Udvalget for Fødevarer, Landbrug og Fiskeri 2010-11 (1. samling)

FLF Alm.del Bilag 71

Offentligt

EUROPEAN PARLIAMENT

2009 - 2014

Special committee on the policy challenges and budgetary resources for asustainable European Union after 2013

21.9.2010

REFLECTION PAPERon the concept of European Added ValueRapporteur:Salvador GARRIGA POLLEDO

1. IntroductionAgainst the background of scarce resources and austerity programmes in literarily allMember States, European expenditure has to be justified even more thoroughly thanin the past.It seems worth reminding that EU expenditure, by creating European added value, issupposed to contribute to achieving agreed policy targets more effectively, whichcould also reduce the need for parallel national expenditure .The purpose of this reflection paper is to examine the concept of European addedvalue with regard to its current use, its operability in European decision makingprocesses and its political semantics in a moment when Europe moves from theLisbon Agenda to EU2020.

European Added Value or European Value Added:These enigmatic words are often used, unfortunately also in aninflationary way. Their multi-purpose use bears the risk that the phraseis turns into "fashionable buzz-words"1that quickly lose their meaning.

2. European added value, the little sister of the principle of subsidiarityIn his working document from 6 May 2010, the Chairman of the Committee onBudgets explores the idea of a "European dividend", which is created by "applying theprinciple of subsidiarity in financial matters." The European dimension can"maximise the efficiency of [Member States'] finances" and help to "reduce totalexpenditure. This is exactly what large industrial groups do: they pool commonservices to benefit from the economies of scale."2In fact, the European Added Value can be considered the "corollary of the establishedprinciple of subsidiarity"3as defined in Article 5 TEU:3. Under the principle of subsidiarity, in areas which do not fall within its exclusive competence, theUnion shall act only if and in so far as the objectives of the proposed action cannot be sufficientlyachieved by the Member States, either at central level or at regional and local level, but can rather, byreason of the scale or effects of the proposed action, be better achieved at Union level.

As a consequence, the EU budget should be used to finance actions that MemberStates and regions cannot finance themselves with better results.In other words, expenditure at EU level should be able to make proof of its Europeanadded value, following the "subsidiarity check".

12

D. Tarschys: The Enigma of European Added Value (SIEPS 2005)A. Lamassoure:Working document DT\815212on financing the 2020 Agenda despite the budgetarycrisis3D. Tarschys: op. cit.

2

However, it is worth recalling the conclusions or the European Convention’sWorkingGroup 1 on the principle of subsidiarity):The Group considered that as the principle of subsidiarity was a principle of anessentially political nature,implementation of which involveda considerable marginof discretion for the institutions(considering whether shared objectives could"better" be achieved at European level or at another level), monitoring of compliancewith that principle should be of an essentially political nature and take place beforethe entry into force of the act in questionWith the entry into force of the Lisbon Treaty, this subsidiarity-check has beenanchored in the TEU (Article 5 as well as Protocol No.1 on the role of NationalParliaments in the European Union).It could be argued that the assessment of European added value is of political natureas well, and that the need for “a considerable margin of discretion for the institutions”is obvious also in this context.3. Europe is not a zero-sum gameEuropean added value is hard to define and rarely quantifiable. However, there is aconsensus that European action has added value: European integration is not a zero-sum game.Maintaining peace on our continent and other obvious advantages of Europeanintegration are difficult to assess in monetary terms. Nevertheless they can beconsidered undisputable elements of European added value.Some studies have tried to calculate the benefits of integration. For instance, ananalysis of the economic benefits of the internal market comes to the conclusion that“theenlarged Internal Market (including liberalisation of network industries) is animportant source of growth and jobs. As a result of the progress made over the period1992-2006 in achieving an enlarged Internal Market of 25 Member States, GDP andemployment levels have increased significantly. The estimated "gains" from theInternal Market in 2006 amount to 2.2% of EU GDP (or 223 billion euro) and 1.4%of total employment (or 2.75 million jobs).”4The recent undertaking to install a European External Action Service will also createtangible savings, because many of the current diplomatic services representing the 27Member States will be replaced.5It could be argued that EAV is not the right tool to make political choices. Whendeciding between different policies competing for scarce resources, focussing solelyon EAV can lead to comparing apples with pears.

45

Commission staff paper, DG ECFIN(2007):The same is possibly true for some of the European agencies, at least in cases where they actuallyreplace similar bodies on national level (e.g. the Office for Harmonisation in the internal market, whichis responsible for European Trademarks)http://ec.europa.eu/dgs/secretariat_general/evaluation/docs/decentralised_agencies_2009_part1_en.pdf

3

However, even if quantitative assessments remain problematic, the concept of EAV isvaluable for justifying the choices made. In addition, it can be used, at least on aqualitative basis, when it comes to defining the best instruments for a given aim, oncethe basic political choice has been taken, or as a management tool used for comparingalternatives within a given policy.4. The concept of European added value in relation to the current MFFDuring the preparation of the current MFF 2007-2013, the concept of added valueplayed a prominent role.In its Communication "Building our common Future", the European Commissioninsisted that "isnot about redistributing resources between Member States. It is abouthow to maximise the impact of our common policies so thatwe further enhance theadded value of every euro spent at European level"6.In its meeting of 16/17 December 2004, the European Council confirmed that "(...)policies agreed in accordance with the Treaty shall be consistent with the principlesof subsidiarity, proportionality and solidarity. They should also provide added value(....)".7In its resolution on Policy Challenges and Budgetary Means of the enlarged Union2007-2013, also the European Parliament underlined that "theFinancial Perspectivecan allow for balanced development of the financial resources allocated to the Unionprovided that they are used for actions with real European added value, clearlydefined priorities and visibility for citizens (...).8"6

The choices to be made on the next financial perspectives are not just about money. It is a question ofpolitical direction, to be made on the basis of a clear vision of what we want to do. These choices willdetermine whether the European Union and its Member States are able to achieve in practice whatEuropean people expect.This means a new phase for the Union’s budget. It is not about redistributing resources betweenMember States. It is about how to maximise the impact of our common policies so that we furtherenhance the added value of every euro spent at European level(COM(2004) 101 final).7

The European Council confirmed that the new Financial Framework, to be agreed in comprehensivenegotiations, should provide the financial means necessary to address effectively and equitably futurechallenges, including those resulting from disparities in the levels of development in the enlargedUnion. Policies agreed in accordance with the Treaty shall be consistent with the principles ofsubsidiarity, proportionality and solidarity. They should also provide added value. Expenditure forindividual policy areas must be seen in the context of the overall expenditure level, and suchexpenditure must be seen in the context of the overall negotiation including the question of ownresources.European Council, Presidency Conclusions–Brussels, 16/17 December 20048

7. Is convinced that the Financial Perspective can allow for balanced development of the financialresources allocated to the Union provided that:-they are used for actions with real European added value, clearly defined prioritiesand visibility for citizens,-they optimise concentration and complementarity with actions run at national,regional and local level to limit as much as possible the burden on taxpayers,-they are spent under rules of sound financial management, focusing on efficiency andeffectiveness; notes that expenditure effected at European level may give rise to

4

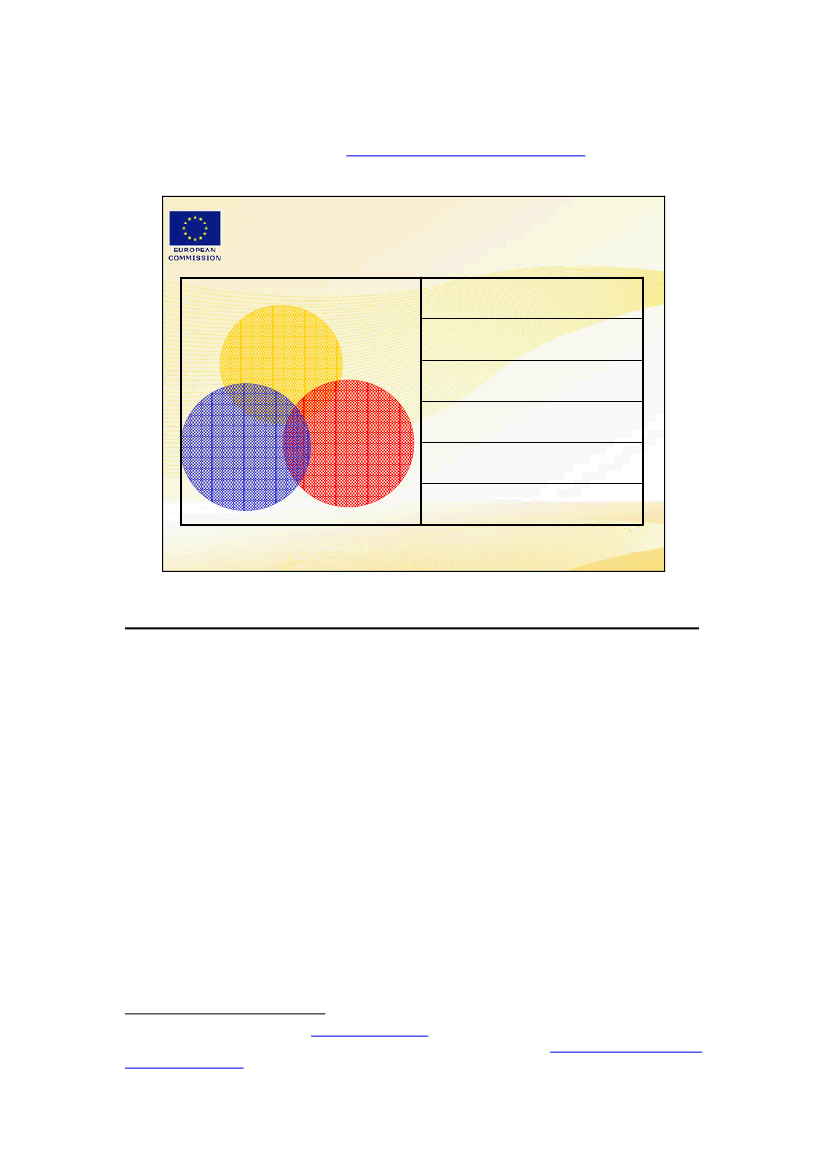

More recently, the European Parliament declares being "convincedthat EU spendingshould concentrate on policies with a clear European added value, fully in line withthe principles of subsidiarity, proportionality and solidarity; recalls that in a time ofcrisis this added value is measured largely in terms of the fundamental principle ofsolidarity between European peoples"9According to the Commission President Barroso, "Europe offers real added value",but "we need to spend our money where we get the most value for it."10TheCommission proposes that EU spending should "meet the added value test "when itfulfils three conditions:---policy relevance (the spending addresses the Union's key objectives)subsidiarity (transnational or cross-border actions, economies of scale)proportionality (assessment of effectiveness and efficiency of delivery)

Passing the Added Value TestPolicy prioritiesWhat do we want?

SubsidiarityProportionalityWho should do it?

EffectivenessQuality of spendingHow do we want it?

EU action should provide clear additional benefits compared to actionsby individual Member States:achieve EU policy objectives,show solidarity, etc.Heads of Representation, Lisbon 12 June 2007

Source: European Commission

savings at national level, in particular because such expenditure makes foreconomies of scale or may generate revenue at national level;(2004/2209(INI)) as adopted on 8 June 20059

European Parliamentresolution of 25 March 2009on the Mid-Term Review of the 2007-2013Financial Framework (2008/2055(INI))10

José Manuel Barroso: Debate on the State of the Union.European Parliament, 07.09.2010

5

In addition, it should be highlighted that European added value can be generated notonly by spending European expenditure, but also by coordination of national policiesand by European legislation (seeCommission roadshow presentation).

Subsidiarity and proportionality inpracticePrinciple of proportionalityPrinciple of subsidiarityTransnational dimensionExpenditure

Economies of scaleCritical mass requirementsLegislationCoordination

Common preferencesLow coordination costs

Not all EU policies require EU spending12 June 2007Heads of Representation, LisbonSource: European Commission5. European added value as operational tool in management and implementationCommission Services are required to assess "the added value of Communityinvolvement" in the framework of anex-ante evaluationin the preparation ofproposals for new or renewed Community actions.11.In addition, in the yearly "Activitystatementsof operational expenditure", issued asworking document along with the DB, the Commission describes the "EU addedvalue of the activity" for each chapter of the Commission's expenditure. At first sight,the methodology for assessing European added value seems to vary significantlybetween the policy areas.For instance, the added value of EuropeanEnergy policyis described by contributingto the aims of increasing the "security of energy supply", gradually "establishing theenergy internal market", "contributing to sustainable development by rational use ofenergy resources and the development and connection of renewable energy sources",increasing the interconnection of energy networks and harmonising the managementof the European electricity grid,.... In the context of "TEN-Energy, the EuropeanCommunity plays a role of catalyst of the efforts made by the member states and theelectric and gas companies".11

Implementing rules of theFinancial regulation(Commission Regulation (EC, Euratom) No2342/2002), Article 21; DG BUDG (2005): Evaluating EU activities.A practical guide for theCommission services;

6

Beyond the general requirements of ex-ante evaluation, several EU policies requireproof of European added value in the context of the selection of projects:Research:Since FP5, the concept of European added value is part of the legislativeFramework programme for research. It constitutes a binding criterion for the selectionof projects (and, to a lesser extent, for the formulation of research programmes). Ingeneral it is agreed that EU funded research has a "high added value by encouragingresearches to cooperate across national boundaries and to share complementary skillsand knowledge", that it "promotes competition in research, leading to higher qualityand excellence" and that it "may make possible projects that, because of theircomplexity and scale, go beyond what is possible at national level"12.However, when it comes to monitoring and evaluating European added value in aquantitativeway for specific programmes and projects, experts speak about a"missionimpossible"13Culture/Communication:European added value shall be described by the applicantsto programmes such as "Europe for Citizens". While there is a broad consensus thatcultural and educational exchange programmes like Lifelong Learning have a strongadded value by increasing citizens’ mobility and by contributing to a "Europeanidentity", it seems that a quantitative assessment of European added value is ratherproblematic.6. From Lisbon Strategy to EU 2020: The political semantics of European addedvalueEuropean integration develops in a continuous tension between a national and aEuropean perspective, in a changing balance between (evolving) interests of differentmember states and a fragile interinstitutional setting.Therefore it could be discussed in the SURE committee how the connotations linkedto the concept of European added value in 2004 (Lisbon agenda) have developed withregard to the current political priorities of the EU. This debate is held in theframework of EU 2020 (including concepts like smart, sustainable and inclusivegrowth), but it will probably also need to address issues linked to the changes inEuropean decision making and instruments through the Lisbon Treaty (climatechange, energy, EEAS, space policy). In addition, current political priorities are likelyto be discussed in regard of their European added value (e.g. the increased Europeancoordination of the budgets of the member states14).Finally, the committee might also consider useful to discuss policy fields whereEuropean added value could be created by strengthening the synergies betweennational and European activities (European development fund, common foreignpolicy, etc), in a view to overcoming the focus on net balances of member states’contributions and revenue.1213

G. Cipriani: Rethinking the EU budget. CEPS (2007)Yellow Window Management Consultants (2000): Identifying the constituent elements of theEuropean Added Value (EAV) of the EU RTD programmes: conceptual analysis based on practicalexperience. Study commission by DG Research, European Commission14http://consilium.europa.eu/uedocs/cms_data/docs/pressdata/en/ecofin/116306.pdf

7

Annex: ReferencesCentre for European Policy Studies (CEPS) (2008):Energy Policy for Europe:Identifying the European Added-ValueCouncil of European Municipalities and Regions: The Added-value of EuropeanUnion Cohesion Policy (2002);http://www.ccre.org/bases/T_599_9_3524.pdfEuropean Commission (2004): Communication from the Commission to the Counciland the European Parliament: Building our common Future. Policy challenges andBudgetary means of the Enlarged Union 2007-2013.COM(2004) 101 finalEuropean Commission (2007):Economic papers N� 271:Steps towards a deepereconomic integration: the Internal Market in the 21st century. A contribution to theSingle Market Review.European Commission (2008):Financing the European Budget.Study for theEuropean Commission, Directorate General for Budget.European Commission (2009b):An Agenda for a reformed Cohesion Policy.Aplace-based approach to meeting European Union challenges and expectations.Independent Report prepared by Fabrizio Barca at the request of Danuta Hübner,Commissioner for Regional Policy.European Commission (2009b): Evaluation of the EU decentralised agencies in 2009.Volume I – Synthesis and recommendationsEuropean Commission (2010): Draft General Budget of the European Commission forthe Financial Year 2011. Working document Part 1: Activity statements of operationalexpenditure.European Council (2002):Council Resolution of 19 December 2002implementingthe work plan on European cooperation in the field of culture: European added valueand mobility of persons and circulation of works in the cultural sectorEuropean Council (2004):Presidency Conclusions– Brussels, 16/17 December 2004European Parliament (2005): European Parliamentresolution of 8 June 2005onPolicy Challenges and Budgetary Means of the enlarged Union 2007-2013;European Parliament (2009a): European Parliamentresolution of 25 March 2009onthe Mid-Term Review of the 2007-2013 Financial Framework (2008/2055(INI))European Parliament (2009b): European Parliamentresolution of 24 March 2009oncomplementarities and coordination of cohesion policy with rural developmentmeasures (2008/2100(INI))European Parliament (2010a): Committee on Budgets: A. Lamassoure:Workingdocument DT\815212on financing the 2020 Agenda despite the budgetary crisis

8

European Parliament (2010b): Committee on Regional Development:Draft PositionPaper on the future cohesion policy,July 15, 2010:European Parliament (2010c):Creating greater synergy between European andnational budgets.Study drafted by Deloitte Consulting, at the request of theCommittee on BudgetsSapir, A (2003):An Agenda for a Growing Europe.Report of an Independent High-Level Study Group established on the initiative of the President of the EuropeanCommission.Tarschys, D (2005):The Enigma of European Added Value(SIEPS)Yellow Window Management Consultants (2000): Identifying the constituentelements of theEuropean Added Value (EAV) of the EU RTD programmes:conceptual analysis based on practical experience. Study commissioned by DGResearch, European Commission

9