Udenrigsudvalget 2013-14, Finansudvalget 2013-14, Klima-, Energi- og Bygningsudvalget 2013-14

URU Alm.del Bilag 42, FIU Alm.del Bilag 26, KEB Alm.del Bilag 74

Offentligt

Audit Result Request- Financial Execution on Budget from Korean Governmentto GGGI -

(Requested by National Assembly)

2012.11.

Bureau of Audit and Inspection1

Table of Contents

I. Overview of the Audit……………………………………………………….6

II. Establishment of GGGI and its Operations………………………….71. Establishment of GGGI and its International Organization conversiontimeline…………………………………………………………………………………………………………….72. The Legal Nature of GGGI…………………………………………………………………………..103. GGGI’s Organization and Employment Status……………………………………………114. GGGI Income and Expenditure Status…………………………………………………………13

III. Audit Findings ………………………………………………………………19[Overview of the Audit Findings]………………………………………………….19

�� Execution of Organizational Operation Expenses…………………………211. Unreasonable Payment of Housing and Child Education Allowances toExecutive Director…………………………………………………………………………………………….212. Unreasonable Payment of Various Allowances including Dispatched Service2

Allowance………………………………………………………………………………………………………….253. Unreasonable Provision of Exclusive Vehicle and Corporate Credit Card toNon-Standing Director………………………………………………………………………………….....31

�� Disbursement of Project Costs……………………………………………341. UnreasonableConclusionandManagementofOutsourcing

Agreements………………………………………………………………………………………………………..342. Unreasonable Conclusion and Management Concerning Ethiopia HouseholdIrrigation Technologies Research Service…………………………………………………………383. Unreasonable Conclusion and Management Concerning Research Service forFormulation of Low-Carbon Development Plan in Shandong Province………....454. Unreasonable Conclusion and Management of AgreementConcerning

Dispatch of Samjong KPMG Experts…………………………………………………………………..475. Improper Outsourcing of Research on Planning for Low-Carbon greenGrowth and Development of Brazil and Two Other Countries……………………..51

�� Execution of Other Expenses and Coaching and Supervision….551. Improper Execution of Expenses for the Office and Improper Management of3

Agreements……………………………………………………………………………………………………….552. Improper Establishment and Operation of an Internal Control System………65

Table of Charts

1. [Table 1] GGGI Establishment Timeline…………………………………………………………72. [Table 2] GGGI International Organization Conversion Timeline………………….93. [Table 3] GGGI Revenue by Country…………………………………………………………….144. [Table 4] Expense by Line Item (ROK support)…………………………………………….145. [Table 5] GGGI Salary Structure and Comparison with Actual Average ofAnnual Salary by Position………………………………………………………………………………….166. [Table 6] GGGI Allowance Standard and Execution Status……………………………177. [Table 7] Payment of Meeting Attendance Allowances Prior to Establishmentof the GGGI………………………………………………………………………………………………………...288. [Table 8] Developments Concerning Mckinsey’s Submission of ResearchService Statements and Their Modification/Supplementation………………………….429. [Table 9] The Budget for Mckinsey of the Outsourcing………………………………..5310. [Table 10] 2010 Budget for the Founding and Operation of the GGGIProvision and Execution…………………………………………………………………………………….56.4

11. [Table 11] Agreements for Office Renovation, etc. Conclude Through Non-Competitive Process…………………………………………………………………………………………6112. [Table 12] Waste of Money and Defects in Purchase of Furniture and“Green Themed” Construction…………………………………………………………………………63

Table of Pictures

[Picture] GGGI Organization Chart…………………………………………………………………….…12

5

I. Overview of the Audit

1.Background and objectivesAccording to Article 127, clause 2 of National Assembly Law, NationalAssembly (Foreign Affairs, Trade and Unification Committee) requested audit onGlobal Green Growth Institute (GGGI), focusing on financial execution on budgetfrom Korean Government on 5 September 2012.

2.Organization for Audit and focusing areaThe audit targets Ministry of Foreign Affairs and Trade, Korea InternationalCooperation Agency (KOICA), and GGGI according to the request from theNational Assembly. The main objective is to review organization operation cost(including salary and various allowances and appropriateness of the payment)and project budget management (including service contract with McKinsey &Company).

3.Period and Audit TeamFrom 10 to 14 September 2012, 4 auditors participated in preliminary review.For 15-day period of actual review, 7 auditors participated from 17 September to6

10 October 2012. After internal process of BAI on November 2012, the result ofthe audit was finalized.

II Establishment of GGGI and it’s Operations

1. Background

In 15 August 2008, the Korean government declared “Low Carbon GreenGrowth” as the new development paradigm of the Republic of Korea andestablished the Global Green Growth Institute on 15 June 2010, with funds fromthe Korea International Cooperation Agency (KOICA), a organization affiliated withthe Ministry of Foreign Affairs, to assist developing countries in the design andimplementation of green growth strategies, and to disseminate green growthglobally. (view [table 1])

[Table 1] GGGI Establishment TimelineDateSubjectIn 15 August 2008, the Korean government declared “Low Carbon Green15 Aug 2008Growth” as the new development paradigm of the Republic of Korea17 Dec 2009Presentation of GGGI establishment plan at COP 15 in Copenhagen

7

Instruction by President Lee Myung-bak to establish GGGI by first half of7 Apr 20102010 (International Organization by 2012 with support from Ministry of Foreign Affairs andTrade and Ministry of Strategy and Finance)

The Presidential Committee on Green Growth requests the establishment19 Apr 2010of GGGI as an affiliated organization to Korean International CooperationAgency(KOICA).20 Apr 201014 May 201016 June 2010Decision by KOICA board of directors to establish GGGIRegistration of Non-Profit Organization under Korean LawAnnouncement of GGGI Establishment at East Asia Climate Forum 2010

*reproduced by GGGI submitted documents

Since then, the GGGI has been working towards converting into aninternational organization with activities such as establishing regional offices inAbu Dhabi, UAE and Copenhagen, Denmark and as seen in [table 2], 16 countriesincluding Korea, Denmark, UK, and Australia signed the “Agreement on theEstablishment of the Global Green Growth Institute” in Rio de Janeiro on 20 June2012.

Following the Signing Ceremony at Rio, Denmark, Guyana and Kiribatisubmitted their Instrument of Ratification of the Establishment Agreement, legallyconverting the GGGI into an international organization on 18 October. In the8

same year, the ratification documents were submitted to the Korean NationalAssembly on 29 August, and in 23 October, the GGGI held a Opening Ceremonyof the Inaugural Meetings of the Assembly and Council, launching the GGGI as aninternational organization.[Table 2] GGGI International Organization Conversion Timeline

Date

SubjectEstablishment of Copenhagen, Denmark regional office, MOU signed with

11 May 2011Danish government7 July 2011Establishment of Abu Dahbi, UAE regional officeSigning Ceremony of the Agreement on the Establishment of the GGGI atRio de Janeiro, Brazil20 June 2012-Signatories: Korea, Denmark, UK, Australia, UAE, Guyana, Qatar,Philippines, Cambodia, Ethiopia, etc-If 3 Signatories ratify the Establishment Agreement, the EstablishmentAgreement takes legal effect29 August 2012Submission of ratification documents to Korean National AssemblyDenmark, Guyana and Kiribati ratification takes effect, fulfilling18 October 2012requirements for an international organizationOpening Ceremony of the Inaugural Meetings of the Assembly and Council23 October 2012in Seoul

9

2.The Legal Nature of GGGI

GGGI is an organization established and registered with the MOFAT as a non-profit foundation on May 14, 2010. Accordingly, it has been under the generalinstruction and supervision of the MOFAT according to the related regulations,such as submitting annual business performance report.Moreover, the MOFAT drew up and executed the needed budget forestablishing and operating GGGI, such as operating and business expenses, aswell as the basic property of GGGI, as contribution from KOICA under thejurisdiction of the MOFAT. In this behalf, GGGI is under the supervision of boththe MOFAT and KOICA (through submission of performance reports and semi-annual review and analysis report).

On the other hand, as the Agreement on GGGI’s conversion into aninternational organization enters into force on October 18, 2012 and goesthrough the ratification process in Korea, the Korean government is expected todraw up a budget and support GGGI with its share of contribution for theinternational organization instead of a contribution from the KOICA, and anindependent external auditor, who the Council of GGGI nominates, will annually

10

conduct the guidance, supervision and audit on this issue according to theinternational accounting standard.

3.GGGI’s Organization and Employment Status

GGGI organization is classified with Board of Directors, Facilitative CommitteeoftheBoardofDirectors,ManagementCommittee,AdvisoryCouncil,

Headquarters and branch offices. Board of Directors is the supreme decision-making body and it is composed of 18 people, 1 person recommended by thegovernment of the country where the headquarters of the GGGI is located, 11people recommended by the government or the organization which has made acertain amount of contribution to GGGI, 4 internationally recognized greengrowth and climate change experts, and 2 green growth and climate changeexperts of developing countries. Han, Seung Soo (term: June 2010 ~ June 2012, aprevious Korean Prime Minister) and Rasmussen at present (term: June 2012 ~June 2015, previous Denmark Prime Minister) has been appointed to thechairman of the board (non-executive). Heo Dong Su (since June2012, CEO of GSCaltex Corp.) is the auditor (non-executive) but GGGI is supposed to be auditedby independent external audit institutions which are entrusted by the auditor.

11

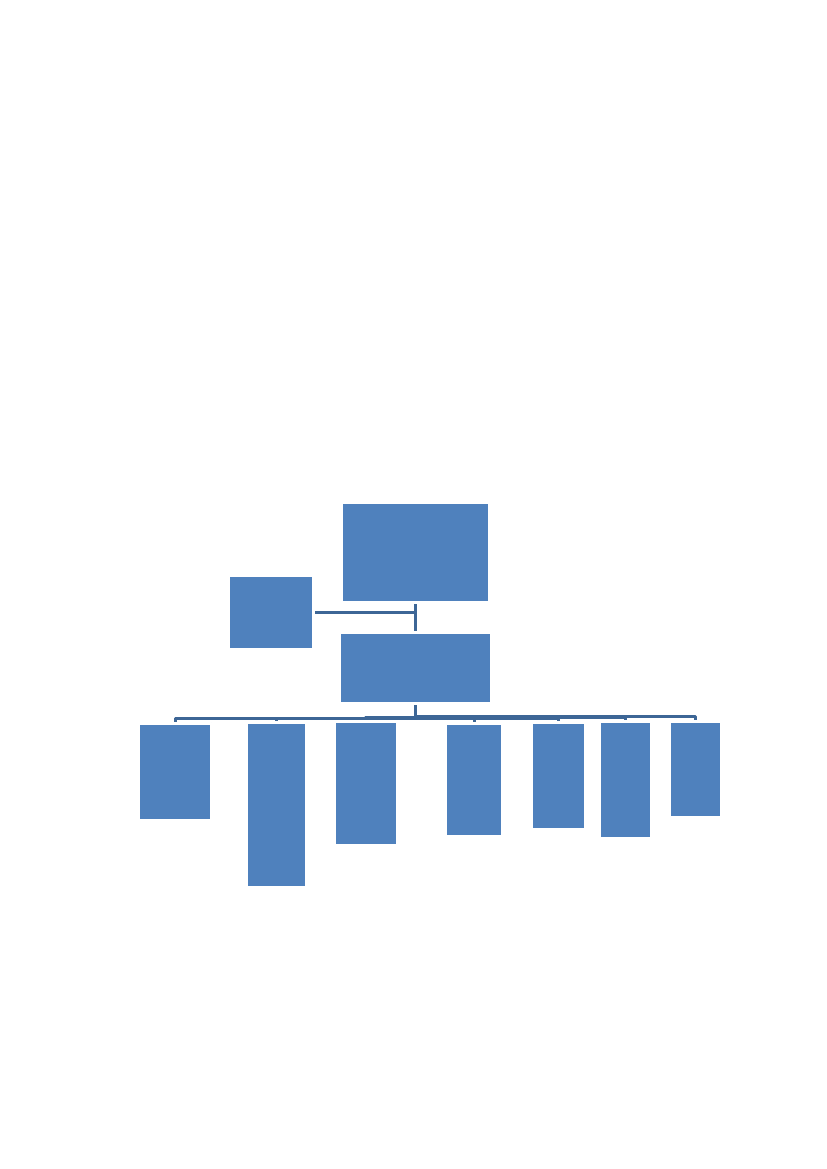

GGGI, as shown in the picture below, is organized with Seoul Headquarterand three overseas branches (Copenhagen, Denmark: 1 staff; London, England: 5staffs, in the process of preparing legal entity; Abu Dhabi, UAE: 6 staffs). SeoulHeadquarter consists of Management and Administration (7 staffs), Public-privatePartnership (7 staffs), Green Growth Planning and Implementation (20 staffs),Operation Department (9) and its total of 60 staffs.

[GGGI Organization Chart]

AuditorHur Dong Su(CEO of GSCaltex Corp.

Board of DirectorsDirectors(18 people includingExecutive Director)Chairman: Lars LokkeRasmussen( previous DenmakPrime Minister

Management committeeExecutive Director(Richard Samans, American)Deputy Executive Diretor(Vacant)

Management&AdministrationDirector(1)Staff(6)

InternationalCooperation,Public-Privatecooperation&TechnologySPM(2)staff(5)

GreenGrowthPlanning&ImplementationDirector(1)SPM(7)STAFF(12)

HR/FinanceCFO(1)Director(1)SPM(2)staff(5)

LondonRegionalOfficeDirector(1)SPM(2)staff(2)

Abu DhabiRegionalOfficeDirector(1)SPM(1)staff(4)

Copenhagen OfficeDirector(1)

12

4. GGGI Income and Expenditure Status

As presented in the figure 3, GGGI received supporting fund from KRW31,300 from Republic of Korea, Denmark (KRW 11,968million) Australia (KRW5,802 million), etc. Total amount of KRW 26,176 million funded by 6 othercountries. Out of KRW 57,476 million, the ratio of Korea’s fund takes part of 54.5%and separate incomes from private enterprise (financial institution, corporation,group, etc.) such as KRW 358 million in 2011 (European Bank for Reconstructionand Development), KRW 1,414 million until July 2012 (EBRD and the other 6institutions 5)), total amount of KRW 1,772 million.

Of these supported funds, if we take a look at execution break down ofKorea’s fund as presented in [table 4], GGGI executed KRW 23,421 million from2010.06 to 2012.07. Therefore, the execution rate is reaching 74.8% (payableaccount KRW 7,879 million from Korean fund as the end of 2012 July). Out of thisexecution rate, project management expenses shares 59.1% (KRW 11, 493 million),and the operation expenses shares 46.9% (10, 981 million).

13

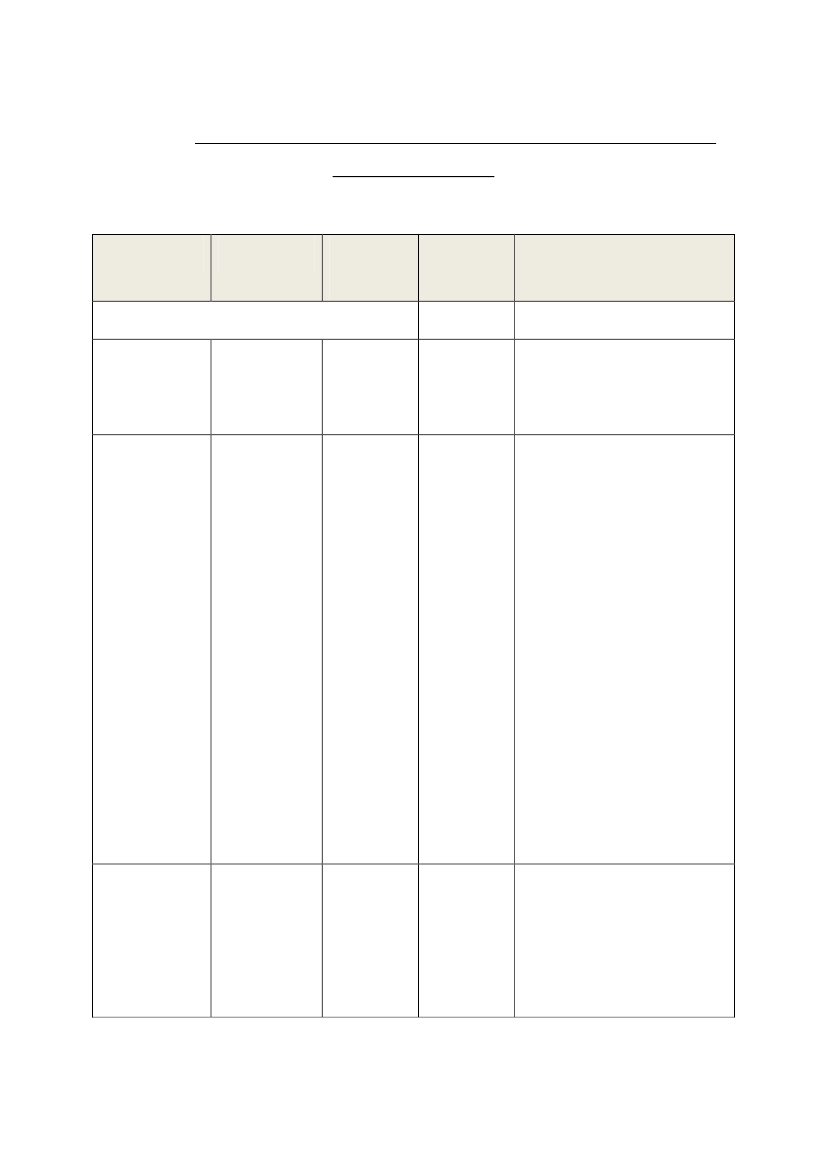

[Table 3] GGGI Revenue by country(Unit : million won, %, 1$=1087.00 won)

Total (%)Total▶ROK▶Foreign CountriesDenmarkUAEJapanGermanyAustraliaUK57,476 (100)31,300 (54.5)26,176 (45.5)11,9605,6841,1285835,8021,019

201011,36311,363

201120,88011,8009,0806,3111,5791,12862

2012(1-7)25,2338,13717,0965,6494,105

5215,8021,019

Data – Rearranged the data from GGGI’s

Outsourcing(8,834 million won), accounting for 76.9% of total projectexpenses (11,493 million won) is the biggest portion out of total expenses. Andthe personnel cost(6,067 million) contributes to 55.2 % of total administrativecost (10,981 million) which is second largest portion of total expenses.

[Table 4] Expense by line item (ROK support)(Unit : million won, %,1$=1087.00 won)

Total (%)Total23,421(100)

20104,082

201110,893

2012(1-7)8,446

14

▶Project costOutsourcing1)

11,493(49.1)8,8342)

1,6971,423

5,5334,025346

4,2633,386758023,2362,801435

Multilateral aid

4212,23810,981(46.9)6,0671.7272,2282742,3854172611,103

Other project cost▶Admin. CostPersonnel costRental, UtilitiesAsset purchase

1,1625,3602,8491,0311,125

Othercost

admin.959604355

▶IO ConversionData – Cash basis

947(4.0)

947

And GGGI appointed Richard Samans as Executive Director of GGGI in March13, 2011, who was the former Managing Director of World Economic Forum andmade a hiring contract with him for 2 years duration and his annual salary is$390,000.

National Assembly questioned that GGGI has been paying the compensationfor ED according to the employment contract but without compensation rulesand that he is paid higher than heads of other international organizations. In thiscontext, National Assembly has requested the Audit to BAI for examining the15

adequacy of compensation of Executives and employees.

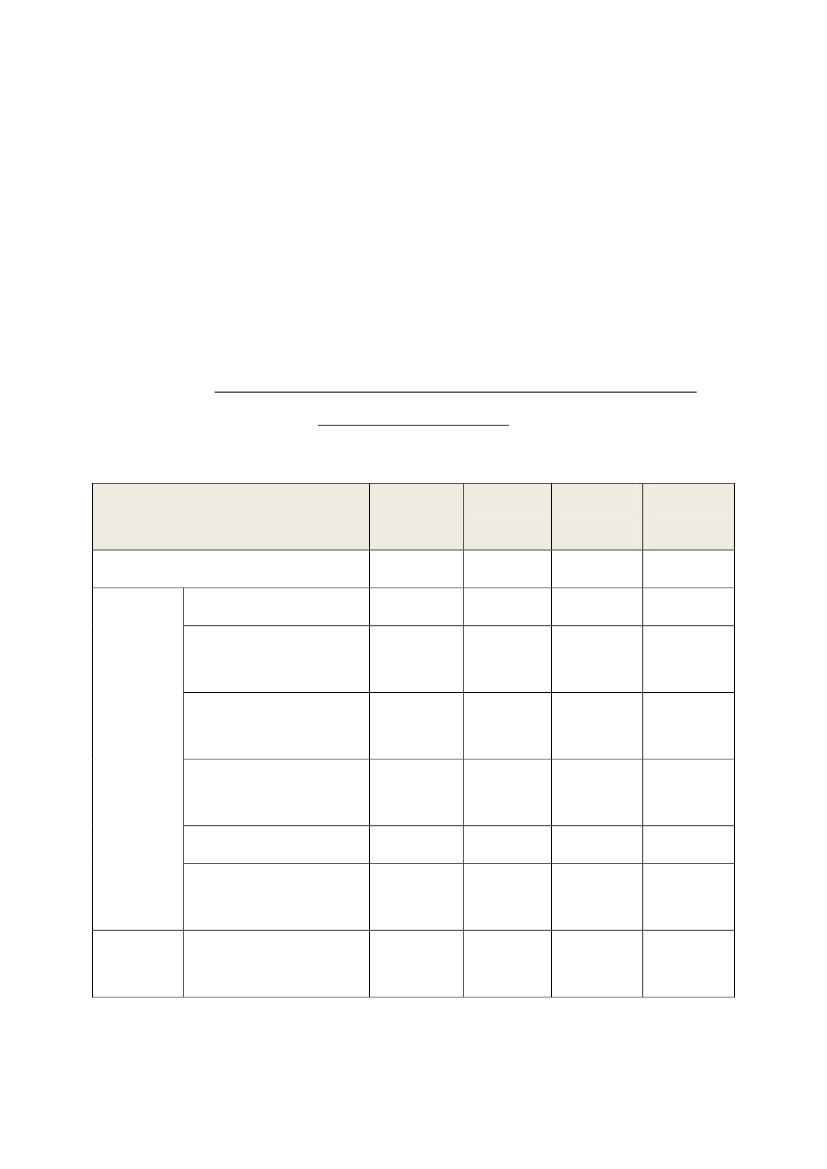

[Table 5] GGGI Salary Structure and Comparison with Actual Average ofAnnual Salary by PositionCassificationSalary structureMinimummaximum20,500DirectorSeniorManager &SeniorResearcherManager &StaffsSecretariat(1$=1087.00 won)Afterwards, GGGI didn’t reflected the salary structure, as shown above, inGGGI Rules on Compensation which has been implemented since 2010.11.01,however, when you see the actual average annual salary of employees who madeemployment agreements with GGGI, deputy directors are paid KRW 256,060,000,directorsarepaidKRW130,0120,000,seniormanagersandsenior13,7007,97039,80028,40014,200Actual Average annual salaryPositionamountExecutive44,070DirectorDeputy Director20,566Director13,012International9,658employeeNational8,449employeeInternational4,600EmployeeNational4,078employee--

3,4202,280

8,5403,980

researchers(foreigner) are paid KRW 96,580,000, managers and staffs are paidKRW 46,000,000, and they have not been exceeded the maximum limit which was16

set up at first.

Also, the annual salary of Executive director, Richard Samans, is about KRW440,700,000 exceeding the maximum wage of KRW 398,000,000 by KRW42,700,000 which was set up at first. However, his salary is at the level ofpresidents ofotherinternationalinstitutes andfoundations which were

comparable initially, and furthermore, he was paid higher then GGGI from hisprevious employer, WEF, and it was approved by submitting the information toBAI through this audit.

Meanwhile, GGGI pays allowances other than annual salary in accordancewith GGGI Budget Execution Guidelines, and they are classified as positionallowances, conferences allowances, business allowances, medical allowances andother welfare allowances. The Execution status by year and items are as belowtable.

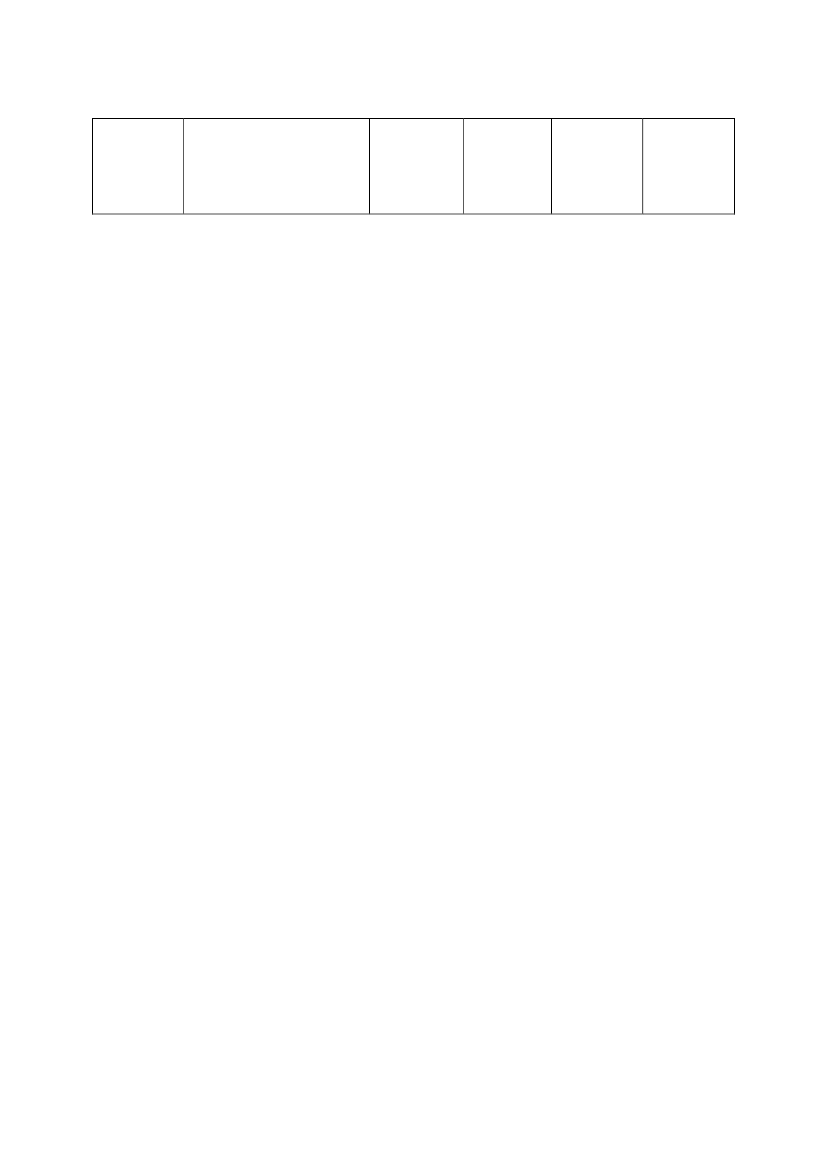

[Table 6] GGGI Allowance standard and execution status(amount unit: 1000)classificationPayment standard2010Execution status2011till Nov2012

17

Allowances other

than annual salary

Chairman: KRW3,000,000Executive Director:KRW2,000,000Secretariat: KRW200,000Driver: KRW200,000Dispatch: KRW1,500,000Internationally dispatch:KRW2,000,000KRW200,000 / monthKRW 200,000 / monthIn accordance withemployment agreementPrimary: KRW25,000,000Secondary: KRW30,000,000169,189Position allowances

26,400

48,600

39,216

Special allowances

9.500

16,000

11,433

Dispatch allowances

8,000

44,700

85,479

TransportationMeal AllowancesHousing AllowancesEducation allowancesOther operation

allowances

Non-executivesbusiness allowancesConferenceallowancesOther welfare

allowances

4,2006,000

68,34264,05160,518360,675

78,21375,413123,333227,521

KRW1,000,000 * 1 time

18,400

-

-

-

-

Medical expenses

1 person/KRW3,000,000*3persons1 person/KRW1,000,000/1yr1 person/KRW200,000/month

Medical check-upFitness & others(1$=1087.00 won)

In this regard, Ministry of Foreign Affairs and Trade requested of reserve fundto Ministry of Strategy and Finance for establishment of GGGI on April 30th 2010and recognized the essentialness of recruiting highly competitive global talents to18

carry forward a successful business of GGGI by suggesting compensations andbenefits at the level of international competitiveness.

Ministry of Foreign Affairs and Trade considered that the salary level ofpresidentsofinternationalinstitutesandfoundationsisbetweenKRW

420,000,000 and KRW 740,000,000, and decided to pay KRW 250,000,000 ~ KRW398,000,000 to executive directors, KRW 137,000,000 ~ KRW 284,000,000 todirectors; KRW 79,700,000 ~ KRW 142,000,000 to senior managers and seniorresearchers, and KRW 34,200,000 ~ KRW 85,400,000 to managers and staffs. Thissalary structure was resolved at the Cabinet council on May 18th 2010.

III. Audit FindingsOverview of Audit Findings❏As part of its “low-carbon green growth” policy, one of the nationaladministration projects, the Korean government intends to promote greengrowth on the global agenda and support the green growth of developingcountries.O Thus, it set up the Global Green Growth Institute (GGGI) on May 14, 2010as a non-profit foundation with the participation of countries includingDenmark and the UAE and vigorously pushed for its conversion into aninternational organization.

19

O On June 20, 2012, sixteen countries including Korea, Denmark, the UnitedKingdom, and Australia concluded the “Agreement on the Establishment ofthe Global Green Growth Institute” in Rio de Janeiro, Brazil. On October 18,2012, ratification of the Agreement by Denmark, Guyana, and Kiribati enteredinto force. As a result, the GGGI held its inaugural meetings on October 23,2012 as the first Korean-led international organization.❏In connection with this, the Board of Audit and Inspection conducted anaudit of the GGGI’s execution of its government-subsidized budget fromSeptember 17 to October 10, 2012 according to the National Assembly’s auditrequest on September 5, 2012. Its findings are summarized as follows:O In executing organizational operation expenses including personnelexpenses, the GGGI paid an excessive amount of housing and child educationallowances, inconsistent with its employment agreements. In addition, it paidvarious allowances including dispatched service allowance without clear andconcrete standards.O Resorting to outsourcing in implementing major projects, the GGGIconcluded optional contracts in some cases, which is against its internal rules.In other cases, it failed to carry out sufficient follow-up management of suchprojects. As a result, a number of projects were delayed beyond theircontractual period. This compromised efficiency and transparency of itsbudget execution.❏These problems are seemingly attributable to the fact that the GGGI, withinsufficient manpower, pressed ahead with its conversion into an internationalorganization over a short time span without formulating rules necessary fororganizational operation in advance, such as rules on management oforganization, human resources, and budget execution, in its establishmentprocess. This situation is also ascribable to ineffective guidance and supervision20

by the Ministry of Foreign Affairs and Trade, the agency in charge of overseeingthe GGGI.O The audit findings show that these defects need to be addressed toenhance transparency of the GGGI’s budget execution and ensure efficiency inits organizational operation so that it may effectively attain its goal ofpromoting global green growth.

1

Execution of Organizational OperationExpenses

[Problem]▪In executing organizational operation expenses including personnel expenses, theGGGI paid an excessive amount of allowances including housing, meeting attendance,and dispatched service allowances or applied unreasonable payment standards.

1

Unreasonable Payment of Housing and Child Education Allowances to

Executive DirectorBased on an open recruitment process, the Board of Directors of the GGGIdecided in July 2010 to appoint Richard SAMANS, the managing director of theWorld Economic Forum (WEF), as its executive director (standing director). Then, itconcluded an employment agreement with said person on March 13, 2011, underwhich it has been paying him housing and child education allowances, etc.

21

The employment agreement above provides that said person shall receive,from March 13, 2011 to March 12, 2013, a housing allowance of up to KRW 8.5million per month and a child education allowance of up to USD 18,000 perchild/year in addition to a basic annual salary of USD 390,000 (inclusive of taxes,insurance costs, etc.; equivalent to about KRW 440.7 million) as compensation forhis assumption of responsibility for operation of the GGGI as its executive directorincluding making reports to its Board of Directors.

① Payment of Housing Allowance

In the meantime, said person entered Korea on a business trip and stayed ata hotel for 44 days, during the period from March 20, 2011 to August 15, 2011(156 days), until he found residence in the country on August 15, 2011.

Out of personnel expenses, allowances are paid at an appropriate level, inaddition to basic annual salary, as needed depending on working and livingconditions and the like. As for the housing allowance, costs actually incurred byan expatriate when he or she changes residence in the employment processshould be paid.

Accordingly, the GGGI should have paid the housing allowance to saidperson under its payment limit of KRW 8.5 million per month until he leased ahouse in Korea on August 15, 2011 to reside in the country, based on materialsevidencing his actual housing costs such as hotel bills during his sojourn in the22

country during said period, including receipts.

However, the GGGI fully paid him a total of KRW 43,322,580 [calculated on apro-rata daily basis for March (19 days) and August (15 days)] as a housingallowance for 156 days in total by applying a maximum monthly payment limit ofKRW 8.5 million stipulated in said employment agreement without ascertainingthe housing costs actually incurred by him while he stayed in Korea during saidperiod.

As a result, an excessive amount of KRW 39,481,230 was paid to said person,who stayed at a hotel instead of renting a house to reside in the country.

② Payment of Child Education Allowance

Article 11(2) of the GGGI Compensation Regulation stipulates that anemployee with a child who needs to attend an international elementary school isentitled to a child education allowance of up to KRW 25,000,000 per year.

In concluding an employment agreement with said person on March 13,2011, the GGGI determined that it would pay such child education allowance inthe amount of up to USD 18,000 per child/year.

23

Accordingly, the GGGI should have reimbursed out-of-pocket expenses as thechild education allowance based on evidentiary materials within a limit set in theemployment agreement, causing any excess to be borne by said person. Inconcluding a modified employment agreement based on the judgment that theamount of the child education allowance set forth in the original employmentagreement was too small, the GGGI should have provided that the childeducation allowance of up to KRW 25,000,000 per child/year shall be paid to saidperson.

However, the GGGI, unlike the employment agreement with said person, puthis child education allowance per child at KRW 32,150,000 on August 31, 2011,KRW 12,962,000 more than the contractual upper limit of KRW 19,188,000 (USD18,000 × then-effective exchange rate of KRW 1,066/dollar). Thus, the GGGI paida child education allowance of KRW 64,300,000 to said person for his twochildren, paying KRW 25,924,000 in excess.

In the meantime, the GGGI, in concluding a modified employment agreementwith said person on June 15, 2012, decided to pay said person a child educationallowance of KRW 30,000,000 per child, KRW 5,000,000 above the KRW25,000,000 limit per child as provided in the GGGI Compensation Regulation. Inaddition, the GGGI determined that such amount would apply retroactively fromMarch 13, 2011 when the original employment agreement was signed.Action to Be Taken: The chairman of the Global Green Growth Institute (GGGI)should prevent a housing allowance from being paid to its executive directormerely based on its monthly payment limit without ascertaining actual housing24

costs. In addition, he is advised to ensure that payment of an excessive amountof a child education allowance in a manner inconsistent with an employmentagreement and retroactive application of such amount based on conclusion of amodified employment agreement, in violation of the GGGI CompensationRegulation, will not occur again.[Admonition]

2

Unreasonable Payment of Various Allowances including Dispatched

Service Allowance

The GGGI has been paying many different allowances, including thedispatched service allowance, the housing allowance, and government employeepension contributions, to its officers and employees in accordance with the GGGICompensation Regulation or an employment agreement, etc.

In connection with this, the GGGI, as a non-profit foundation registered withthe Ministry of Foreign Affairs and Trade, has been receiving governmentcontributions from the Korea International Cooperation Agency to finance itsoperation. Accordingly, the GGGI should have formulated reasonable rules on thepayment targets, requirements and levels concerning employee wages andallowances in line with the purpose of its establishment, and executed such costsin an efficient fashion based on such rules.

① Payment of Dispatched Service Allowance25

Articles 3(1)5 and 14(1) of the GGGI Compensation Regulation provide that adispatched service allowance of up to KRW 1.5 million may be paid to a workerassociated with any other organization and working for the GGGI for a month orlonger.

Therefore, only a worker providing full-time service to the GGGI for at leastone month under a dispatch order from his or her organization is entitled to thedispatched service allowance. Thus, the GGGI should not have paid thedispatched service allowance to any worker who did not receive a dispatch orderfrom his or her organization and simply assisted the GGGI on a non-full-timebasis.

However, the GGGI paid a total of KRW 12 million as a dispatched serviceallowance (KRW 1 million per month), in addition to an allowance of KRW400,000 for a post per month, to Yeon-Chul YOO, an employee of the Ministry ofForeign Affairs and Trade (currently, an officer at the Ministry of Environment),who was dispatched in the capacity of the head of the International CooperationTeam of the Presidential Committee on Green Growth and took charge ofsupporting establishment and operation of the GGGI, on grounds that he servedas a temporary CFO from June 2010 to May 2011, even though he had beenreceiving an allowance (monthly allowance for a post) from the PresidentialCommittee on Green Growth and was not dispatched to the GGGI again.Concerning Chan Ho PARK, the head of the Global Legal Research Center ofthe Korea Legislation Research Institute, the GGGI paid him KRW 2 million inDecember 2010 as advisory fees and also paid KRW 20 million in total (KRW 126

million per month) as a dispatched service allowance on grounds that heprovided legal advice from June 2010 to January 2012, even though he was notdispatched to, nor worked for the GGGI on a full-time basis, until he took a leaveof absence in February 2012.

② Payment of Meeting Attendance Allowance Before Establishment

Meeting attendance allowances should be paid based on materialsevidencing actual summoning of a meeting, the date of attendance, etc. to theextent that there exist rules on payment targets, standards, amount, etc.

Despite the fact that the GGGI has no such rules allowing payment ofmeeting attendance allowances, it paid KRW 9 million in total (minimum KRW 1.8million to maximum 2.4 million) on December 30, 2010 as indicated in [Table 7]to four government employees, who carried out their given duties, in the name ofpre-establishmentmeetingattendanceallowanceswithoutcollectingany

evidentiary materials on the frequency, time, and attendees of meetings ongrounds that they laid out a plan to set up the GGGI and formulated a staffingand financing method prior to establishment of the GGGI.

27

[Table 7] Payment of Meeting Attendance Allowances Prior to Establishmentof the GGGI(Unit: KRW,1$=1087.00 won)DescriptionPayeeTotalSang- Office of the President; ahyupKIM▪Meetingsprior toestablishmentof the GGGIYeon-ChulYOOSungbinYIMWonnon-standing director ofthe GGGI▸Time,Presidential Committeeon Green Growth2,400,000frequency, etc. ofmeetingsunidentifiableOffice of the President2,400,0002,400,000AssociationAmount9,000,000Remarks

Presidential Committee

JANG on Green Growth

1,800,000

Source: Recompilation of materials submitted by the GGGI, etc.

③ Payment of Housing Allowance

According to the GGGI Budget Execution Guidelines (June 17, 2011), ahousing allowance may be paid to foreign expatriates stationed in Seoul. In28

addition, the GGGI Overseas Leased Housing Management Guidelines (June 17,2011) stipulate that a housing allowance equivalent to rent which is stated in alease contract shall be paid to an employee working for its overseas branchunder the maximum limit of monthly rent payment.

Out of personnel expenses, allowances are paid at an appropriate level, inaddition to basic annual salary, as required depending on working and livingconditions, and the like. As for the housing allowance, the GGGI should reimburseout-of-pocket expenses under a certain limit according to clear standards, causingany excess to be borne by the employee concerned.

Despite this situation, the GGGI paid KRW 63,400,283 in total (KRW 5.2million per month) on a pro-rata daily basis from June 14, 2011 to June 13, 2012to Tae Yong JUNG, the former vice executive director who relocated from Manila,Philippines to Seoul, on the basis of his employment agreement providing forpayment of a housing allowance of up to KRW 5.2 million per month withoutconfirming the actual amount of rent and specifying the targets, limits, methods,etc. of housing allowance payment in applicable rules including the GGGI BudgetExecution Guidelines.

In addition, the GGGI paid housing allowances (minimum KRW 1.25 million ~maximum KRW 8 million per month) to seven out of ten foreign expatriatesstationed in Seoul based on actual rent receipts, unlike the vice executive directorabove. In contrast, the GGGI has been paying no housing allowance to the29

remaining three expatriates without any justifiable cause.

Besides, four employees working for the branches in Copenhagen, Denmark,and London, the United Kingdom had respectively been living in Denmark andthe United Kingdom before they entered into an employment agreement with theGGGI. Although they did not change their residence due to such employmentagreement, the GGGI, in breach of said Overseas Leased Housing ManagementGuidelines, paid a fixed monthly amount of USD 1,500 to 2,000, i.e. USD 57,542 intotal (equivalent to KRW 61,413,639) as housing allowances from June 2011 toSeptember 2012, failing to ascertain whether they had actually leased theirhousing.

There exist concerns that such inconsistency in payment of housingallowances might lead to inefficient execution of a relevant budget or undermineequality of treatment among employees.

④ Payment of Government Employee Pension Contributions

The GGGI Compensation Regulation provides that the GGGI shall pay avariety of allowances including the allowance for a post, dispatched serviceallowance, business promotion expenses, lunch expenses, and transportationexpenses in addition to basic pay. The Regulation does not define governmentemployee pension contributions as a type of allowance that must be paid in30

addition to basic pay, which means that they should be deducted from individualemployees’ basic pay. Accordingly, the GGGI should not have concluded anemployment agreement to the effect that such contributions would be paid as anallowance payable on top of basic pay.However, the GGGI entered into an employment agreement on March 29,2011 with Joo Sueb LEE, who took a leave of absence from the Ministry ofStrategy and Finance, to the effect that it would pay KRW 330,000 a month asgovernment employee pension contributions, in addition to basic monthly pay ofKRW 7.9 million and KRW 200,000 in lunch and transportation expensesrespectively. Under the agreement, the GGGI paid him KRW 5.94 million in totalas government employee pension contributions from April 2011 to September2012.

Action to Be Taken: The chairman of the Global Green Growth Institute (GGGI)is advised not to apply its budget inefficiently by paying dispatched serviceallowances, meeting attendance allowances, housing allowances, and governmentemployee pension contributions at his sole discretion or in an inconsistentmanner, in breach of the GGGI Compensation Regulation, etc., or without anyrules providing rationale for their payment.[Admonition]

3

Unreasonable Provision of Exclusive Vehicle and Corporate Credit Card to

Non-Standing Director

The GGGI operates the Board of Directors consisting of 17 non-standing31

directors (including the chairman) and an executive director, who is a standingdirector, to support its activities.

Since a non-standing director is not engaged in affairs of the GGGI on a full-time basis, it is reasonable to provide financial assistance to such director only tothe extent that business needs arise. Even in case where the GGGI supportsactivities by a non-standing director out of business needs, it should execute itsbudget transparently according to rules specifying the rationale, targets, etc. ofsupport.

Article 19 of the GGGI Compensation Regulation provides that exclusivevehicles shall be supplied to the chairman and executive director only and that upto KRW 3 million’s monthly compensation be paid to a chauffeur for theiroperation.

Accordingly, it is not allowed to provide exclusive vehicles to any non-standing director other than the chairman or executive director and renderfinancial assistance including compensation for a chauffeur.

Nonetheless, the GGGI rented a YF Sonata (total rent of KRW 3.85 million) forover five months from April 20, 2011 to September 30, 2011 and allocated thevehicle to Sang-hyup KIM, a non-standing director (then Secretary and currentSenior Secretary to the President for Green Growth and Environment),not entitled32

to an exclusive vehicle, for his exclusive use. Thus, the GGGI disbursed KRW27,472,066 in total as compensation for a chauffeur and maintenance costs of thevehicle.

In addition, the GGGI enacted the GGGI Corporate Credit Card Regulation inNovember 2010 (date unknown). Said Regulation stipulates that individualcorporate credit cards shall be provided to the chairman, executive director, vice-executive director, CFO, and a director and that in the event of incurrence ofbusiness promotion expenses, etc. based on use of a corporate credit card, theperson concerned shall submit evidentiary documents clearly stating details ofits use including the purpose, time, place, and target of disbursement to ensuretransparent use of a corporate credit card.

The GGGI formulated said Regulation, but failed to enforce it, asdemonstrated by the fact that it issued an individual corporate credit card to thenon-standing director above, who is not eligible to such card under saidRegulation. Thus, it allowed the non-standing director to disburse businesspromotion expenses in the amount of KRW 31,507,694 over 123 occasions fromAugust 23, 2010 to September 5, 2012.

Besides, the GGGI did not collect evidentiary documents specifying details ofits use (purpose, time, place and target of disbursement, etc.) regarding 108payments made prior to January 27, 2012. Out of those payments, 73 paymentswere fully reimbursed without confirming whether they were actually made for a33

purpose related to the GGGI’s business affairs in a situation where credit card billswere submitted in lieu of evidentiary documents.

Action to Be Taken: The chairman of the Global Green Growth Institute (GGGI)should ensure that any non-standing director not entitled to a vehicle for hisexclusive use shall not be provided with such vehicle. In addition, the chairman isadvised to implement the Corporate Credit Card Regulation as soon as possibleand handle matters pertaining to issuance and management of corporate creditcards thoroughly to warrant appropriate management and control of their use.[Admonition]

2

Disbursement of Project Costs

[Problem]▪In performing outsourcing projects to help developing countries formulate greengrowth development strategies, the GGGI executed its budget in an inefficientmanner through reckless conclusion of optional agreements and sloppy managementof those projects.

1

Unreasonable Conclusion and Management of Outsourcing Agreements

With a view to formulating and supporting green growth plans of developing34

countries, the GGGI entered into twenty outsourcing agreements on the East AsiaClimate Partnership (EACP) initiative and five outsourcing agreements on researchfrom September 28, 2010 to September 7, 2012. Since then, it has poured KRW9.622 billion into the projects.

① Selection of Outsourced Entities and Conclusion of Agreements

Paragraphs 1 and 3 of Chapter I and Paragraph 6 of Chapter IV of the GGGIProcurement Regulation (March 31, 2011) provide that open competition amongbidders is required in principle to ensure transparency and openness of contractconclusion procedures. However, conclusion of an optional agreement ispermitted on an exceptional basis if the amount of outsourcing is no more thanUSD 100,000 or if a partner which signed an MOU with the GGGI is suitable forthe purpose and scope of a project.

As a non-profit foundation associated with the Ministry of Foreign Affairs andTrade, the GGGI has been a beneficiary of government contributions through theKorea International Cooperation Agency. Therefore, when the GGGI pursues anoutsourcing project, it would be desirable to apply related rules of the KoreaInternational Cooperation Agencymutatis mutandiseven prior to formulation ofthe said Regulation, selecting an entity based on open competition if possibleand executing a budget fairly and transparently.

35

In carrying out outsourcing projects, however, the GGGI signed all 25outsourcing agreements concluded from September 2010 to September 2012 inthe form of an optional agreement, including a USD 4,250,000 (equivalent toabout KRW 4.7 billion) outsourcing agreement with Climate Works, a USfoundation, entered into on September 28, 2010, as indicated in Attached Table 1,“Status of Conclusion and Management of Outsourcing Agreements Concerningthe East Asia Climate Partnership (EACP)” and Attached Table 2, “Status ofConclusion and Management of Outsourcing Agreements Concerning Research.”

Specifically, the GGGI concluded five optional agreements before enactmentand enforcement of the GGGI Procurement Regulation (March 31, 2011). Evenafter enactment and enforcement of the Regulation, which mandates opencompetition in principle, the GGGI signed eleven optional agreements on groundsthat their respective contractual amount is no more than USD 100,000 and fiveoptional agreements respectively worth over USD 100,000 with government-funded research institutes associated with the National Research Council forEconomics, Humanities and Social Sciences (NRCS) on grounds that the GGGIconcluded an MOU with the NRCS on December 23, 2010. As for the remainingfour contracts, the GGGI entered into optional agreements even though theirrespective contractual amount is over USD 100,000 and there was no clearrationale to conclude an optional agreement as stipulated in said Regulation.

As stated above, the GGGI signed optional agreements for all outsourcingprojects that it pushed for with a government-subsidized budget. Thus, there existconcerns that fairness and transparency regarding selection of an outsourced36

entity may be compromised.② Management of Outsourcing

Paragraph 15 of Chapter II of the GGGI Procurement Regulation provides thatin concluding an agreement, it is necessary to clarify the scope of service to beperformed, goods to be supplied, rights and obligations of a supplier orcontractor, finaldeliverables, and annexed documents including financial

statements and evidentiary payment documents.

Accordingly, the GGGI has to clarify the contractual period, scope of researchservice, etc. in concluding an outsourcing agreement so as to ensure a highquality of such service. Then, it must thoroughly manage progress in researchservice so that research service may be completed within the contractual periodand its results be utilized in a timely fashion.However, the research service for the Mongolia-PPP Financing SchemeAnalysis regarding which the GGGI entered into an outsourcing agreement withSamjong KPMG on November 17, 2011 has not been completed seven monthsafter its contractual period (November 2011 to February 2012). As shown inAttached Table 1, “Status of Conclusion and Management of OutsourcingAgreements Concerning the East Asia Climate Partnership (EACP)” and AttachedTable 2, “Status of Conclusion and Management of Outsourcing AgreementsConcerning Research”, services have not been completed two to seventeenmonths after the contractual periods for 17 out of 25 research serviceagreements concluded by the GGGI with a government-funded budget. In spite37

of this situation, the GGGI has not taken any measures including collection ofliquidated damages.Such sloppy management of contractual performance resulted in failures tocomplete research services within contractual periods and to take advantage oftheir results in a timely manner.

Action to Be Taken: The chairman of the Global Green Growth Institute (GGGI)should ensure that contracts are concluded in an open competition processaccording to applicable rules for fair and transparent execution of its researchservice budgets. In addition, he is advised to carry out seamless follow-upmanagement of research service projects including prior review of the necessityof a project and imposition of liquidated damages so that outsourcing servicesmay be completed in a timely manner and its budget be executed efficiently.[Admonition]

2

Unreasonable Conclusion and Management of Agreement Concerning

Ethiopia Household Irrigation Technologies Research Service

With respect to the Ethiopia Household Irrigation Technologies project(amount: USD 555,000 which is equivalent to KRW 618,270,000, period: December24, 2010 to April 24, 2011), the GGGI concluded a research service agreementwith∆∆∆on December 24, 2010, and subsequently implemented the project.

38

① Conclusion of Agreement

The GGGI learned in about November 2010 (date unknown) that the Bill &Melinda Gates Foundation(“Gates”) and Mckinsey & Company Inc.(“Mckinsey”)had been pursuing a project related to Ethiopian irrigation facilities. The GGGIreceived a proposal from the Gates Foundation that it should participate in theproject undertaken by Mckinsey.

According to the written proposal that the GGGI received from Mckinsey onNovember 27, 2010, said project was to be conducted in phase A and B (sixweeks in total including three weeks for phase A and B respectively). Phase A(three weeks) would cost USD 250,000 while phase B (three weeks) would costUSD 305,000 after completion of phase A. However, the USD 250,000 budgetrequired for phase A included tasks for phase B.

Under the circumstances, the GGGI, upon examination of said proposal,produced a business plan to the effect that both phase A and B would becompleted during a six-week period at the cost of USD 250,000 (equivalent toKRW 278,500,000). It submitted the plan to its FacCom on December 4, 2010, andthe plan was approved without any modification on December 9, 2010.

In the meantime, Article 12(3)1, 12(3)11, 12(4) and 21(1) of the GGGI’sArticles of Incorporation, its budget and annual basic business plan should be39

approved by the Board of Directors or the FacCom installed in the Board ofDirectors.

Therefore, the GGGI has to ensure efficient execution of a budget inconducting outsourcing by scrutinizing a proposal submitted by a service provider,the scope of service, rationale for computation, etc. In addition, it should push fora project with approval from the FacCom, etc. and obtain approval again in theevent of any modification.

On December 23, 2010, the GGGI received a draft contract from Mckinseystating that phase A (three weeks) of the project above would be performed atthe cost of USD 250,000. Thus, it requested its legal advisor (Chan Ho PARKassociated with the Korea Legislation Research Institute) to review the details ofthe contract.

The legal advisor named Chan Ho PARK opined that it was unclear whetherthe consideration for service (USD 250,000) as specified in the proposal originallysubmitted by Mckinsey is for phase A only or for both phases A and B. He alsosaid that the FacCom had approved a plan to conduct phase A and B (six weeks)at the cost of USD 250,000. Noting that the draft contract stated that only phaseA (three weeks) would be performed at the cost of USD 250,000, he said thatconsideration of USD 250,000 is excessive for three weeks of service. Thus, hesuggested that the contractual period be prolonged to four months and thatboth phase A and B be performed at the cost of USD 555,000. He went on to say40

that such change would require re-approval by the FacCom.

However, the GGGI prolonged the contractual period to four months onDecember 24, 2010 without obtaining the FacCom’s approval of such modification.With the contractual amount increased by USD 305,000, the GGGI concluded aUSD 555,000 optional agreement with Mckinsey.

Said agreement on research service provides that the final payment shall bemade in two months after launch of the project and that the actual period ofservice shall be six weeks. This indicates that the contractual period wasnominally prolonged to four months.

② Management of Research Service

In addition, said agreement on research service stipulates that interim, final,and financial statements should be submitted by set deadlines to attain the goalof the project and that payments should be made accordingly.

Therefore, the GGGI should have thoroughly managed the research service sothat it could be performed smoothly as provided in the agreement, ensuringtimely utilization of service results.

41

Mckinsey, the counterparty to the agreement, did not request payment of adeposit upon commencement of the agreement unlike the details of theagreement. Besides, it failed to submit an interim statement by January 10, 2011,a set deadline. However, the GGGI did not take any actions to ascertain progressin service including confirming whether Mckinsey had begun to perform theagreement or identifying the reason for its failure to submit an interim statement.

After Mckinsey submitted a final statement on March 4, 2011, the GGGIrequested that the statement be modified and complemented four times asspecified in Table 8 on grounds that its content was not satisfactory. However,Mckinsey failed to appropriately modify and supplement the statement. As aresult, a final statement had yet to be produced and published as of September17, 2012, the commencement date of this audit.

[Table 8] Developments Concerning Mckinsey’s Submission of ResearchService Statements and Their Modification/SupplementationDateDescription‧Submission of the 1st finalMarch 4, 2011 Mckinsey statement; invoice for down payment(in full)‧Request for submission of anMarch 15, 2011GGGIinterim statement, financial statement,etc.42

Officer in Charge

-

Dr. Okju JEONG

March 25, 2011

GGGI

‧Request to modify and supplementthe 1st final statement‧Submission of the 2nd finalstatement‧Request to modify and supplementthe 2nd final statement‧Submission of the 3rd finalstatement

June 10, 2011

Mckinsey

-

August 3, 2011

GGGI

Dr. Okju JEONG

September 7,2011

Mckinsey

-

September 27,2011

GGGI

‧Request to modify and supplementthe 3rd final statement

Tae Yong JUNG,former viceexecutive director

About October2011

Mckinsey

‧Submission of the 4th finalstatement‧Request to modify and supplementthe 4th final statement‧Submission of the 5th finalstatement

-

GGGIAbout April2012Mckinsey

Dr. Seong CheolKANG

-

Source: Recompilation of submitted materials including four GGGI employees’confirmation letters and e-mails

As shown above, the GGGI failed to manage a research service project43

appropriately. This prompted the project to pass its contractual deadline foreighteen months. Thus, the GGGI could not utilize its project outcomes in atimely manner, which attests to its failure to efficiently apply a budget.

Action to Be Taken: The chairman of the Global Green Growth Institute (GGGI)is advised to thoroughly review research service proposals and agreements andnot to increase a contractual amount without obtaining approval by the FacCom.In addition, the chairman is requested to completely examine the final statementconcerning the Ethiopia Household Irrigation Technologies research service andsettle related expenses.[Admonition]

The Minister of Environmentis advised to urge caution to personnel who werenegligent in performing duties concerning contract conclusion in connection withpursuit of said project.[Admonition]

The presidential chief of staffis advised to urge caution to personnel who werenegligent in performing duties concerning coordination in connection withpursuit of said project.[Admonition]

44

3

Unreasonable Conclusion and Management of Agreement Concerning

Research Service for Formulation of Low-Carbon Development Plan inShandong Province

On December 30, 2010, the GGGI concluded an agreement on “researchservice for formulation of a low-carbon development plan for Shandong Province,China” (amount: USD 500,000 equivalent to KRW 557,000,000, period: December31, 2010 to September 30, 2011) with ���� University in China. The service wascompleted on March 22, 2012.

On November 10, 2010, the GGGI held the fourth meeting of its Board ofDirectors and decided to pursue said outsourcing project by receiving aninvitation letter from Shandong Province and to convert it into an R&D programin the event of a failure to receive such letter. As receipt of an invitation letterfrom Shandong Province was delayed, the GGGI summoned the FacCom onDecember 4, 2010 and decided to change said project into an R&D program onthe premise that it obtained a promise by an officer at the level of the Governorof Shandong Province.

As specified above, said outsourcing project is to draw up a low-carbondevelopment plan for Shandong Province. Since smooth implementation of theproject required cooperation and support by Shandong Province, the GGGIshould have pressed for the project after obtaining a promise from ShandongProvince and then determining the purpose and details of the project, scope of45

service, contractual amount and period, etc.

Without securing a promise from Shandong Province, i.e. a precondition forpursuit of said outsourcing project, the GGGI converted the project into an R&Dprogram on December 30, 2010 and pushed for the program. On January 10,2011, it paid USD 150,000 (equivalent to KRW 167,100,000) as a deposit.In the meantime, Tsinghua University continuously sought to conclude anagreement with Shandong Province from about March 2010 (accurate dateunknown)tocollectbasicmaterialsandgarnersupportnecessaryfor

performance of said outsourcing project. However, it failed to reach an agreement.

Against this backdrop, the GGGI decided to merely receive a technical reportnot reflecting actual research and analysis findings on Shandong Province basedon consultation with Tsinghua University, instead of a research deliverableconcerning formulation of a low-carbon development plan for Shandong Province,which is the original purpose of the project. On November 11, 2011, the GGGIreceived said technical report from Tsinghua University. On November 18, 2011,the GGGI held a meeting of its Management Committee and decided to put theproject to an end and to make an interim payment of USD 150,000 additionally.On January 17, 2012, the GGGI paid USD 150,000 to Tsinghua University withoutreceiving a financial statement, which was contractually required and necessaryfor settlement of project costs.

As explained above, said outsourcing project was concluded even without46

settlement of project costs concerning the amount already disbursed. In addition,the technical report that the GGGI received from Tsinghua University, thecounterparty to the agreement, on November 11, 2011 remains unutilized as ofSeptember 17, 2012, over ten months after its submission. This implies that itsbudget has not been efficiently executed.

Action to Be Taken: The chairman of the Global Green Growth Institute (GGGI)should not pursue outsourcing when a prerequisite for outsourcing such as apromise by the agency concerned has not been met.[Admonition]

4

Unreasonable Conclusion and Management of Agreement Concerning

Dispatch of Samjong KPMG Experts

On September 6, 2011, the GGGI concluded agreements (amount: KRW 55million per person (two persons) and KRW 87 million per person (one person),KRW 197 million in total) to the effect that Samjong KPMG Advisory Inc.(hereinafter referred to as “Samjong”) should dispatch three experts for 26 weeksfrom September 15, 2011 to February 15, 2012 for benchmarking and researchpertaining to “response to climate change issues” and “promotion of recyclableenergy” in Cambodia, the UAE, etc.

47

① Conclusion of Agreement on Dispatch of Experts

Paragraphs 1 and 3 of Chapter I and Paragraph 6 of Chapter IV of the GGGIProcurement Regulation (March 31, 2011) provides that open competition isrequired in principle when concluding a contract to ensure transparency andopenness of the related procedures. However, conclusion of an optionalagreement is permitted in certain cases such as when the amount of contractualservice is no more than USD 100,000.

Paragraph 5 of Chapter III of said Regulation stipulates that for conclusion ofa consulting agreement, three to six qualified and experienced consultingcompanies shall be selected as final candidates after a public announcement. Inaccordance with such Regulation, the GGGI should undergo a transparentcontract conclusion process.

Concerning dispatch of three experts for which the GGGI concludedagreements on September 6, 2011, the contractual date, dispatching company,time, and period of dispatch, etc. were the same. Furthermore, the areas ofresearch were similar to each other and the combined contractual amount wasKRW 197 million. Therefore, it was reasonable to conclude such agreements bymeans of open competition in accordance with said Regulation. However, theGGGI entered into separate optional agreements.

48

② Agreements on Dispatch of Experts and Their Follow-Up Management

Paragraph 15 of Chapter II of said Procurement Regulation provides that inconcluding an agreement, it is necessary to clearly define the scope of service tobe performed, goods to be supplied, rights and obligations of a supplier orcontractor, finaldeliverables,and annexed documents including financial

statements and evidentiary payment documents. Paragraphs 1 and 3 of ChapterIII of the same Regulation stipulates that in employing a consultant to receiveconsulting service and professional advice, the GGGI should ensure clear, high-quality deliverables. In addition, estimation of consulting costs should be basedon resources required for task execution including time input, etc.

In the meantime, two experts (A and B) dispatched according to theirrespective agreements are participants in the “Kazakhstan national green growthplan” for which the GGGI concluded a service agreement with Seung Hyun KIMand Oksu LEE (amount: 490,000 euro equivalent to KRW 7 million). The term ofsaid service agreement is from September 15, 2011 to 2012. 9. 14, which overlapswith the period of said dispatch agreements (September 15, 2011 to February 15,2012).

Accordingly, the GGGI should have entered into dispatch agreements afterclarifying the ratio of performance of duties, time input, etc. of said twodispatched experts irrespective of whether their participation in said researchservice is excluded or acknowledged. With respect to dispatched experts, the49

GGGI should have formulated a reasonable management plan, clearly specifyingservices to be performed or deliverables to be produced.

When it concluded said agreements on dispatch of experts on September 6,2011, the GGGI did not clarify the ratio of performance of duties, time input, etc.,nor formulated a reasonable management plan. Thus, said experts reported forduty at the GGGI only for about three days a week during the 26-week periodfrom September 15, 2011 to February 15, 2012 to attend internal meetings andcollect necessary materials (they worked for their own company for the remainingperiod). They failed to produce clear and separate research deliverables.

Concerning this situation, the GGGI suggested that they had preparedmaterials necessary for GGGI-Cambodia advisory meetings held in December2011 and March 2012, presenting them as deliverables of expert researchactivities. However, they were prepared not by the experts, but by eachorganization on specific subjects. Other materials submitted by the GGGI canhardly be deemed concrete research deliverables reflecting their professionalability.

Considering this situation across the board, it is believed that the GGGI failedto serve the original purpose of the project, i.e. obtaining high-level researchdeliverables by utilizing dispatched experts.

50

Action to Be Taken:The chairman of the Global Green Growth Institute (GGGI) isadvised not to conclude separate optional agreements when it enters intoagreements on dispatch of experts with a similar purpose with the same company.In addition, the chairman is urged to ensure that dispatch of experts will translateinto clear deliverables and to thoroughly conclude and manage agreements ondispatch of experts by producing a clear budget based on time input, etc. whenthe same expert is utilized for overlapping projects in order to prevent anybudget waste.[Admonition]

5

Improper Outsourcing of Research on Planning for Low-Carbon Green

Growth and Development of Brazil and Two Other CountriesSeptember 28, 2010, the GGGI outsourced a research project to the UnitedStates’ Climate Works Foundation (hereinafter referred to as “CW”) in order todevise a plan for the low-carbon growth and development of Brazil, Ethiopia, andIndonesia (hereinafter referred to as the “Development Plan”) [amount: USD4,250,000 (or KRW 4.7 billion); period: June 2010 (no date is indicated in theagreement) – December 31, 2010](hereafter in this translation of this sectionoften referred to as the “Research (Service)”, “Outsourcing,” and “Project”respectively),and it received a financial report from CW thereon on February 15,2011.

As a nonprofit foundation that is registered with the Ministry of ForeignAffairs and Trade and of which operation is funded by the government in theform of contributions from the Korea International Cooperation Agency (KOICA),the GGGI should formulate rules on agreements including the details of the tasks,51

budget calculations and adjustments, execution periods, late charges, and the likewhen pursuing an outsourcing project; comply with the rules; and ensure the fairand transparent execution of the budget, but it failed to do so.

When the GGGI pursues a service outsourcing agreement, it should clearlyindicate when to commence the project and obtain signatures of the people withappropriate authority after all the prerequisites for the performance of the serviceare ready. The GGGI also needs to enter into an agreement in a manner thatensures the responsible execution of the budget by receiving the grounds forcost calculations and, when the project ends, documentary evidence to ensure anaccurate settlement.

However, when the GGGI pursued a service outsourcing agreement on theThree Country Development Plan with CW (hereafter in this translation of thissection often referred to as the “Agreement”) on September 28, 2010, it did notindicate the date when the project would begin. That is, it indicated the date ofcommencement of the project as June 2010, which is about three months earlierthan the date of agreement (September 28, 2010), as seen in 3. Period andCompletion of Attached Table 4. Main Points of the Agreement Between the GGGIand CW.In addition, the GGGI commenced the outsourcing by paying USD 1,275,000 infront money on October 11, 2010 and USD 1,275,000 on January 10, 2011,though the Agreement had not been signed because Brazil had not placed aformal request for the Project, which was one of the prerequisites for undertakingthe Three Country Project (see 13. Appendix of Attached Table 4), and thus theAgreement had yet to be effectively established and taken effect.52

According to the detailed calculation of the total price of the Agreement, CW(which is a party to the Agreement) was the manager of the Research Service,and the management cost was USD 250,000, while⧋⧋⧋was the actual entitythat conducted the Research, and the total cost of the Research was USD4,000,000. As seen in [Table 9] below, USD 3,180,290 is assigned for consultingthe three countries and USD 819,710 is earmarked for incidentals (business trips,lodging, meals, equipment, communication, and the like).

[Table 9] The Budget for Mckinsey of the Outsourcing(Unit: USD)ClassificationTotalBrazilEthiopiaIndonesiaSubtotal4,000,0001,600,0001,100,0001,300,000Consulting service3,180,2901,340,980814,3101,025,000Incidentals819,710259,020285,690275,000

Source: Recompilation of materials submitted by the GGGI, etc.

However, the GGGI did not receive specific calculation grounds for the costsrequired for CW to manage the Project and for Mckinsey to conduct the Researchincluding the scope of the research and the number of consultants and theirinput time. The GGGI asked CW to submit a financial report and additionalmaterials for external audit, if necessary (see 2. Reports of Attached Table 4),whereas it made it impossible to ask Mckinsey (which is the actual serviceprovider) to submit any evidence for the labor cost for consultants, all sorts ofexpenses, and the like (see 13. ANNEX B of Attached Table 4), thereby making it53

impossible to check, at the time of settlement, whether or not the budget hasproperly been executed.

In regard to the foregoing, CW submitted a financial report on February 15,2011, when it asked for the payment of the balance(hereafter in this translationof this section, the Financial Report).In the Financial Report and the details ofpayment, the total amount of the consulting cost (USD 3,180,290) that CW paidto the representative of Mckinsey is indicated without any mention of how muchhad been paid to whom for labor. Concerning the incidental expenses of USD819,710, a list was attached, but there was no indication of evidence. Thus, thereis no way to know whether or not the funds had really been spent for theperformance of the Research. Moreover, the cost of the management of theProject by CW (USD 250,000) included expenses that are not related to theResearch Service, prompting the GGGI to cut USD 220,756.

As explained above, the GGGI pursued a research outsourcing project whenthe prerequisites for the performance of the research service were not ready andwithout ensuring the responsible execution of expenses, as a result causingopaque execution of a research service budget.

Action to Be Taken:In entering into a research service agreement in order todevise plans for the green growth of developing countries,the chairman of theGlobal Green Growth Institute (GGGI)is advised to ensure that the prerequisites(e.g., formal business requests from the countries concerned) are ready; that areview of whether or not the grounds for the calculation of the price of the54

agreement are appropriate is conducted in order to facilitate the transparentsettlement of expenses; and that the process undergoes appropriate procedures(e.g., signing by the people in authority) for flawless conclusion and managementof research service agreements.[Admonition]

3

Execution of Other Expenses and Coaching and Supervision

[Problem]The inefficient execution of other expenses including expenses for the office aswell as the ineffective internal control system and coaching and supervision werepointed out as problems.

1

Improper Execution of Expenses for the Office and Improper Management

of AgreementsThe GGGI received more than KRW 5,363 million to cover expenses of itsfounding from the reserved fund of the Ministry of Foreign Affairs and Trade forthe fiscal year 2010 and executed more than KRW 5,531 million, mostly for rentand to ready the office (in terms of encumbrances and including the money thatwas not executed in 2010).

① Execution of Expenses (Including Expenses to Ready the Office)

With regard to this matter, the taskforce that prepared for the founding of theGGGI(hereafter in this translation of this section often referred to as the55

“Taskforce”)planned to streamline the organization as much as possible andoperate it with only 30-40 people until the end of 2012; calculated the fundsrequired for the individual budget items (including the rent deposit) accordinglyas seen in [Table 10]; earmarked KRW 5,500 million for the founding andoperation of the GGGI for the fiscal year 2010; and the requested the Ministry ofForeign Affairs and Trade provide that amount.

[Table 10] 2010 Budget for the Founding and Operation of the GGGI—Provision and Execution[Unit: KRW 1,000,1$=1087.00 won]ClassificationRequestedProvided(A)TotalFoundingSubtotalRent deposit for theheadquarters in SeoulInterior of the SeoulheadquartersInterior of the LondonbranchOffice fixturesLegal consulting andotherOperation Rent deposit, laborcost, etc.5,500,000588,170300,0005,363,058536,058300,000Executed(B)5,531,411Difference(B-A)168,353

2,254,830 1,718,772501,868201,868

170,850

162,308

1,373,955 1,211,647

34,17037,59845,5522,411,830

-28,19845,5522,337,000

-299,71479,2931,243,078

-271,51633,741∆1,093,922

56

Business

Development ofinternal capabilitiesand global outreach2,500,0002,490,0002,033,503∆456,497

Source: Recompilation of materials submitted by the GGGI, etc.

On April 30, 2010, the Ministry of Foreign Affairs and Trade submitted to theMinistry of Strategy and Finance a request for the expenditure from the reservedfund in order to budget KRW 5,500 million for the founding and operation of theGGGI, but on May 18, 2010, the Ministry of Strategy and Finance cut therequested amount by KRW 136 million for the reason that excessive expenseswere assigned for interior renovations and office fixtures as seen in [Table 10] andsubmitted a request for KRW 5,363 million to the Cabinet, which approved therequest as it was.

Later, on May 27, 2010, the Ministry of Foreign Affairs and Trade notified theGGGI of the budget above and asked it to execute the budget in compliance withthe plans on its use, details thereof, and the like as much as possible.

Therefore, the GGGI was supposed to execute the funds it received incompliance with their use plans, details thereof, and the like, and if it intended touse such funds for purposes other than those planned and the like, it wassupposed to request the Ministry of Foreign Affairs and Trade’s review andapproval of the reason for the proposed use and the amount thereof.However, the GGGI not only rented a floor area of 829.75 m2on the 19thfloor of Jeongdong Building(hereafter in this translation of this section, the57

“Building”)in Jung-gu, Seoul on May 13, 2010 and paid rent of KRW 238 million(rent period: May 19, 2010 – June 18, 2012), but also rented an additional floorarea of 1,000.93 m2on the 18thfloor of the Building on November 30 of thesame year and paid rent of KRW 263 million (period: the same as that for the19th-floor rent), resulting in total rent of KRW 501 million, which exceeds the KRW300 million earmarked for renting in the budget by KRW 201 million.

In addition, the GGGI executed KRW 1,373 million or so for interiorrenovation, which exceeds the KRW 162 million or so earmarked for interiorrenovation in the 2010 budget (or 8.4 times the budgeted amount); constructedan office space of 199.28 m2on the 19thfloor of the Building with a conditionthat the newly constructed office space would be demolished when the rentagreement expires, spending about KRW 390 million on the construction andvirtually creating the 20thfloor of the Building; conducted a so-called “green-themed” construction, spending about KRW 420 million; and also executed anadditional KRW 469 million or so for the interior renovation of the 18thfloor fromMay to November 2011.

As regards office fixtures, the GGGI executed KRW 299 million or so,exceeding the KRW 28 million or so assigned in the 2010 budget by KRW 271million or so and continued to purchase more fixtures for the 18thfloor in 2011,spending KRW 217 million or so.

As explained above and as seen in [Table 10], the GGGI executed the 2010budget for its founding and operation with variations—an insufficient execution58

of KRW 1,550 million or so (operation: KRW 1,093 million or so; business: KRW456 million or so) and an excessive execution of KRW 1,718 million or so inexpenses for founding, spending a total of KRW 2,254 million for founding (orKRW 2,942 million if the KRW 687 million executed in 2011 is included)—withoutthe Ministry of Foreign Affairs and Trade’s review and approval.

Meanwhile, the GGGI had a plan as of October 2012 to move its Seoulheadquarters to the KDI Hongreung Research Complex in Dongdaemun-gu, Seoulby 2014. Thus, it is likely that KRW 810 million (about KRW 390 million for theoffice expansion construction and about KRW 420 million for the “green-themed”construction) will become a sunk cost and that additional costs will be incurredfor the demolition thereof.

② Office Renovation and Purchase of Tailored Furniture

The GGGI spent KRW 2,226 million or so on four works including officeinterior renovation and purchased custom-made furniture from August 23, 2010to November 2011.

In regard to the foregoing, Paragraphs 1 and 3 of Chapter I and Paragraph 6of Chapter IV of the GGGI Procurement Regulation set forth that the process ofentering into an agreement shall in principle involve open competition to ensureprocedural transparency and openness, but a private contract process is allowedfor a purchase agreement of which the total price does not exceed USD 50,000and for a service outsourcing agreement of which the total price does not exceed59

USD 100,000.

As seen in Paragraph ① earlier, the GGGI received KRW 5,336 million fromthe general reserve account of the Ministry of Foreign Affairs and Trade for itsfounding and operation and the like.

Thus, even though there were no internal rules on entering into agreementson construction works and the like as no procurement rules have yet to bedevised, the GGGI was required to apply the corresponding rules of KOICA withappropriate modifications in dealing with agreement-related tasks such asdetermining the bidding method, calculating costs, and conducting inspections inorder to select the contractors in a fair and transparent manner; eliminate wastefactors; and ensure the efficient execution of its budgets.

However, as seen in [Table 11], when the GGGI proceeded with the fourworks on the office space including an interior renovation and the purchase oftailored furniture, it did not estimate expected prices, but received quotationsfrom a single company before setting the prices and entered into eachagreement orally or in writing without open competition (KRW 2,226 million orso).

60

[Table 11] Agreements for Office Renovation, etc. Concluded Through Non-Competitive Process(Unit: KRW 1,000,1$=1087.00 won)AgreementContractorDate ofPrice ofRemarks

agreement agreementTotalExpansion(construction)SamhupTotalConstructionAug. 16,20102,226,398. Extended the period394,350 twice; increased the costby KRW 164,010,000. Received quotations fromonly one prospectcontractor; non-competitive agreementprocessInteriorrenovation(19thand 20thfloors)Min’sDesignAug. 23,2010553,852. KRW 34,100,000 fordesign and permission forthe expansion work andKRW 49,500,000 for theinterior renovation of the18thfloor are included.. Extended the periodtwice; increased the costby KRW 87,672,000. Received quotations fromInteriorrenovation(18thfloor)DragonflyJan. 21,2011only one prospect472,010 contractor; non-competitive agreementprocess61

. Increased the price KRW98,560,000. Received quotations fromonly one prospectcontractor; non-“Green-themed”constructionGreenConstructionTechnologySept. 20,2010competitive agreement423,500 process. Excessive appropriation(KRW 53,140,000); defectsamounting to KRW58,870,000. Received quotations fromonly one prospectPurchase oftailoredfurniturecontractor; orallyHanssemEffex-382,686requested the contractorto make furniture fivetimes. Expensive furniture (KRW38,260,000)Source: Recompilation of materials submitted by the GGGI, etc.

The GGGI is supposed to pay the balance of an agreement after a pre-delivery inspection, but it paid Green Construction Technology Co., Ltd.(hereafterin this translation of this section, often referred to as the “Green Contractor”)theentire amount of the agreement (KRW 423 million or so) in three installmentsbetween October 21, 2010 and February 14, 2011 without a pre-deliveryinspection, even though it deemed that there were many problems. For example,62

the Green Contractor had proposed installing an electric blind system, whichworks automatically according to changes in the temperature, but the blinds didnot work automatically, and the water flow and the waterproofing of theecological pond also required testing.

In regard to the foregoing, we reviewed how the GGGI had proceeded withthe aforementioned five agreements and found {1} that the GGGI purchasedexpensive, custom-made furniture and interior [sic] for KRW 37 million; and {2}that in the case of the “green-themed” construction, {i} there was an excessiveappropriation of KRW 53 million, {ii} the electric blinds (KRW 67 million or so) donot automatically work according to temperature changes, contrary to what thecontractor proposed, {iii} the roof-top garden and ecological pond created torender a green image (price of construction: KRW 58 million or so) have beendemolished due to defects; and {iv} the hybrid streetlamps and a rainwaterharvesting system are not working as of October 2012.

[Table 12] Waste of Money and Defects in Purchase of Furniture and “Green-Themed” Construction(Unit: KRW 1,000,1$=1087.00 won)AgreementContractorPrice ofagreementPurchaseof tailor-madeHanssemEffex. Purchase the furniture at a high price of over382,686 KRW 37 million. We received quotations from Lavat Furniture63

Details of waste of money and defects

furniture

and more for the price of furniture of the sametypes and dimensions on January 14, 2011 andfound Hanssem Effex price (KRW 165 million)was higher than Livart Furniture’s price (KRW149 million) by about 9.8 %, indicating that thetotal price would have been lower by KRW 37million[=0.098 x KRW 382,686,000 (price paidto Hanssem Effex )] if the furniture had beenpurchased from Livart Furniture .An excess of about KRW 53 million was paid. In the first sheet of quotations, the consultingfee was KRW 17 million or so.. Considering KRW 24 million was earmarkedas the fee for reviewing technology /structurereinforcement and production of detaileddrawings (detailed working drawing anddetailed cross-sectional drawing), whichconstitute consulting on detailed construction423,500including the installation of a double-skinsystem, the consulting fee of KRW 53 millionor so, which is separately assigned, shouldhave not been included in the total price ofthe agreement.Defects. The electric blinds does not automaticallywork according to temperature changes. As regards the construction to render a greenimage (price: KRW 58 million or so), theecological pond and the roof-top garden were64

“Green-themed”construction

GreenConstructionTechnology

demolished, and the hybrid streetlamps andthe rainwater harvesting system do not work.. While the installation of the double-skinsystem (price: KRW 117 million or so) helpsreduce theheating cost, but resulted in ahigher cooling cost including the installation ofair conditionersSource: Recompilation of materials submitted by the GGGI, etc.