteria used to

determine when significant harm is done for each of the PAI indicators.

- It would increase the simplicity and comparability of SFDR, if the mandatory PAI indicators had to be used

for Article 7 reporting, and to make Article 7 reporting mandatory for all "Article 8" and "Article 9" SFDR

products.

The cost of disclosures under the SFDR today

Questions 1.10, 1.10.1 and 1.11 are intended for financial market participants and financial

advisors subject to the SFDR.

The following two questions aim to assess the costs of the SFDR disclosure requirements distinguishing between one-

off and recurring costs. One-off costs are incurred only once to implement a new reporting requirement, e.g. getting

familiarised with the legal act and the associated regulatory or implementing technical standards, setting-up data

collection processes or adjusting IT-systems. Recurring costs occur repeatedly every year once the new reporting is in

place, e.g. costs of annual data collection and report preparation. In the specific case of precontractual disclosures for

example, there are one-off costs to set up the process of publishing precontractual disclosures when a new product is

launched, and recurring annual costs to repeat the process of publishing pre-contractual disclosures each time a new

product is launched (depends on the number of products launched on average each year). These two questions apply

both to entity and product level disclosures.

22

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.10 Could you provide estimates of the one-off and recurring annual costs associated with complying

with the SFDR disclosure requirements (EUR)?

Please split these estimates between internal costs incurred by the financial market participant and any external

services contracted to assist in complying with the requirements (services from third-party data providers,

advisory services, etc.).

If such a breakdown is not possible, please provide the total figures.

Please leave the cell blank for the data you are not able to provide.

Estimated one off costs

(in euros)

Estimated recurring annual costs

(in euros)

Total internal costs

Internal costs for personnel

Internal costs for IT

Total external costs

External costs for data providers

External costs for advisory services

23

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Total costs of SFDR disclosure

requirements

24

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.10.1: Could you split the total costs between product level and entity level disclosures?

Please leave the cell blank for the data you are not able to provide.

Product-level disclosures

(in %)

Entity-level disclosures

(in %)

Estimated percentage of costs

25

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

If you wish, please provide additional details:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

Question 1.11 In order to have a better understanding of internal costs, could

you provide an estimate of how many full-time-equivalents (FTEs - 1 FTE

corresponds to 1 employee working full-time the whole year) are involved in

preparing SFDR disclosures?

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

26

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.11.1 Could you please provide a split between:

Please leave the cell blank for the data you are not able to provide.

Retrieving the data

(in %)

Analysing the data

(in %)

Reporting SFDR disclosures

(in %)

Other

(in %)

Estimated percentage

27

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Please specify what corresponds to “other” costs:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

Data and estimates

Financial market participants' and financial advisers’ ability to fulfil their ESG transparency requirements depends in

part on other disclosure requirements under the EU framework. In particular, they will rely to a significant extent on the

Corporate Sustainability Reporting Directive (CSRD)

. However, entities are not reporting yet under those new

disclosure requirements, or they may not be within the scope of the CSRD. Besides, even when data is already

available today, it may not always be of good quality.

Question 1.12 Are you facing difficulties in obtaining good-quality data?

Yes

No

Don’t know / no opinion / not applicable

Question 1.12.2 Is the SFDR sufficiently flexible to allow for the use of

estimates?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Question 1.12.3 Is it clear what kind of estimates are allowed by the SFDR?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Question 1.12.4 If you use estimates, what kind of estimates do you use to fill the data gap?

28

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

a) For entity level principal adverse impacts:

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Estimates

from data

providers,

based on

data coming

from the

investee

companies

Estimates

from data

providers,

based on

data coming

from other

sources

In-house

estimates

Internal ESG

score models

External

ESG score

models

Other

b) For taxonomy aligned investments (product level):

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Estimates

from data

providers,

29

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

based on

data coming

from the

investee

companies

Estimates

from data

providers,

based on

data coming

from other

sources

In-house

estimates

Internal ESG

score models

External

ESG score

models

Other

c) For sustainable investments (product level):

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Estimates

from data

providers,

based on

data coming

from the

investee

companies

Estimates

from data

providers,

based on

30

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

data coming

from other

sources

In-house

estimates

Internal ESG

score models

External

ESG score

models

Other

d) Other data points:

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Estimates

from data

providers,

based on

data coming

from the

investee

companies

Estimates

from data

providers,

based on

data coming

from other

sources

In-house

estimates

Internal ESG

score models

31

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

External

ESG score

models

Other

Question 1.12.5 Do you engage with investee companies to encourage

reporting of the missing data?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Please provide further explanations to your replies to questions 1.12 to 1.12.5:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

Question 1.13 Have you increased your offer of financial products that make

sustainability claims since the disclosure requirements of Articles 8 and 9 of

the SFDR began to apply (i.e. since 2021, have you been offering more

products that you categorise as Articles 8 and 9 than those you offered

before the regulation was in place and for which you also claimed a certain

sustainability performance)?

1 - Not at all

2 - To a limited extent

3 - To some extent

32

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

33

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.13.1 Please specify how the share of financial products making sustainability claims has evolved in

the past years

(Please express it as a percentage of the total financial products you offered each year)

Percentage of the total financial products

2020

2021

2022

2023

34

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 1.13.2 If you have increased your offering of financial products

making sustainability claims, in your view, has any of the following factors

influenced this increase?

Don't

know -

1

(not at all)

2

(not really)

3

(partially)

4

(mostly)

5

(totally)

No

opinion -

Not

applicable

SFDR

requirements

Retail investor

interest

Professional

investor interest

Market

competitiveness

Other factors

Please provide further explanations to your replies to questions 1.13, 1.13

1 and 1.13.2:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

Section 2. Interaction with other sustainable finance

legislation

The SFDR interacts with other parts of the EU’s sustainable finance framework. Questions in this section will therefore

seek respondents’ views about the current interactions, as well as potential inconsistencies or misalignments that might

exist between the SFDR and other sustainable finance legislation. There is a need to assess the potential implications

for other sustainable finance legal acts if the SFDR legal framework was changed in the future. Questions as regards

these potential implications are included in section 4 of this questionnaire, when consulting on the potential

establishment of a categorisation system for products, and they do not prejudge future positions that might be taken by

the Commission.

35

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

The SFDR mainly interacts with the following legislation and their related delegated and implementing acts:

the

Taxonomy Regulation

the

Benchmarks Regulation

the

Corporate Sustainability Reporting Directive (CSRD)

the

Markets in Financial Instruments Directive (MiFID 2)

and the

Insurance Distribution Directive (IDD)

the

Regulation on Packaged Retail Investment and Insurance Products (PRIIPs)

Other legal acts that are currently being negotiated may also interact with the SFDR in the future. They are not covered

in this questionnaire as the detailed requirements of these legal acts have not yet been agreed. At this stage, it would

be speculative to seek to assess how their interaction with SFDR would function.

Both the SFDR and the Taxonomy Regulation introduce key concepts to the sustainable finance framework. Notably,

they introduce definitions of ‘sustainable investment’ (SFDR) and ‘environmentally sustainable’ economic activities

(taxonomy). Both definitions require, inter alia, a contribution to a sustainable objective and a do no significant harm

(DNSH) test. But while these definitions are similar, there are differences between them which could create practical

challenges for market participants.

Question 2.1 The

Commission recently adopted a FAQ

clarifying that

investments in taxonomy-aligned ‘environmentally sustainable’ economic

activities can automatically qualify as ‘sustainable investments’ in those

activities under the SFDR.

To what extent do you agree that this FAQ offers sufficient clarity to market

participants on how to treat taxonomy-aligned investment in the SFDR

product level disclosures?

1 - Totally disagree

2 - Mostly disagree

3 - Partially disagree and partially agree

4 - Mostly agree

5 - Totally agree

Don’t know / no opinion / not applicable

The Benchmarks Regulation introduces two categories of climate benchmarks – the EU climate transition benchmark

(EU CTB) and the EU Paris-aligned benchmark (EU PAB) - and requires benchmark administrators to disclose on ESG

related matters for all benchmarks (except interest rate and foreign exchange benchmarks). The SFDR makes

reference to the CTB and PAB in connection with financial products that have the reduction of carbon emissions as

their objective. Both legal frameworks are closely linked as products disclosing under the SFDR can for example

passively track a CTB or a PAB or use one of them as a reference benchmark in an active investment strategy. More

broadly, passive products rely on the design choices made by the benchmark administrators.

36

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 2.2 To what extent do you agree or disagree with the following statements?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

The

questions

& answers published by the Commission

in April 2023

specifying that the SFDR deems products

passively tracking CTB and PAB to be making ‘sustainable

investments’ as defined in the SFDR provide sufficient clarity to

market participants

The approach to DNSH and good governance in the SFDR is

consistent with the environmental, social and governance

exclusions under the PAB/CTB

The ESG information provided by benchmark administrators is

sufficient and is aligned with the information required by the SFDR

for products tracking or referencing these benchmarks

37

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Both the SFDR and the Corporate Sustainability Reporting Directive (CSRD) introduce entity level disclosure

requirements with a double-materiality approach

[1]

. The CSRD sets out sustainability reporting requirements mainly for

all large and all listed undertakings with limited liability (except listed micro-enterprises)

[2]

, while the SFDR introduces

sustainability disclosure requirements at entity level for financial market participants and financial advisers as regards

the consideration of sustainability related factors in their investment decision-making process. Moreover, in order for

financial market participants and financial advisers to meet their product and entity level disclosure obligations under

the SFDR, they will rely to a significant extent, on the information reported according to the CSRD and its

European

Sustainability Reporting Standards (ESRS)

(provided positive scrutiny of co-legislators of the

ESRS delegated act

).

1

Transparency requirements relate to the sustainability risks that can affect the value of investments (SFDR) or companies (CSRD) (‘outside-in’

effect) and the adverse impacts that such investments or companies have on the environment and society (‘inside-out’).

2

Credit institutions and insurance undertakings with unlimited liability are also in scope subject to the same size criteria. Non-EU undertakings

listed on the EU regulated markets and non-EU undertakings with a net turnover above EUR 150 million that carry out business in the EU will

also have to publish certain sustainability-related information through their EU subsidiaries that are subject to CSRD (or - in the absence of such

EU subsidiaries – through their EU branches with net turnover above EUR 40 million).

38

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 2.3 To what extent do you agree or disagree with the following statements?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

The SFDR disclosures are consistent with the CSRD

requirements, in particular with the European Sustainability

Reporting Standards

There is room to streamline the entity level disclosure

requirements of the SFDR and the CSRD

39

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Financial advisors (under MiFID 2) and distributors of insurance-based investment products (under IDD) have to

conduct suitability assessments based on the sustainability preferences of customers. These assessments rely in part

on sustainability-related information made available by market participants reporting under the SFDR.

Question 2.4 To what extent do you agree that the product disclosures

required in the SFDR and

its Delegated Regulation

(e.g. the proportion of

sustainable investments or taxonomy aligned investments, or information

about principal adverse impacts) are sufficiently useful and comparable to

allow distributors to determine whether a product can fit investors’

sustainability preferences under MiFID 2 and the IDD?

1 - Totally disagree

2 - Mostly disagree

3 - Partially disagree and partially agree

4 - Mostly agree

5 - Totally agree

Don’t know / no opinion / not applicable

Question 2.5 MIFID and IDD require financial advisors to take into account

sustainability preferences of clients when providing certain services to them.

Do you believe that, on top of this behavioural obligation, the following

disclosure requirements for financial advisors of the SFDR are useful?

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Article 3,

entity level

disclosures

about the

integration of

sustainability

risks policies

in investment

or insurance

advice

Article 4,

entity level

disclosures

40

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

about

consideration

of principal

adverse

impacts

Article 5,

entity level

disclosures

about

remuneration

policies in

relation to

the

integration of

sustainability

risks

Article 6,

product level

pre-

contractual

disclosures

about the

integration of

sustainability

risks in

investment

or insurance

advice

Article 12,

requirement

to keep

information

disclosed

according to

Articles 3

and 5 up to

date

Question 2.6 Have the requirements on distributors to consider sustainability

preferences of clients impacted the quality and consistency of disclosures

made under SFDR?

Yes

No

Don’t know / no opinion / not applicable

41

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

PRIIPs requires market participants to provide retail investors with

key information documents (KIDs)

. As part of the

reta

il investment strategy

, the Commission has recently proposed to include a new sustainability section in the KID to make

sustainability-related information of investment products more visible, comparable and understandable for retail

investors. Section 4 of this questionnaire includes questions related to PRIIPs, to seek stakeholders’ views as regards

potential impacts on the content of the KID if a product categorisation system was established.

Please clarify your replies to questions in section 2 as necessary:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

- We support alignment of SFDR with CSRD/ESRS also in terms of a potential materiality assessment/test in

PAI reporting.

- In terms of the use of PAI indicators in the DNSH test, it could be further highlighted that all the mandatory

PAI indicators must be used, and to add a requirement for FMPs to disclose the thresholds and criteria used

to determine when significant harm is done for each of the PAI indicators.

- It would increase the simplicity and comparability of SFDR, if the mandatory PAI indicators had to be used

for Art. 7 reporting, and to make Art. 7 reporting mandatory for all "Article 8" and "Article 9" SFDR products.

Section 3. Potential changes to disclosure requirements for

financial market participants

3.1 Entity level disclosures

The SFDR contains entity level disclosure requirements for financial market participants and financial advisers. They

shall disclose on their website their policies on the integration of sustainability risks in their investment decision-making

process or their investment or insurance advice (Article 3). In addition, they shall disclose whether, and if so, how, they

consider the principal adverse impacts of their investment decisions on sustainability factors. For financial market

participants with 500 or more employees, the disclosure of a due diligence statement, including information of adverse

impacts, is mandatory (Article 4). In addition, financial market participants and financial advisers shall disclose how their

remuneration policies are consistent with the integration of sustainability risks (Article 5).

Question 3.1.1 Are these disclosures useful?

Don't know -

1

(not at all)

Article

3

Article

4

2

(not really)

3

(partially)

4

(mostly)

5

(totally)

No opinion -

Not

applicable

42

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Article

5

Please explain your replies to question 3.1.1 as necessary:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

- PAI-reporting at entity level is less relevant for some investors. If the obligation to make PAI-reporting at

entity level is to be revised, then we would suggest considering removing the obligation for CSRD-

companies.

- That said, we consider it is important to maintain the obligation (to do PAI reporting at entity level) for at

least the non-CSRD companies, as the information would elsewise be lacking.

- Moreover, PAI-reporting at product level should be mandatory for "Article 8" and "Article 9" SFDR products.

This revision should also include a requirement to use the mandatory PAI indicators also for Artcle 7

reporting.

Complementing the

consultation by the European Supervisory Authorities (ESAs) on the revision of the regulatory

technical standards of the SFDR

, the Commission is interested in respondents’ views as regards the principal adverse

impact indicators required by the current Delegated Regulation.

Question 3.1.2 Among the specific entity level principal adverse impact

indicators required by the

Delegated Regulation of the SFDR

adopted

pursuant to Article 4 (tables 1, 2 and 3 of Annex I), which indicators do you

find the most (and least) useful?

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

-

Most useful are:

PAI indicator no.: 1 (GHG emissions)

2 (carbon footprint)

3 (GHG intensity of investment companies)

4 (Exposure to companies active in the fossil fuel sector)

7 (Activities negatively affecting biodiversity-sensitive areas) and

8 (Emissions to water).

Several pieces of EU legislation require entity level disclosures, whether through transparency requirements on

sustainability for businesses (for example the CSRD) or disclosure requirements regarding own ESG exposures (such

as the Capital Requirements Regulation (CRR) and its Delegated Regulation).

43

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 3.1.3 In this context, is the SFDR the right place to include entity

level disclosures?

1 - Not at all

2 - Not really

3 - Partially

4 - Mostly

5 - Totally

Don’t know / no opinion / not applicable

Question 3.1.4 To what extent is there room for streamlining sustainability-

related entity level requirements across different pieces of legislation?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Please explain your replies to questions in section 3.1 as necessary:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

- SFDR is the right place to include entity level disclosures at least for the FMPs in SFDR, which are not

subject to CSRD reporting.

3.2 Product level disclosures

The SFDR includes product level disclosure requirements (Articles 6, 7, 8, 9, 10 and 11) that mainly concern risk and

adverse impact related information, as well as information about the sustainability performance of a given financial

product. The regulation determines which information should be included in precontractual and periodic documentation

and on websites.

44

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

The SFDR was designed as a disclosure regime, but is being used as a labelling scheme, suggesting that there might

be a demand for establishing sustainability product categories. Before assessing whether there might be merit in setting

up such product categories in Section 4, Section 3 includes questions analysing the need for possible changes to

disclosures, as well as any potential link between product categories and disclosures. The need to ask about potential

links between disclosures and sustainability product categories is the reason why this section contains some references

to ‘products making sustainability claims’. However, this does not pre-empt in any way a decision about how a potential

categorisation system and an updated disclosure regime would interact if these were established. The Commission

services are openly consulting on all these issues to further assess potential ways forward as regards the SFDR.

The Commission services would therefore like to collect feedback on what transparency requirements stakeholders

consider useful and necessary. We would also like to know respondents’ views on whether and how these

transparency requirements should link to different potential categories of products.

The general principle of the SFDR is that products that make sustainability claims need to disclose information to back

up those claims and combat greenwashing. This could be viewed as placing additional burden on products that factor in

sustainability considerations. This is why, in the following questions Commission services ask respondents about the

usefulness of uniform disclosure requirements for products across the board, regardless of related sustainability claims,

departing from the general philosophy of the SFDR as regards product disclosures. Providing proportionate information

on the sustainability profile of a product which does not make sustainability claims could make it easier for some

investors to understand products’ sustainability performance, as they would get information also about products that are

not designed to achieve any sustainability-related outcome. This section also contains questions exploring whether it

could be useful to require financial market participants who make sustainability claims about certain products to

disclose additional information (i.e. in case a categorisation system is introduced in the EU framework, the need to

require additional information about products that would fall under a category).

Question 3.2.1 Standardised product disclosures - Should the EU impose

uniform disclosure requirements for all financial products offered in the EU,

regardless of their sustainability-related claims or any other consideration?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Question 3.2.1 a) If the EU was to impose uniform disclosure requirements

for all financial products offered in the EU, should disclosures on a limited

number of principal adverse impact indicators be required for all financial

products offered in the EU?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

45

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Don’t know / no opinion / not applicable

Please specify which principal adverse impact indicators should be required

for all financial products offered in the EU:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

PAI indicator number:

1 (GHG emissions)

2 (carbon footprint)

3 (GHG intensity of investment companies)

4 (Exposure to companies active in the fossil fuel sector)

7 (Activities negatively affecting biodiversity-sensitive areas)

8 (Emissions to water) and 10 (Violations of UN Global Compact principles and Organisation for Economic

Cooperation and Development (OECD) Guidelines for Multinational Enterprises) and

13 (Board gender diversity).

Question 3.2.1 b) Please see a list of examples of disclosures that could also

be required about all financial products for transparency purposes.

In your view, should these disclosures be mandatory, and/or should any

other information be required about all financial products for transparency

purposes?

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Taxonomy-

related

disclosures

Engagement

strategies

Exclusions

Information

about how

ESG-related

information

is used in

the

investment

process

46

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Other

information

Please specify what other information should be required about all financial

products:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

-Whether there is PAI reporting at product level.

-Whether the product is Paris-aligned.

Please explain as necessary your replies to questions 3.2.1 and its sub-

questions:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

Question 3.2.2 Standardised product disclosures - Would uniform disclosure

requirements for some financial products be a more appropriate approach,

regardless of their sustainability-related claims (e.g. products whose assets

under management, or equivalent, would exceed a certain threshold to be

defined, products intended solely for retail investors, etc.)?

(Please note that next question 3.2.3 asks specifically about the need for disclosures

in cases of products making sustainability claims.)

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

47

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

5 - To a very large extent

Don’t know / no opinion / not applicable

Question 3.2.2 a) If the EU was to impose uniform disclosure requirements

for some financial products, what would be the criterion/criteria that would

trigger the reporting obligations?

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

- Use of exclusions, active ownership, whether the product is Paris-aligned.

Question 3.2.2 b) If the EU was to impose uniform disclosure requirements

for some financial products, should a limited number of principal adverse

impact indicators be required?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Please specify which principal adverse impact indicators should be required:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

See Q. 3.2.1.a.

48

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 3.2.2 c) Please see a list of examples of disclosures that could also

be required about the group of financial products that would be subject to

standardised disclosure obligations for transparency purposes (in line with

your answer to Q 3.2.2 above).

In your view, should these disclosures be mandatory, and/or should any

other information be required about that group of financial products?

Don't

1

(not at all)

2

(to a

limited

extent)

3

(to some

extent)

4

(to a large

extent)

5

(to a very

large

extent)

know -

No

opinion -

Not

applicable

Taxonomy-

related

disclosures

Engagement

strategies

Exclusions

Information

about how

ESG-related

information

is used in

the

investment

process

Other

information

Please specify what other information should be required about the financial

products that would be subject to disclosure obligations:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

- Whether the product is investing in alignment with the Paris Agreement.

49

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Please explain as necessary your replies to questions 3.2.2 and its sub-

questions:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

It can be difficult for consumers and investors to determine whether an investment product is aligned with the

Paris Agreement, while this is one of the most relevant and used benchmarks for assessing transition or

sustainability.

We propose that alignment with the Paris Agreement is used more broadly as a clear and understandable

indicator for the sustainability profile of a product, as e.g. specific GHG-emission targets or transition “claims”

can be difficult for end investors to assess or understand.

The following and last section of this questionnaire (section 4) includes questions about the potential establishment of a

sustainability product categorisation system at EU level based on certain criteria that products would have to meet. It

presents questions about different ways of setting up such system, including whether additional category specific

disclosure requirements should be envisaged. There are therefore certain links between questions in this section

(section 3) and questions in the last section of the questionnaire (section 4).

Question 3.2.3 If requirements were imposed as per question 3.2.1 and/or

3.2.2, should there be some additional disclosure requirements when a

product makes a sustainability claim?

1 - Totally disagree

2 - Mostly disagree

3 - Partially disagree and partially agree

4 - Mostly agree

5 - Totally agree

Don’t know / no opinion / not applicable

Please explain as necessary your replies to question 3.2.3:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

50

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Sustainability product information disclosed according to the current requirements of the SFDR can be found in

precontractual and periodic documentation and on financial market participants’ websites, as required by Articles 6, 7,

8, 9, 10 and 11.

Question 3.2.4 In general, is it appropriate to have product related

information spread across these three places, i.e. in precontractual

disclosures, in periodic documentation and on websites?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Question 3.2.5 More specifically, is the current breakdown of information

between precontractual, periodic documentation and websites disclosures

appropriate and user friendly?

1 - Not at all

2 - To a limited extent

3 - To some extent

4 - To a large extent

5 - To a very large extent

Don’t know / no opinion / not applicable

Please explain as necessary your replies to questions 3.2.4 and 3.2.5:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.

51

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Current website disclosures make it mandatory for product sustainability information to be publicly available. This

includes portfolios managed under a portfolio management mandate, which can mean a large number of disclosures,

as each of the managed portfolios is considered a financial product under the SFDR. A

Q&A published by the

Commission in July 2021

(see question 3 of section V of the consolidated questions and answers (Q&A) on the SFDR

and its Delegated Regulation published on the ESAs websites) clarified that where a financial market participant makes

use of standard portfolio management strategies replicated for clients with similar investment profiles, transparency at

the level of those standard strategies can be considered a way of complying with requirements on websites disclosures.

This approach facilitates the compliance with Union and national law governing the data protection, and where relevant,

it also ensures confidentiality owed to clients.

52

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Question 3.2.6 To what extent do you agree with the following statements?

1

(totally

disagree)

2

(mostly

disagree)

3

(partially

disagree

and

partially

agree)

4

(mostly

agree)

5

(totally

agree)

Don't

know -

No

opinion -

Not

applicable

It is useful that product disclosures under SFDR are publicly

available, (e.g. because they have the potential to bring wider

societal benefits)

Confidentiality aspects need to be taken into account when

specifying the information that should be made available to the

public under the SFDR

Sustainability information about financial products should be made

available to potential investors, investors or the public according to

rules in sectoral legislation (e.g.: UCITS, AIFM, IORPs directives);

the SFDR should not impose rules in this regard

53

EUU, Alm.del - 2023-24 - Bilag 214: Orienteringsnotat, høringssvar og ministerbrev om dansk høringssvar vedr. Kommissionens offentlige høring om revision af SFDR (disclosureforordningen)

Please explain as necessary your replies to question 3.2.6:

5000 character(s) maximum

including spaces and line breaks, i.e. stricter than the MS Word characters counting method.