Udvalget for Fødevarer, Landbrug og Fiskeri 2011-12

FLF Alm.del Bilag 10

Offentligt

COUNCIL OFTHE EUROPEAN UNION

Brussels, 12 September 2011 (13.09)(OR. fr)

6751/11EXT 1

PECHE 52

PARTIAL DECLASSIFICATIONof document:6751/11 RESTREINT UEdated:18 February 2011new classification: publicSubject :Specific Agreement No 26: Ex-post evaluation of the current Protocol to theFisheries Partnership Agreement between the European Union and theKingdom of Morocco, Impact study for a possible future Protocol to theAgreement

Delegations will find attached the above document, partially declassified (first part1).

_______________________

1

See also EXT 1 ADD 1-5.

6751/11 EXT 1DG B III

kea/JL/ms

1

EN

@

MEGAPESCA Lda

FRAMEWORK CONTRACT FISH/2006/20SPECIFICAGREEMENTNO26: EX-POST EVALUATION OFTHE CURRENTPROTOCOL TO THEFISHERIESPARTNERSHIPAGREEMENT BETWEEN THEEUROPEANUNION AND THEKINGDOM OFMOROCCO,IMPACT STUDY FOR A POSSIBLE FUTUREPROTOCOL TOTHEAGREEMENTReportDecember 2010

6751/11 EXT 1ANNEX

kea/JL/msDG B III

2

EN

This report has been prepared with the financial support of the European Commission.The views expressed in this study are those of the authors and do not necessarily reflect the views of theEuropean Commission or of its services. This report does not seek to establish the Commission’s futurepolicy in this area.The content of this report may not be reproduced, or even part thereof, without explicit reference to thesource.

Oceanic Développement, MegaPesca Lda (2009). ‘Framework contract for carrying out evaluations,impact studies and monitoring concerning the Fisheries Partnership Agreements (FPA) concludedbetween the European Community and third countries, and more generally on the external aspect of theCommon Fisheries Policy: Ex-post evaluation of the current Protocol to the Fisheries PartnershipAgreement between the European Union and the Kingdom of Morocco, Impact study for a possible futureProtocol to the Agreement.

INTERNAL DOCUMENT : NOT FOR PUBLICATIONAuthor’s contact:OCEANIC DEVELOPPEMENTZ.I. du Moros, 29900 Concarneau, FranceTel :+33 2 98 50 89 99Fax :+33 2 98 50 78 98Email :[email protected]URL :http://www.oceanic-dev.comVersion : ReportRef. report: FPA 26/MAR/10Publication Date: 14/12/2010

Annual exchange rates used20041 EUR = MADSource: FXTOP.com11.02200511.02200611.04200711.21200811.33200911.24201011.14

6751/11 EXT 1ANNEX

kea/JL/msDG B III

3

EN

List of abbreviationsACPCACECAFCITESAfrican, Caribbean and Pacific StatesTurnoverFishery Committee for the Eastern CentralAtlanticConvention on International Trade inEndangered Species of Wild Fauna andFloraMinisterial Conference on FisheriesCooperation among African Statesbordering the AtlanticData Collection FrameworkData Collection RegulationDirect foreign investmentDépartement de Pêche Maritime (SeaFisheries Department)Exclusive Economic ZoneEuropean Fisheries FundEtablissement de Formation Maritime(Maritime Training Institute)European Free Trade AssociationFood and Agriculture OrganisationFisheries Monitoring CentreFull-time equivalentFood and Veterinary OfficeGross Domestic ProductGross registered tonnageInternational Convention for theConservation of Atlantic TunaICESICTIEOINRHInternational Council forthe Exploration of theSeaInformation andCommunicationTechnologiesInstituto Español deOceanografíaInstitut National deRecherche Halieutique(National Institute forFisheries Research)International Union forConservation of NatureIllegal, Unreported andUnregulatedMillion euroMoroccan DirhamMillion ECUNorthwest AtlanticFisheries OrganisationNon-governmentalorganisationNational IndicativeProgrammeOffice National desPêches (NationalFisheries Office)Fish landing siteRefrigerated Sea WaterSanitary orPhytosanitaryTotal allowable catchesValue addedVillage de Pêche(fishing village)Vessel MonitoringSystem

COMHAFATDCFDCRDFIDPMEEZEFFEFMEFTAFAOFMCFTEFVOGDPGRTICCAT

IUCNIUUM€MADMECUNAFONGONIPONPPDARSWSPSTACVAVDPVMS

6751/11 EXT 1ANNEX

kea/JL/msDG B III

4

EN

CONTENTSINTRODUCTION .................................................................................................................1PART 1: GENERAL FRAMEWORK ....................................................................................21GENERAL PRESENTATION ......................................................................................21.1 Physical geography ...............................................................................................21.2 Population ............................................................................................................. 32MACROECONOMIC SITUATION ...............................................................................42.1 Gross domestic product.........................................................................................52.2 Foreign trade .........................................................................................................62.3 Budgetary aspects.................................................................................................82.4 Foreign investment and the business climate........................................................92.5 Employment......................................................................................................... 113REGIONAL DATA .....................................................................................................124RELATIONS WITH THE EUROPEAN UNION ..........................................................144.1 Political aspects................................................................................................... 144.2 Financial aspects................................................................................................. 154.3 Relations with other donors .................................................................................15PART 2: ANALYSIS OF THE FISHERIES SECTOR .........................................................171OCEANOGRAPHIC CHARACTERISTICS OF THE MOROCCAN EEZ ................... 171.1 Exclusive Economic Zone ................................................................................... 171.2 Hydrological conditions of the Moroccan Atlantic coastline ................................. 172THE MOROCCAN FISHERIES SECTOR ................................................................. 202.1 National fishing fleet ............................................................................................202.2 Foreign fishing fleet ............................................................................................. 252.3 Summary: fishing fleets in the Moroccan EEZ ..................................................... 312.4 Aquaculture ......................................................................................................... 322.5 Land-based industries .........................................................................................332.6 Utilisation of catches............................................................................................352.7 Employment......................................................................................................... 413SUPERVISION OF THE SECTOR AND CHECKS FOR COMPLIANCE WITHTHE REGULATIONS ................................................................................................ 433.1 Principal fisheries supervisory measures ............................................................ 433.2 The national surveillance and control system ...................................................... 454THE INSTITUTIONAL FRAMEWORK....................................................................... 474.1 The main institutions responsible ........................................................................ 474.2 Sectoral policy .....................................................................................................514.3 International integration ....................................................................................... 58

- Page i -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

5

EN

STATE OF FISHERIES resources ................................................................... 595.1 Small pelagic species ................................................................................. 595.2 Demersal resources ................................................................................... 685.3 Large pelagic species................................................................................. 745.4 Impact of fishing on the environment.......................................................... 75PART 3: ASSESSMENT OF THE FISHERIES PARTNERSHIP AGREEMENT....... 841THE FISHERIES PARTNERSHIP AGREEMENT ............................................ 841.1 Presentation of the agreement and its protocol .......................................... 841.2 The fishing opportunities negotiated........................................................... 861.3 Utilisation of negotiated fishing opportunities ............................................. 871.4 The cost of the agreement.......................................................................... 911.5 Provisions dealing with seamen and compulsory landings......................... 961.6 Provisions on monitoring of vessels ........................................................... 992SOCIOECONOMIC ANALYSIS OF THE IMPACT OF THE AGREEMENT ... 1002.1 Economic analysis.................................................................................... 1002.2 Employment.............................................................................................. 1053THE PARTNERSHIP APPROACH................................................................. 1063.1 Partnership in the field of sectoral policy .................................................. 1063.2 Partnership in the scientific field ............................................................... 1073.3 Partnership in the field of economic integration ........................................ 1083.4 Partnership in the field of inspection and surveillance .............................. 1094EX-POST EVALUATION OF THE PROTOCOL TO THE AGREEMENT ....... 1194.1 The effectiveness of the fisheries agreement ........................................... 1104.2 The efficiency of the fisheries agreement ................................................. 1124.3 The relevance of the fisheries agreement ................................................ 1144.4 The viability of the fisheries agreement .................................................... 1154.5 Main conclusions of the ex-post evaluation .............................................. 116CONCLUSION........................................................................................................ 118

5

- Page ii -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

6

EN

INTRODUCTIONFisheries relations between the Kingdom of Morocco and the EU are longstanding. Before Spain’saccession, there were already agreements which allowed Spanish vessels access to Moroccanfishing zones. Under the exclusive competence of the Union in this field, it was logical for theCommunity institutions to take over these agreements, with a first Agreement concluded in 1988.This Agreement was renewed several times without interruption until 1999, when the two partieswere forced to concede that the negotiations had failed.The two parties decided to resume dialogue on the subject and, in July 2005, the EU and Moroccosigned a Fisheries Partnership Agreement which would enter into force only in February 2007 afterthe ratification procedures. The Protocol to the Agreement expires in February 2011. Prior to therenegotiation of the Agreement, and following the Council guidelines and the provisions of the EUFinancial Regulation, the present Protocol must be the subject of ex-post evaluation and an impactstudy to ascertain whether the results of the programme correspond to the objectives set (ex-postevaluation) and to provide the legislator with the means to judge whether a new programme (thefuture protocol) is necessary and consistent with the Union policies in this sector, by providing itwith the tools to assess the impact of the policy. To this end, DG MARE assigned the evaluation ofthis Protocol to the consortium of undertakings holding the FISH/2006/20 framework contract.The Fisheries Partnership Agreement concluded between the EU and Morocco is of particularimportance in many respects. Firstly, its financial importance and the European fishing capacitieswhich can fish in the Moroccan fishing zone. With provision for more than 100 EU vessels and witha financial contribution of EUR 36.1 million per year for four years, the Agreement with Morocco isthe second most significant Community agreement with the countries of the South, far behind theagreement with Mauritania (EUR 85 million per year maximum) but exceeding the agreement withGuinea Bissau (EUR 7.5 million per year maximum), which is the third largest agreement infinancial terms. The agreement with Morocco represents 25% of the budgetary commitments ofDG MARE for bilateral fisheries agreements. Secondly, the agreement is important as it involvestwo partners with neighbouring, and in part common, frontiers which have chosen to strengthentheir political links and to move towards progressive economic integration. The AssociationAgreement which entered into force in 2000 and the advanced status accorded to Morocco in 2008constitute tangible evidence of this will to deepen relations.This draft final evaluation report provides a general portrait of the Moroccan economy. It seeks todefine the significance of the fisheries sector in the country’s macroeconomic equilibrium. In part 2,the fisheries sector in Morocco is reviewed in order to present its main characteristics and toidentify the absolute and relative contribution of the European part in its recent development.Finally, part 3 of this report uses the results of the first two parts to draw the main lessons ofrelevance for the ex-post evaluation of the Protocol and the impact study of several scenarios forrenewal of the Protocol to the Agreement in progress so that a future protocol respects theinternational commitments of the two parties and minimises any unfavourable impact on the partiesto the Agreement.The key information for this evaluation study was collected by examining the relevant literature andsupplementing this by talks with the Commission services, the Moroccan authorities, and thestakeholders of European and Moroccan civil society (primarily professional organisation). Anassessment mission to Morocco was organised in September 2010, during which the experts wereable to meet the Moroccan authorities and the EU delegation at Rabat, the research institute andnational fisheries office in Casablanca, and various parties involved in the sector in Dakhla. Thesemeetings in Morocco were held in an excellent spirit of cooperation and in full transparency. Themission thanks the Moroccan authorities for their availability and the assistance given for theorganisation of the meetings in Morocco.- Page 1 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

7

EN

PART 1: GENERAL FRAMEWORK11.1GENERALPRESENTATION

Physical geography

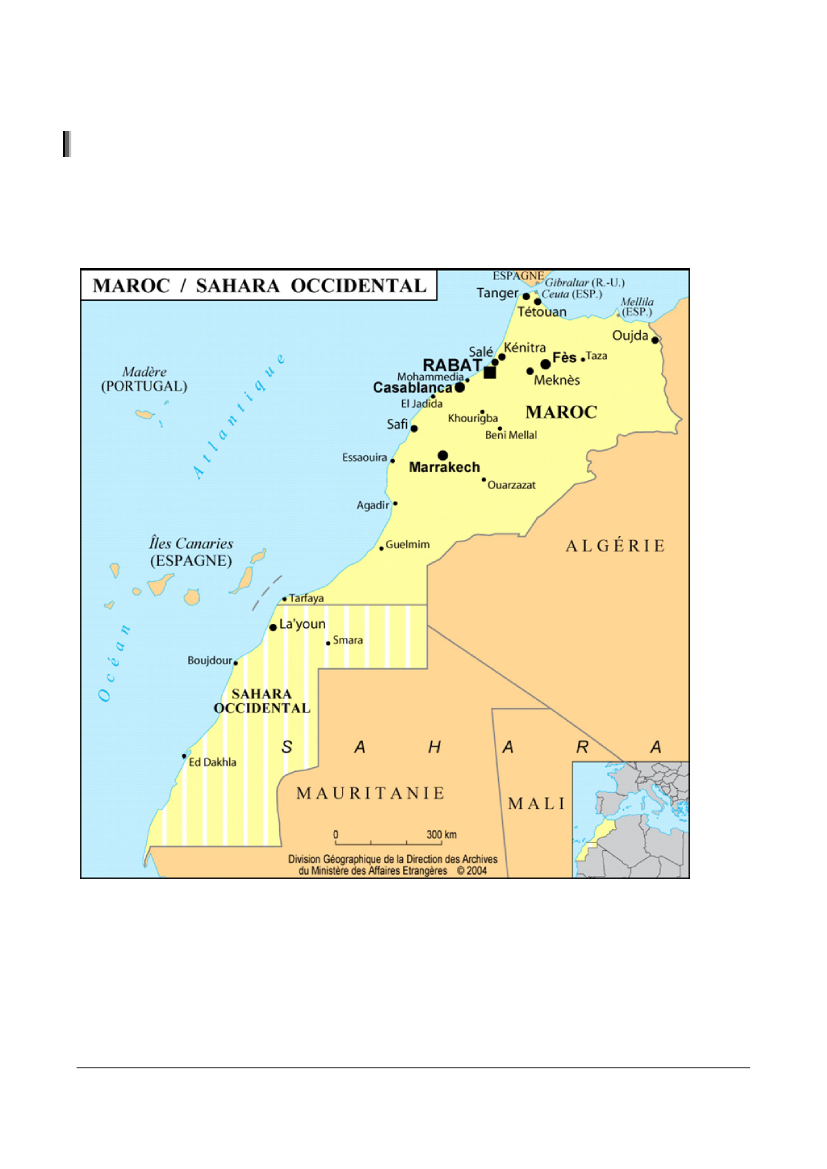

Morocco, officially the Kingdom of Morocco, is a country located in North-West Africa andbelonging to the Maghreb. Its political capital is Rabat, whereas its economic capital and largestcity is Casablanca. The country is bordered by the Atlantic Ocean to the west, Spain, the Straightof Gibraltar and the Mediterranean Sea to the north, Algeria to the east andde factoby Mauritaniato the south, beyond the Western Sahara which is in dispute. The country covers an area of some710 000 km�, of which 252 000 km� in the Western Sahara.

Figure 1: General map of Morocco and the Western Sahara. Source: Ministry of Foreign Affairs, France

The Moroccan climate is both Mediterranean and Atlantic, with a dry, hot season coupled with acold wet season, the end of the hot period being characterised by the October rains. The presenceof the sea mitigates the temperature differences, moderates the seasons and increases the airhumidity (400 to 1000 mm of rain at the coast). Inland, the climate varies according to the altitude.The summers are hot and dry, especially when the sirocco or the chergui, a summer Saharan- Page 2 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

8

EN

wind, is blowing. During this season, the temperatures average 22�C to 24�C. The winters are coldand rainy with frost and snow. The average temperature then fluctuates between -2�C and 14�Cand may fall as low as -26�C. The mountainous regions have very heavy rainfall (over 2000 mm ofrain in Rif or 1800 mm in the Middle Atlas). Pre-Saharan and Saharan Morocco has a dry desertclimate.1.2Population

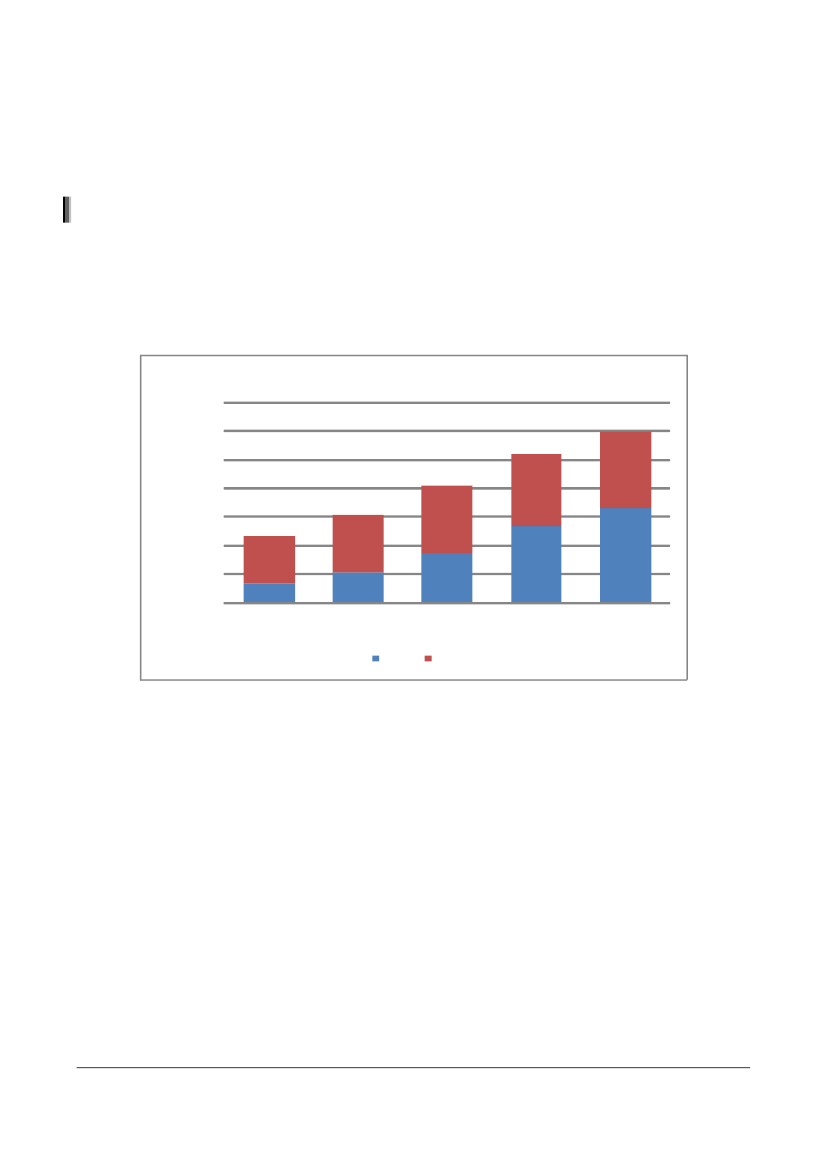

According to estimates, Morocco’s resident population in mid-2010 is approximately 31.8 million.The country experienced strong demographic growth throughout the 20th century, with itspopulation multiplying six-fold. During the same period, the proportion of the population in urbanareas increased constantly, attaining 55% in 2004: the country now has some thirty cities withmore than 100 000 inhabitants, whereas there were none a century ago; and three agglomerations(Casablanca, Rabat-Salé and Fès) have more than one million inhabitants.Population35 000 00030 000 00025 000 00020 000 00015 000 00010 000 0005 000 000019601971Urban1982Rural19942004

Figure 2: Trend in the Moroccan population according to censuses. Source: High Commission for Planning

The population of the Kingdom comprises almost as many men as women. The percentage ofwomen is 50.7%. The proportion is the same in both town and countryside. By age group, 31.2% ofinhabitants are under 15 years of age, 60.7% between 15 and 59 and 8.1% are 60 years of ageand over. Compared to the 1994 census, the proportions of the population of working age andthose of retirement age have increased to the detriment of the young, indicating a relative ageingof the population of the country. This phenomenon should be compared to the sharp fall in the totalfertility rate from 7.2 in 1962, to 3.3 in 1994, then to 2.5 in 2004.In 2008, the Moroccan diaspora was estimated at 5.2 million people spread over the fivecontinents. Just under 85% of Moroccan residents abroad were at that time resident in Europe.France, in first place, accommodated 34% of the Moroccan expatriate community, i.e. 1.9 millionpeople, of whom 31% in the vicinity of Paris. Then comes Spain with 917 132 residents, followedby Italy with 710 105, the Netherlands and Belgium, both with about 500 000. Germany and theUnited States total 140 000 and 250 000 residents respectively.- Page 3 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

9

EN

2.

MACROECONOMIC SITUATION

Morocco now belongs to the category of emerging countries, in the same capacity as India orTurkey. Morocco is classified by the United Nations in the lower middle income category ofcountries.Morocco has a liberal market economy governed by the law of supply and demand, although forthe time being some economic sectors are still State monopolies (although none in the fisheriessector).The country’s economic system is multi-faceted. It is characterised by considerable openness tothe outside world, as shown by the various free trade agreements which Morocco has ratified withits main economic partners:the free trade agreement with the European Union in the context of the EuroMed partnership,also associating other countries of the continent bordering on the Mediterranean;1the free trade agreement with the EFTA countries;the Agadir Agreement, signed with Egypt, Jordan, Tunisia, in the context of theestablishment of the Arab Free Trade Area;the free trade agreement with the United Arab Emirates;the free trade agreement with Turkey;and recently the free trade agreement with the United States, which entered into force in2006.Morocco is the world’s leading producer and exporter of phosphates. This product represents asignificant inflow of foreign currency for the country. Concentrated in the north, 60% of farmland inthis region is devoted to this activity, which is highly lucrative given the trend in world prices.Morocco also exports significant quantities of handicraft products each year.Cereals (wheat and barley) are cultivated on 50% of the arable land. These economically importantcrops are cultivated on the basis of two systems: one very modern and the other still archaic.Since independence, the authorities decided to exploit the immediate possibilities offered by thecountry. The government policies had several objectives:Turning the rural and agricultural aspect of the country to effect in order to develop modern,efficient agriculture, despite the difficult climatic conditions plaguing the country, with a viewto fuelling exports, the country’s domestic markets and the agri-foodstuffs industry. It shouldalso be noted that the fisheries sector was already making a large contribution to exports.The authorities have opted for large-scale exploitation of the deposits of phosphates, ofwhich the country possesses about one third of the known world reserves, in this way leadingto the establishment of a major chemicals plant for the processing and development ofphosphates.The industrial processing sector has not lagged behind since the country is still seeking toattract a growing number of foreign investors. The government aims to strengthen severalsectors, such as textiles, light processing industries, mechanical engineering industry, motorindustry, pharmaceuticals, electronics, new technologies and recently the aeronautics sectorthanks to the national enterprises and especially too the many European relocations toMorocco in this field.1

Therefore Morocco, plus Algeria, Palestinian Authority, Egypt, Israel, Jordan, Lebanon, Syria,Tunisia and Turkey.- Page 4 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

10

EN

In Morocco, the development of tourism has received considerable government attention. Forthat matter, the government has always given strong encouragement to private Moroccaninvestors and large international groups to make massive investments in this sector.Development in the tertiary sector has accelerated strongly over the past decade and more,in particular in the sectors of banking, finance, retailing and distribution, mobile telephonyand offshoring (relocation of call centres and services, as well as European computer servicecompanies, etc.).

2.1

Gross domestic product

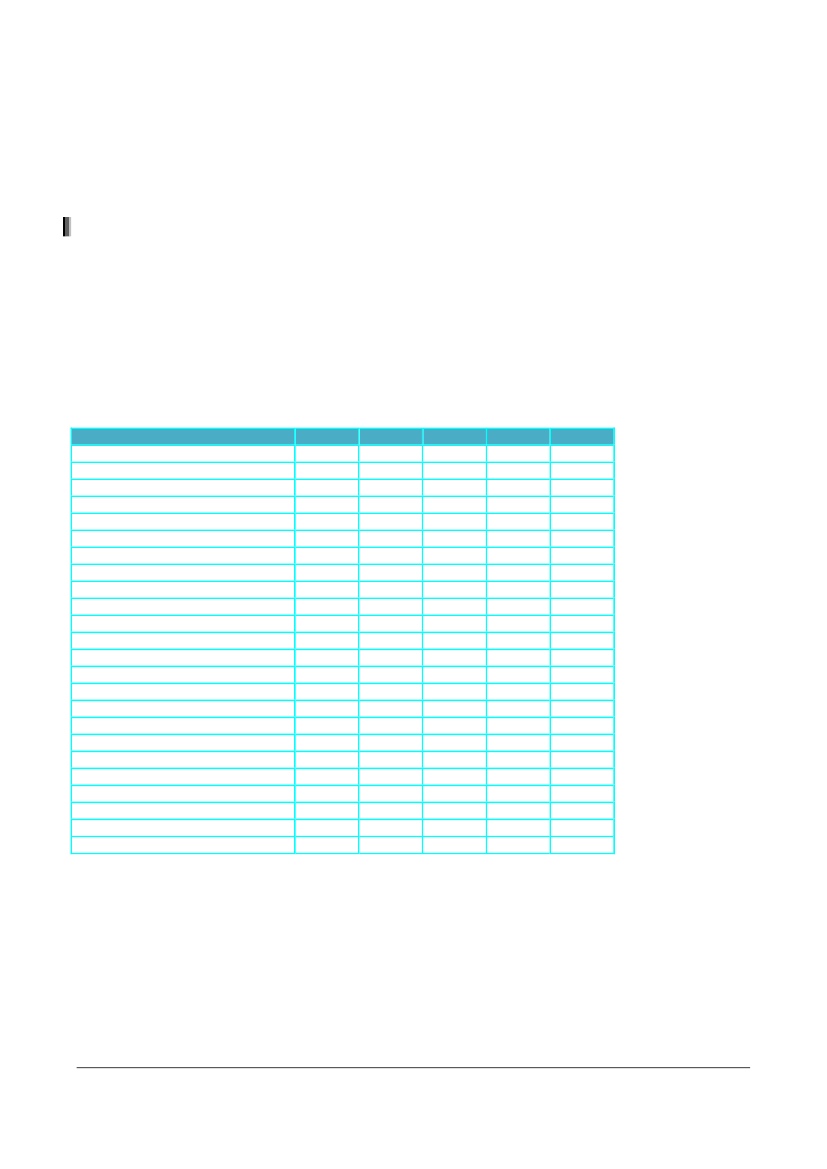

According to the data of the National Accounts Department of the High Commission for Planning,Morocco’s GDP at current prices amounted in 2008 to just over EUR 60 billion and has been risingsteadily since 2004. Accounting for 55%, the tertiary sector remains the main contributor to GDP. Itoutstrips the secondary sector (30% contribution) driven in particular by the mining sector, and theprimary sector, the contribution of which amounts to approximately 15%. Overall, GDP at currentprices has risen by 11.8%, compared to 6.7% in 2007. The added value from agriculture rose by20.7%, whereas that from non-agricultural activities increased by 12.4%.Table 1: Details of Morocco’s gross domestic product. Data shown in EUR million.* Source: High Commission forPlanningEconomic sectorPrimary sector (M€)AgricultureFisheriesSecondary sector (M€)Extractive industryIndustry (other than petroleum)PetroleumElectricity and waterConstructionTertiary sector (M€)CommerceHotels & restaurantsTransportPost and telecommunicationsOther servicesPublic administrationTotal basic prices (M€)Tax on income net of subsidies20046 7276 26446311 7587367 134881 1842 61522 7384 9231 0011 6881 3979 7174 01241 22341 2234 60420056 3135 71160212 1378167 0021351 3232 86024 5595 1231 1761 6301 50310 7794 34843 00943 0094 87520067 9247 35057412 7389547 3551171 3302 98126 2535 5211 2021 6631 64311 6364 58946 91646 9165 38020076 6846 13055413 2961 1747 321751 4053 32128 6995 8041 4542 0751 77412 9624 63148 67948 7036 2942008**8 0287 32368116 5813 9827 678851 4233 41230 1046 2311 4372 1091 88613 6754 76654 71354 6896 109

GDP (M€)45 82747 88452 29654 97460 798* The original data are in million MAD. They were converted into EUR on the basis of the mean parity presented in the introduction for the purposesof this study.** Forecasts

Economic growth amounted to 5.6% in 2008, compared to 2.7% one year previously, as a result ofthe 16.6% increase in added value of the primary sector and, to a lesser extent, the progress in thenon-agricultural activities, although this has slowed from 6% to 4.1%. In fact the deterioration in theeconomic situation in the euro area, Morocco’s main trading partner, especially from the fourthquarter, has affected certain industrial sectors, the production of which mainly targets theEuropean market, as well as tourism and transport.- Page 5 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

11

EN

At primary sector level, agricultural activities increased by 16.3%, as opposed to a fall of 20.8%one year previously. Cereals production more than doubled from one year to the next on accountof more favourable weather conditions, whilst fisheries activities recorded an increase of 19% aftera fall of 10.1% one year previously. On the other hand, the growth rate in the secondary sector fellfrom 6.6% to 3.6%, mainly as a result of the 5.9% contraction in the activity of the extractiveindustries and the slowdown in the activities of the manufacturing industries following the decline inforeign demand linked to the world crisis. The agri-foodstuffs industries (including the processing offisheries products) make a significant sectoral contribution, estimated to represent 35% ofindustrial GDP. The tertiary activities, including the non-market services supplied by the publicadministration, rose by 4.1% after 6.1% growth in 2007, despite the near stagnation intourism-related services. For their part, commercial activities and telecommunications haverecorded appreciable progress year-on-year.For 2009, the IMF forecasts real growth of 5%, sustained in particular by a crop year deemed to beexceptional. The financial sector in Morocco is unlikely to be greatly affected by the world financialcrisis in view of its low exposure to toxic assets. However, the world crisis does affect the realsector. Morocco felt the effects of the crisis largely through the economic slowdown in Europe, itsmain trading partner. Although most of the recent data show a recovery in revenue, for the first halfof 2009 compared to that of 2008, exports fell by 34%, tourism revenue declined by 14% andremittances by 12%. DFI was also down by 34%. Affected by the employment crisis in Europe,transfers by Moroccan nationals established abroad also fell significantly. These transfersrepresent about 10% of GDP.For all that, according to the IMF, economic activity in 2009 resisted partly thanks to the soundnessof the initial conditions, attributable to the reforms in recent years. The reforms of the past tenyears have stimulated non-agricultural growth and made the economy more resilient to shocks,thereby enabling Morocco to limit the impact of the crisis. In particular, the macroeconomic gains –low inflation, low budget deficits and public debt ratios falling – as well as the structural reformsdesigned to increase economic flexibility, have increased Morocco’s room for manoeuvre in itsresponse.→Thefisheries sector and GDPThe contribution of the fisheries sector to Morocco’s GDP is estimated at approximately 1% of totalGDP and at 7% to 8% of primary sector GDP. However, this contribution takes no account of theactivities relating to the catching and first sale of the produce and takes no account of the addedvalue generated by the related upstream sectors (shipbuilding and repairs, supplies of goods andservices for fitting out vessels) and especially the downstream sectors (processing and marketingof fisheries products). The contribution from the related sectors to GDP is posted to the accountsunder other sectors, notably those of industries and services.According to the assessments of the Minister responsible for fisheries, the total contribution of thefisheries sector to GDP, all sectors together, is in the order of 2% of national GDP. Thiscontribution remains low, which would indicate that the fisheries sector in Morocco is not yet adriver of growth.2.2Foreign trade

The Moroccan trade balance records a deficit which has tended to increase over the past fiveyears (from EUR -7.7 billion in 2005 à EUR -13.6 billion in 2009). For this last year, the tradebalance shows a 10% improvement, but this masks a slowdown in exports of 29% compared to2008, which is a consequence of the fall in international demand resulting from the financial crisis.The concurrent decline in imports in 2009 (-18.7%) is attributable to the significant fall in petroleumproduct prices.- Page 6 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

12

EN

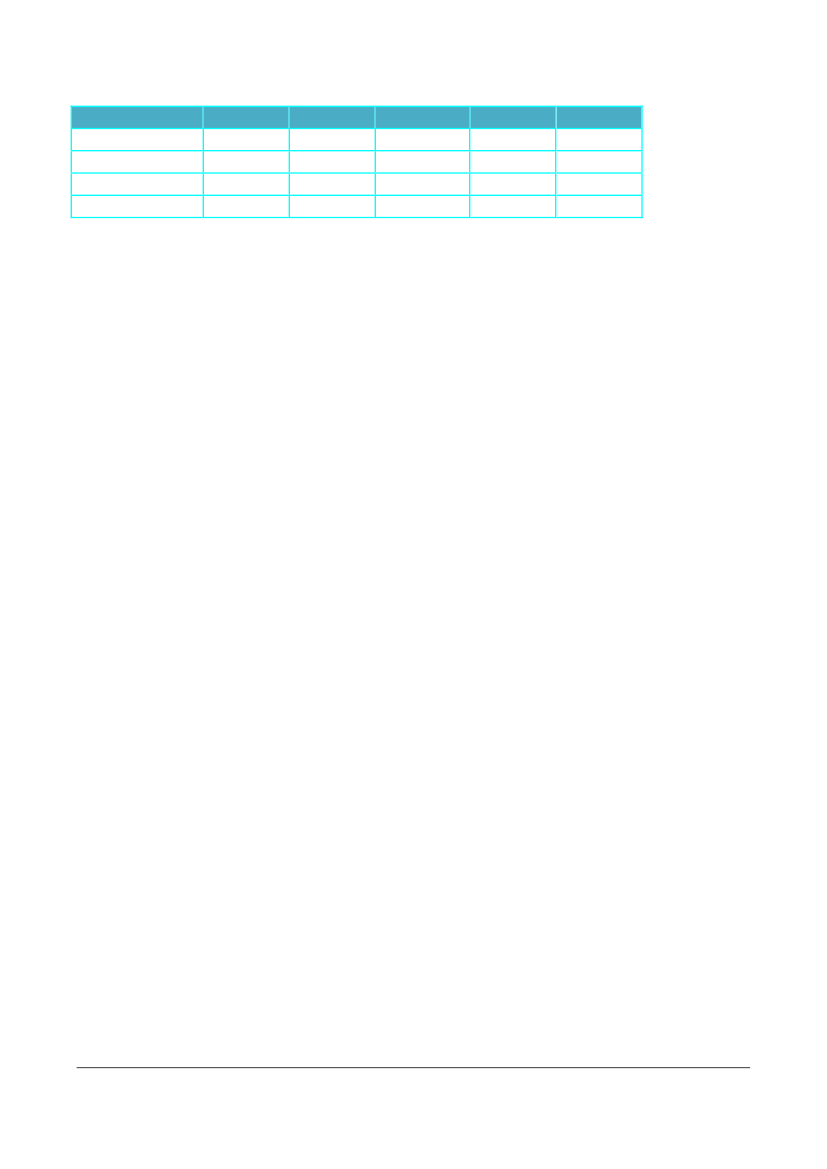

Table 2: Moroccan trade balance Source: Foreign Exchange Office(million EUR)

Imports

Exports

Balance

Cover rate

* Provisional data

2005

16 7319 008-7 72453.8%2006

19 07210 143-8 92953.2%2007

23 30811 197-12 11248.0%2008

28 77713 746-15 03147.8%2009*

23 5939 961-13 63242.2%Moroccan imports are dominated by hydrocarbons (petroleum products, gas) and capital goods(machines, vehicles, domestic equipment), which together account for 55% (2008) to 60% (2009)of total imports. Owing to the fall in world prices in 2009 compared to 2008, the value of imports ofhydrocarbons fell by almost 50% in 2009 compared to 2008. Thanks to a favourable crop year,Morocco was also able to halve its cereals imports in 2009.Morocco’s main exported goods are phosphates and derived products, ready-made clothing andfisheries products. On account of the fall in world prices, the contribution of phosphates, which in2008 accounted for 33% of total exports and a value of nearly EUR 4.5 billion, in 2009 amounted toonly 17% and a value of EUR 1.7 billion (-63%). The exports of ready-made goods also fellbetween 2008 and 2009 (-6%) with a contribution to total exports rising by 12% to nearly 16%.Exports of fisheries products (raw or processed) in 2008 represented a value of nearly EUR 1.2billion (8.5% of total exports in 2008) but fell to EUR 1.1 billion in 2009. This sector’s contribution tototal exports shows a significant increase in 2009 (11.1% of Moroccan exports). For 2009, like theprevious year, exports of fisheries products are well above the exports of other agricultural sectors(citrus fruit, tomatoes or fresh and processed vegetables).As regards Morocco’s trading partners, the European Union remains the main partner, well aheadof the countries of Asia, America or Africa. In 2009, 60% of imports into the country originated inthe EU and 70% of Moroccan exports were destined for the EU market. The second mostimportant partner region is Asia, with 22% of imports and 14% of exports. By country, France andSpain are Morocco’s main trading partners, with shares of 18.3% and 14.8% respectively of totaltrade. The balance of trade between the EU and Morocco is heavily in favour of the EU (deficit ofEUR 8.8 billion in 2008 and EUR 7.1 billion in 2009).- Page 7 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

13

EN

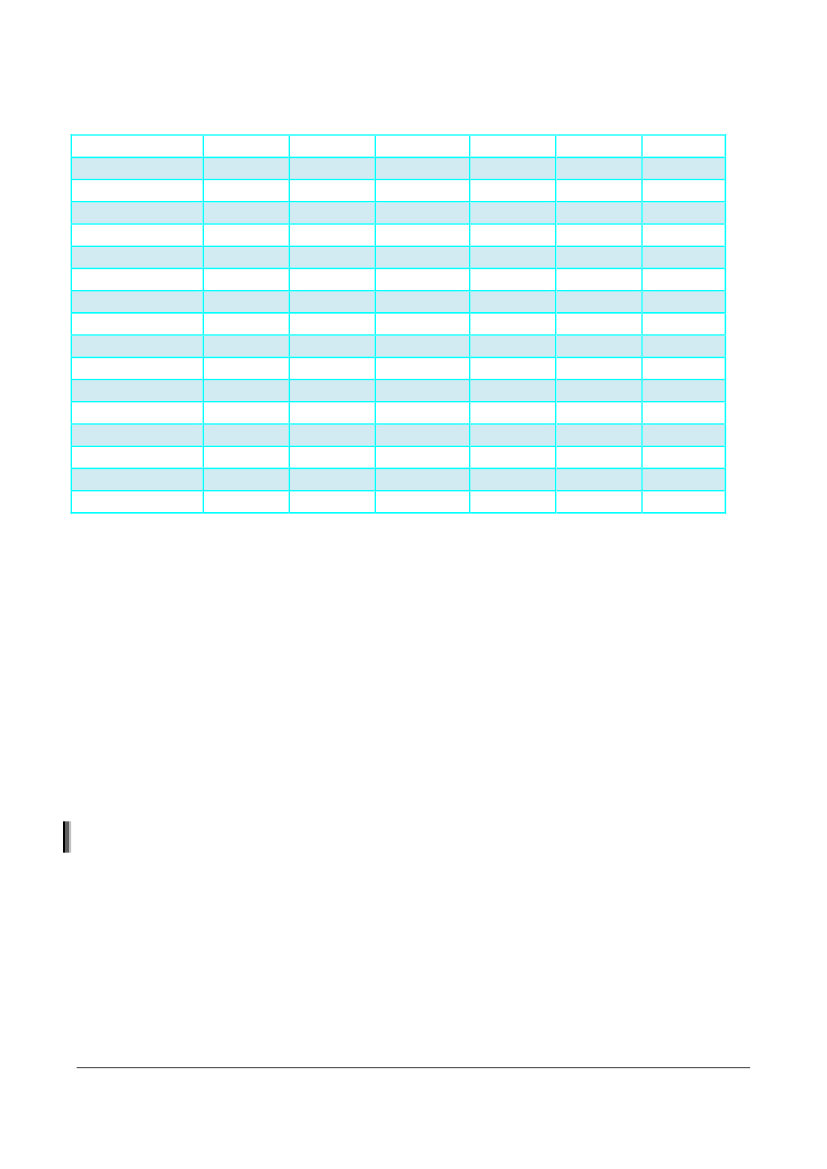

Table 3: Geographical structure of trade. Source: Foreign Exchange Office(million EUR)EUROPEEUOtherImportImportImport200510 8048 8341 970200611 7229 8371 884200714 62212 3772 253200817 81615 0622 7542009*14 06912 2791 790

EUROPEEUOther

ExportExportExport

6 9786 638340

7 8207 375445

8 4628 022440

8 9338 225709

6 9596 484475

ASIAASIA

ImportExport

3 513892

4 277978

4 8221 083

6 6262 265

5 0761 372

AMERICAAMERICA

ImportExport

1 435601

1 706619

2 556889

3 0151 462

2 991675

AFRICAAFRICA* Provisional data

ImportExport

933460

1 038571

1 483565

1 551705

1 194719

→Thefisheries sector and foreign tradeRaw or processed fish, crustaceans and molluscs make a significant contribution to exportearnings, accounting for 11% of the total and a value of EUR 1.1 billion (2009 provisional data).Exports of fisheries products provide a positive net contribution to the trade balance in so far asimports are very limited apart from products admitted under temporary procedures for inwardprocessing and which are therefore subsequently re-exported. The fishing industry therefore playsa significant role in the country’s export earnings. As will be shown below, the EU market, andespecially those of Spain, France and Italy, is the main outlet for the fisheries product exports,accounting for nearly 70% of turnover. The second major market is that of the other Africancountries, which generates 13% of export earnings. It is a particularly dynamic sector, with aturnover which has practically doubled between 2004 and 2008.

2.3

Budgetary aspects

The table below shows the main budgetary aspects published in the successive Finance Actspassed since 2007. The budget deficit forecasts aim to confine the deficit to about 2% of GDPeach year. The 2010 budget takes account of the indirect effects of the world financial crisis onMorocco, with falling revenue accompanied by expenditure estimates which are also lower.Morocco plans to control the expenditure of the Administration with a smaller operating budgetthan in 2009, but by continuing to increase investment, with a forward budget exceeding EUR 7billion, whereas it was below EUR 5 billion in 2008.- Page 8 -

6751/11 EXT 1ANNEX

kea/JL/msDG B III

14

EN