Miljø- og Planlægningsudvalget 2009-10, Det Energipolitiske Udvalg 2009-10

MPU Alm.del Bilag 173, EPU Alm.del Bilag 85

Offentligt

SUSTAINABLEENERGY SCENARIOS

20092009

Boosting the Top of EuropeEnergy Perspectives for the Baltic Sea Region

Setting an agenda for the future

Ea Energy AnalysesPrepared by:Ea Energy AnalysesFrederiksholms Kanal 1, 1st1220 Copenhagen KDenmarkPhone: +45 88 70 70 83Fax: +45 33 32 16 61Email: [email protected]Web: www.eaea.dkInitiated by:Baltic Development ForumNygade 3, 5th1002 Copenhagen KDenmarkPhone: +45 70 20 93 94Fax: +45 70 20 93 95Email: [email protected]Web: www.bdforum.orgSponsored by:Nordic Council of MinistersNordic CouncilFabrikant Mads Clausens Fond, Danfoss

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

3

Table of contentsForeword and prefacesForewordPreface by the EU Energy Commissioner Andris PiebalgsPreface by the Baltic Sea Energy Cooperation (BASREC)Group of Senior Energy Officials (GSEO)Preface by the Baltic Sea Parliamentary Conference WorkingGroup on Energy and Climate ChangePreface by the Union of Baltic Cities Energy Commission1 Summary and recommendations1.1 Introduction1.2 Scenarios in phase I and phase II1.3 The Baseline scenario1.4 Three alternative policy scenarios1.5 Dialogue with stakeholders1.6 Next steps2 Scenarios and policy targets2.1 One Baseline scenario and three policy scenarios2.2 Existing subsidies and energy taxes3 Modelling tool4 Key assumptions for the scenarios4.1 Fuel prices4.2 Transmission capacity4.3 Electricity demand4.4 Existing generation capacity4.5 New generation capacity5 Scenario analyses5.1 Baseline scenario5.2 Regional RE target5.3 Improved efficiency scenario5.4 30%@COP155.5 Analysis: CO2and RE targets6 Case analysis of Kriegers Flak7 Screening of new interconnectorsAnnex 1: The consultation and presentation process44679101111131724313234373839414142434445555566707478818385

4

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

Foreword and prefacesForewordGlobal attention is firmly directed towards the Baltic Sea Region due to UNClimate Summits in Copenhagen in December 2009 and in Poznan in 2008.The UN Summit in Copenhagen takes place in parallel with the Swedish EUPresidency. These high-level events are unique opportunities for the countriesin the region to illustrate to a broader audience the political importance of theregion by highlighting the Baltic Sea cooperation and regional solutions toglobal challenges.Climate change and energy consumption are challenges that influence almost allaspects of our daily life. Global challenges regarding reduction of green housegasses, increase of renewable energies and energy efficiency need to be tackledon all levels – private households, national, European and global levels. Oftenenergy co-operation onregionalorsub-regionallevels can indeed providevery positive results that leave each country better off when implementing theEU’s or the UN’s targets on climate change and energy, as well as in ensuringgreater security of energy supply. This has been the basic assumption behindthe present report, not least based on the Nordic experience. The Baltic SeaRegion’s specific character in terms of many different energy sources and theindividual countries’ energy-mix supports implicitly such an assumption.The present report discloses some of the advantages of enhanced energy co-operation in the Baltic Sea Region based on facts and data. It illustrates thatthere is a huge potential for cost-efficient energy savings and energy efficiencymeasures through a stronger coordination of the energy policies across theregion.In preparing the report, data on energy generating facilities in all Baltic SeaStates have been collected and used in the open and transparent analyticalmodels – Stream and Balmorel. These models were also used in the preparationof national/regional policies in Denmark and in the European Parliament andthey similarly proved to be useful and interesting in the Baltic Sea Region whenlooking at the region as one integrated energy system. With the different energydata collected a unique database has been created. It can now serve as a platformfor identifying and implementing very specific energy projects in the Baltic SeaRegion.The analytical and empirical results and findings have been presented for anddiscussed with different public and private stakeholders in the region in order toanchor the different energy scenarios, results and recommendations. We hopethat this final report and its recommendations can continue to serve as a keypoint of reference in the further discussions on energy planning in the Baltic

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

5

Sea Region, not least in the framework of BASREC, the Nordic-Baltic energycooperation through the Nordic Council of Ministers as well as initiatives underthe EU strategy for the Baltic Sea region. First and foremost, the report willform the basis for the regional energy discussions at the Baltic DevelopmentForum Summit, 5-6 October in Stockholm. And it will provide an input to theNordic Council’s 61stsession, 27-29 October in Stockholm.The analysis and conclusions of the report are those of the authors and donot necessarily reflect the views of the Nordic Council of Ministers or BalticDevelopment Forum. However, we are convinced that the report will beinspiring. We wish you all good reading.

Copenhagen, 15 September 2009

Halldór ÁsgrímssonSecretary GeneralNordic Council of Minsters

Hans BraskDirectorBaltic Development Forum

6

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

Preface by Mr Andris Piebalgs,Commissioner for EnergyAt the 2007 Baltic Development Forum’s Summit in Tallinn, it was concludedin the session on energy and climate change in which I took part– together withPrime Minister Fredrik Reinfeldt, Prime Minister Matti Vanhanen and CEO ofForum Michael Lilius – that there was a need to draw up a paper that couldhelp the governments realize the vision of closer and more efficient energycooperation in the Baltic Sea Region. The Baltic Sea Region indeed has a hugepotential for implementing energy projects that are of wider importance due totheir potential and diversified energy-mix.I am therefore glad to acknowledge the work and effort that has been investedin elaborating this report on Sustainable Energy Scenarios. I have had thechance to observe the process since the preliminary results were presented tome in connection to the BASREC Ministerial conference in February 2009. Iwas introduced to the two overall scenarios for regional co-operation basedon a “small-tech and big-tech” approach. I find the approach useful to presentdifferent sc enarios as a means of involving different stakeholders in agreeingon the most pressing energy projects and priorities that can be beneficial for alarger group of countries.As I mentioned in February at the Ministerial Conference, we indeed need bothsmall-tech and big-tech solutions if we are to successfully implement the EU’s20-20-20 targets. We must not ignore the importance of small-tech solutions.As it is issued while the discussions on the EU strategy for the Baltic Sea areatake place, the report is very timely. The Baltic Sea Region has the potential toshow to the rest of the world how many of the energy and climate challengescan be solved intelligently. The region could become home of many lighthouseprojects – like the Windmill Park at Krieger’s Flak that the Commission hasdecided to support. In this respect, the present report is an important tool whichI hope will be used by all stakeholders in the region, and beyond.As European Commissioner responsible for Energy, I am very pleased by theinitiative taken to draw up this report and by many results in the report.With every good wish for a successful follow-up,

Andris PiebalgsEU Commissioner for Energy

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

7

Preface by the Bal c Sea Energy Coopera on(BASREC) Group of Senior Energy Officials (GSEO)In spite of the current economic downturn the Baltic Sea Region has a greatpotential for developing into a more coherent and prosperous economic regionin the aftermath of the crisis. It depends on the future policy design and theability of the countries to benefit from closer cooperation on issues that enhancecompetition, green growth and job creation and cater for the climate.Energy is crucial when it comes to designing policies that meet the futurechallenges of developing renewed growth and prosperity in the region,competition and climate friendly new technologies.Keen political interest is taking in the Baltic Sea region in these years providinggreat opportunities for the region to shape its energy policies to develop andobtain prosperity.The ministers of the Baltic Sea Energy Cooperation (BASREC) have recentlyagreed to continue and strengthen the transnational energy cooperation in orderto make contributions to stability, growth and development in the region bypromoting market-based, secure, competitive and sustainable energy systems.The EU has taken initiatives to abolish the energy isolation of the Baltic Sea statesfrom the EU energy markets by the endorsement of the Baltic Energy MarketInterconnector Plan (BEMIP) in June 2009. BEMIP is a plan for the futuredevelopment of the energy markets in the region. The EU has also launched theEU Economic Recovery Plan which gives substantial financial support to someof the essential BEMIP infrastructure projects in the region.The EU will also launch a Strategy for the Baltic Sea Region in 2009. Energyplays a central role in this strategy and the implementation of BEMIP will beone of the essential actions in this energy strategy for the Baltic Sea Region.Past experience has shown that political support is crucial to success indeveloping coherent and common energy policies and strategies for the region.The present report on Sustainable Energy Scenarios for the Baltic Sea regionclarifies the strengths of the region and the opportunities for shaping coordinatedregional energy policies and solutions that can meet the triple challenges ofrenewed growth, energy security of supply and climate change for the region.The report shows that the region has a sufficient potential of renewables, energyefficiency and new efficient technologies to become a low-emission growthregion with secure energy supplies in 2030.The report underlines that strong and dedicated cooperation on achieving theEU 20-20-20 goals will bring substantial economic benefits to the region as willfurther integration of the infrastructure in the region.

8

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

The present report has been initiated by Baltic Development Forum, preparedby Ea Energy Analyses and financed by Nordic Council of Ministers, NordicCouncil, and Fabrikant Mads Clausens Fond, Danfoss. The conclusions arethose of Ea Energy Analyses and do not necessarily represent the opinions ofthe organisations that have initiated the report. The report provides a good anduseful background and shows the great opportunities for designing co-ordinatedenergy strategies and policies to our common urgent challenge for the benefitof the region. In that capacity it will be included in the basis for the future co-operation in BASREC.

Hans Jørgen KochDeputy State SecretaryChairman of the BASREC Group of Senior Energy Officials1 July-30 June 2008-09

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

9

Preface by the Bal c Sea Parliamentary ConferenceWorking Group on Energy and Climate ChangeLife on Earth is impossible without production, conversion and transmission ofenergy in all its diversity. Those who are able to find energy in the environmentand use the resources rationally are better fit to meet the challenges of life andare more likely to survive over long periods of time. Today, energy issues havea higher priority in our daily life than ever before. On one hand, fuels which fedeconomies and countries throughout the last century are becoming scarce dueto intensive and often inefficient use, on the other hand, wasteful use of energyand fuels in just a few human generations have released back to the environmentchemical compounds which cause a warming of the Earth’s atmosphere, leadingto irreversible catastrophic changes in the foreseeable future.Effects on the climate are global and not restricted by national or politicalborders, thus in order to mitigate and stop climate change, our efforts must beglobal, agreements regional and actions - individual. The Baltic Sea Region joinscountries with very different economies and energy resources, but for naturalor historical reasons there are still gaps and barriers between different areas.This report, using transparent analytical instruments, weighs today’s situationand draws scenarios for a common future. The diversity of fuels and energyproduction is seen as an advantage rather than an obstacle, as it has created awide range of practices and know-how in the fields of energy production andsustainable use. With dedication and co-operation this unique opportunity canbe developed into a world-leading concept of energy efficiency supporting ourimminent efforts to stabilize the environment of our overheating planet Earth.As a marine biologist I have learned how delicate the energetic balance of globalenvironment is, and I have seen the consequences of recent developments inhuman energy consumption. This report looks several generations ahead,helping us to plan and secure our energetic future.

Mart Jüssi, MPChairman of the Estonian Parliament Environment CommitteeChairman of the BSPC WG on Energy and Climate Change

10

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

Preface by the Union of Bal c Ci esEnergy CommissionEnergy will be one of the defining issues of this century. A new global revolutionis needed in ways of how energy is used and supplied. We need this energyrevolution not only for stopping the green house gas emissions that cause climatechange, but also for generating jobs and new economic growth. Energy demandis soaring like never before as populations grow and economies start to take offagain. Millions of citizens in the new democracies around the Baltic Sea Region(BSR) are expecting to enjoy a lifestyle that definitely requires more energy.This report outlines how we as municipalities and cities can take concrete actionto meet this challenge. The technology and science is there – what is missingis a strategy and decisive measures on a local political level. The policies in theBSR related to energy and associated big tech infrastructure will increasingly bea national and regional concern. This report is visionary in its BSR integratedmarket approach. But its greatest value is that it defines the importance of theSmall Tech measures that can be taken on a local municipal level in order toimplement a better energy system and the thereby meet global and regionalenvironmental targets. This report definitely puts us citizens back in the driver’sseat and in charge of our own future.

Stefan WindhUBC Energy commission

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

11

1

Summary and recommenda ons1.1 Introduction

Baltic 21 Energy

In 1996-1998 the first comprehensive energy study for the Baltic Sea Region,Baltic 21 Energy, was carried out, investigating a sustainable energy developmentthe Baltic Sea Region. The study, carried out by authorities, non-governmentalorganisations and consultants, concluded, that a sustainable pathway wouldinclude energy savings in all sectors, reduction of losses in energy transformationand increased use of renewable energy and natural gas in the energy system inthe region.

Figure 1: The Baltic Sea Region: Denmark, Estonia, Finland, North East Germany, North West Russia,Kaliningrad, Latvia, Lithuania, Poland, Norway and Sweden.

Baltic Ring I and II

In the same period the electricity sector in the region carried out the first BalticRing study with the purpose of examining the benefits from stronger electricityinterconnectors in the Baltic Sea Region. In 2003, the second Baltic Ring studywas concluded, this time with more focus on market integration. Both studiesconcluded that a stronger cooperation between the stakeholders around theBaltic Sea would benefit the development of the electricity sector.In recent years the energy agenda has changed in Europe. The EU countrieshave placed a strong focus on meeting the challenges from climate change. Theenergy sector has to comply with tough targets for the reduction of greenhousegas emissions, targets for deployment of renewable energy sources and targetsfor energy efficiency improvements. At the same time, security of fuel supplyhas become an even more urgent topic on the energy agenda.

New energy agenda

12

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

This agenda calls for a new basis for strategic decisions and an updated overviewof the possibilities for developing the energy system in the Baltic Sea Region.It is particularly relevant to explore the potential in the region for developingregional solutions to the energy challenges and to identify projects that couldbenefit the region as a showcase for sustainable energy development andbecoming frontrunners in innovative solutions through regional cooperation.BEMIP and the EUBaltic Sea RegionstrategyIn June 2009 the eight Baltic EU member states reached agreement on a BalticEnergy Market Interconnection Plan (BEMIP), underlining the urgent needfor connecting the Baltic region with the EU. The BEMIP is also identifiedas a flagship project in the broader context of the EU Strategy for the BalticSea Region, presented by the EU Commission on 10 June 2009. The plan andstrategy highlight the need for a stronger regional co-operation in the field ofenergy in order to harvest the potential synergies in the region.In this context Baltic Development Forum (BDF) has initiated the study‘Enhanced regional energy cooperation in the Baltic Sea Region. The study isa multi-client study, financed by Nordic Council of Ministers, Nordic Council,Baltic Development Forum and Fabrikant Mads Clausens Fond, Danfoss andcarried out by the consulting company Ea Energy Analyses.The study has two parallel objectives:1) To promote a common energy agenda for the Baltic Sea Region through theinvolvement of key stakeholders;2) To provide a substantial basis for discussion of different energy scenariosfor the region based on an analysis of energy data of all the countries in theregion.The study consists of three phases. The first phase (mid 2008 – ultimo 2008)included an overview of the current energy situation, collection of data forthe region and setting up of scenarios for the future regional energy system.Phase II of the project (beginning of 2009 – mid 2009) includes more detailedscenario analyses of the electricity and district heating markets and a prioritizedlist of regional projects/policies to promote the region as a sustainable region.A vital part of this phase has been to collect data for the whole region, includingNorthwest Russia. A planned phase III will develop strategies for the deploymentof regional projects, identify activities for regional knowledge sharing in the fieldof sustainable energy, and outline the possibilities for the industry to be frontrunners in the development of new energy technologies.Dialogue with the stakeholders on the energy scene in the Baltic Sea Region hasbeen an important part of the study process. Preliminary results from the studyhave been presented and discussed at a number of occasions. See Annex 1 formore details about the stakeholders’ involvement.Phase II of the study is documented in two reports. This summary report gives anoverview of the approach, the results and recommendations from the analyses.More detailed information is provided in the background report.

The present study

Objectives

Three phases

Dialogue with thestakeholders

Summary report andbackground report

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

13

1.2 Scenarios in phase I and phase IIDifferent scenario techniquesIn the study, two different scenario techniques have been used.Phase I scenariosThe scenarios in phase I are inspired by a study for the European Parliament1,where the future composition of technologies in the energy system are based onbest estimates and visions for the development of a sustainable energy system.These estimates are then evaluated and fitted to meet the political targetsregarding CO2, shares of renewable energy and non-quantified objectivesregarding security of supply and different stakeholder involvements in thedecision process. The scenarios comprise the whole energy system includingthe transport sector.The scenarios in phase I were developed with STREAM, a bottom-up basedspread-sheet modeling tool looking at the energy flows of the region on anannual basis2.Phase II scenariosIn phase II, the scenarios focus on detailed analyses of the electricity and districtheating system in the Baltic Sea Region. The future composition of technologiesin the electricity and district heating system are determined by the energy marketmodel Balmorel3, developed as a part of the energy cooperation in the BalticSea Region in the late 1990-ties. The model decides which technologies shouldbe used, based on input of technical and economical data for the individualtechnologies and assumptions about the future fuel prices. The model calculatesa least cost solution for the whole system taking the given constraints regardinge.g. CO2-targets and shares of renewable energy into account.Both scenario techniques have their strengths and in a dialogue process, as thepresent study, the combination of the techniques gives valuable information tothe decision making process between the stakeholders in the region.

Phase I: Big Tech and Small Tech scenariosDataPhase I of the study focused on a description of the current situation in theenergy sector in the Baltic Sea Region and collecting data for the scenarios,including data for relevant new technologies that could be used in the futureenergy system in the region.In order to shed light on different pathways towards achieving the long-termstrategic goals of the region two essentially different developments have beenexplored through a so-called Small-tech scenario and a Big-tech scenario. Bothscenarios aim at achieving two concrete goals for 2030: reducing CO2emissionsby 50 % compared to the 1990 level and reducing oil consumption by 50 %compared to the present level.1 Future energy systems in Europe, STOA-20092 See. www.streammodel.org3 See www.balmorel.com

Targets

14Small-tech scenario

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

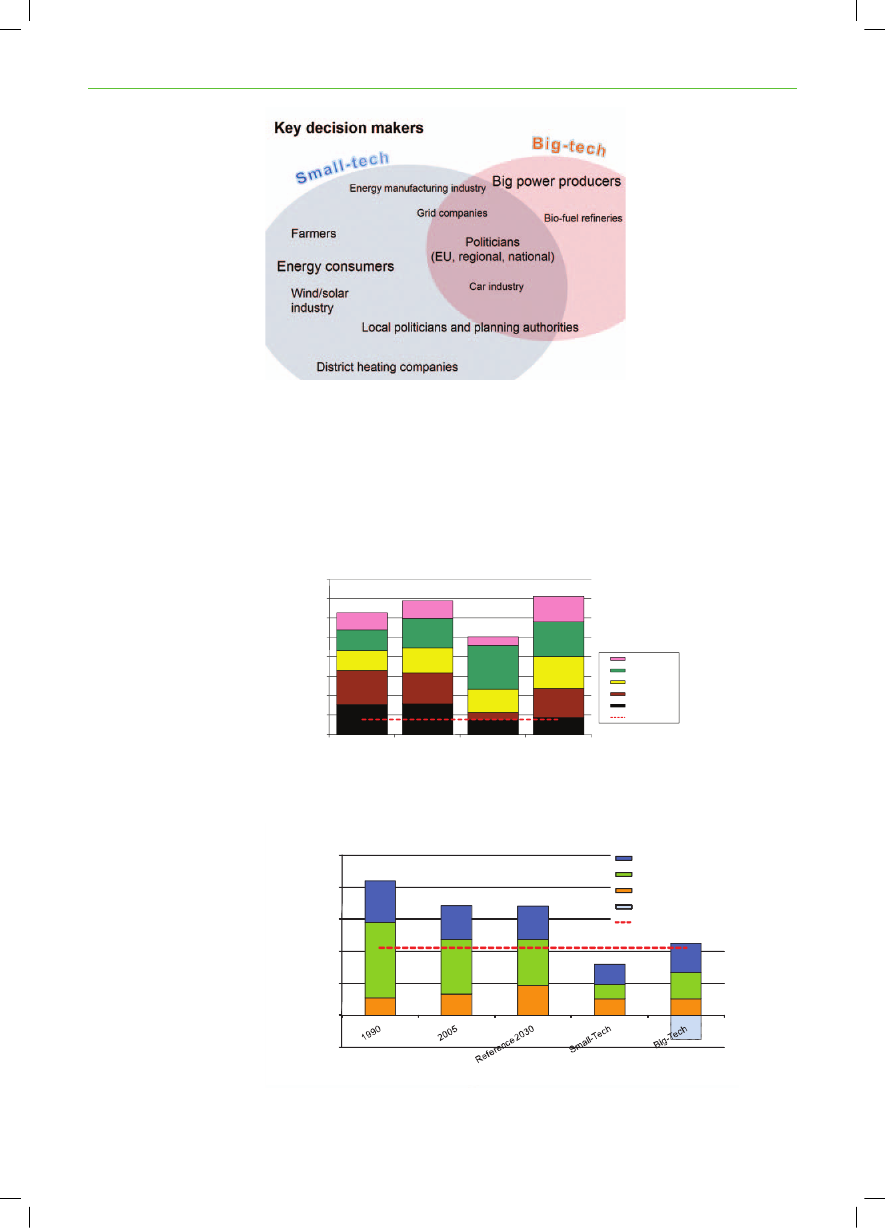

The Small-tech scenario focuses on distributed energy generation, energy savingsand efficient utilisation of energy through combined heat and power generation.This scenario assumes a high level of interconnection of the electricity gridsin the Baltic Sea Region to allow for the integration of a high share of windpower. So-called ‘smart grid technology’ and improved communication betweenthe different parts in the energy system play a key role in providing an optimaldispatch and efficient utilization of the energy infrastructure.The Big-tech scenario explores the opportunities of more centralised solutions.In the Big-tech scenario, almost all new coal and natural gas power plantsestablished from 2020 and onwards will be equipped with carbon capturestorage technologies (CCS). In addition, it is assumed that most new large coalpower plants commissioned in the period 2010-2020 are prepared for CCS andretrofitted in the subsequent decade. The nuclear power capacity will be increasedby 35 % compared to today. New nuclear generation capacity is presumed to bebuilt in Finland, Lithuania and Poland, and existing nuclear power plants inGermany, Sweden and North West Russia will continue generation.In both scenarios the transport sector undergoes fundamental changes in orderto comply with the target of 50 % oil reduction. In both the Small tech andthe Big-tech scenarios it is a critical assumption that the technical potentialsfor improving the fuel economy of conventional vehicles are partly realised.Moreover, in the Small-tech scenario, electric vehicles and plug-in hybridsdisplace oil consumption, and information and communication technologies areput in place to decrease the demand for “physical” transportation. In the Big-techscenario, in addition to the electrification of the transport sector 2ndgenerationbiofuels and natural gas are important means for reducing oil dependence.In the Big-tech scenario, the existing structure of the energy supply systemremains essentially unchanged, and the large suppliers of electricity become themain actors. Hence, the implementation of the Big-tech scenario depends onrelatively few decision-makers. Partnerships for the demonstration of the CCStechnology provide an obvious opportunity for regional cooperation in the Big-tech scenario.In the Small-tech scenario, citizens play an important role as active consumersof energy, changing energy behaviour according to price signals and investingin energy-efficient appliances and buildings; grid owners must develop theirsystems and the suppliers of energy will have to change sources graduallyfrom large power plants to renewables and to distributed units located closerto the consumers. In the Small-tech scenario the integration of fluctuatingenergy sources calls for a high level of cooperation on energy markets and newinfrastructure projects, particularly concerning off-shore wind. Local authoritiesand cities are crucial for the facilitation of district heating grids and sustainabletransport systems – and the need for more efficient supply and demandtechnologies provides business opportunities in many industry branches.

Big-tech scenario

Transport

Key decision makersin the two scenarios

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

15

Figure 2: Key decision makers in the Small-tech and Big-tech scenarios

Results

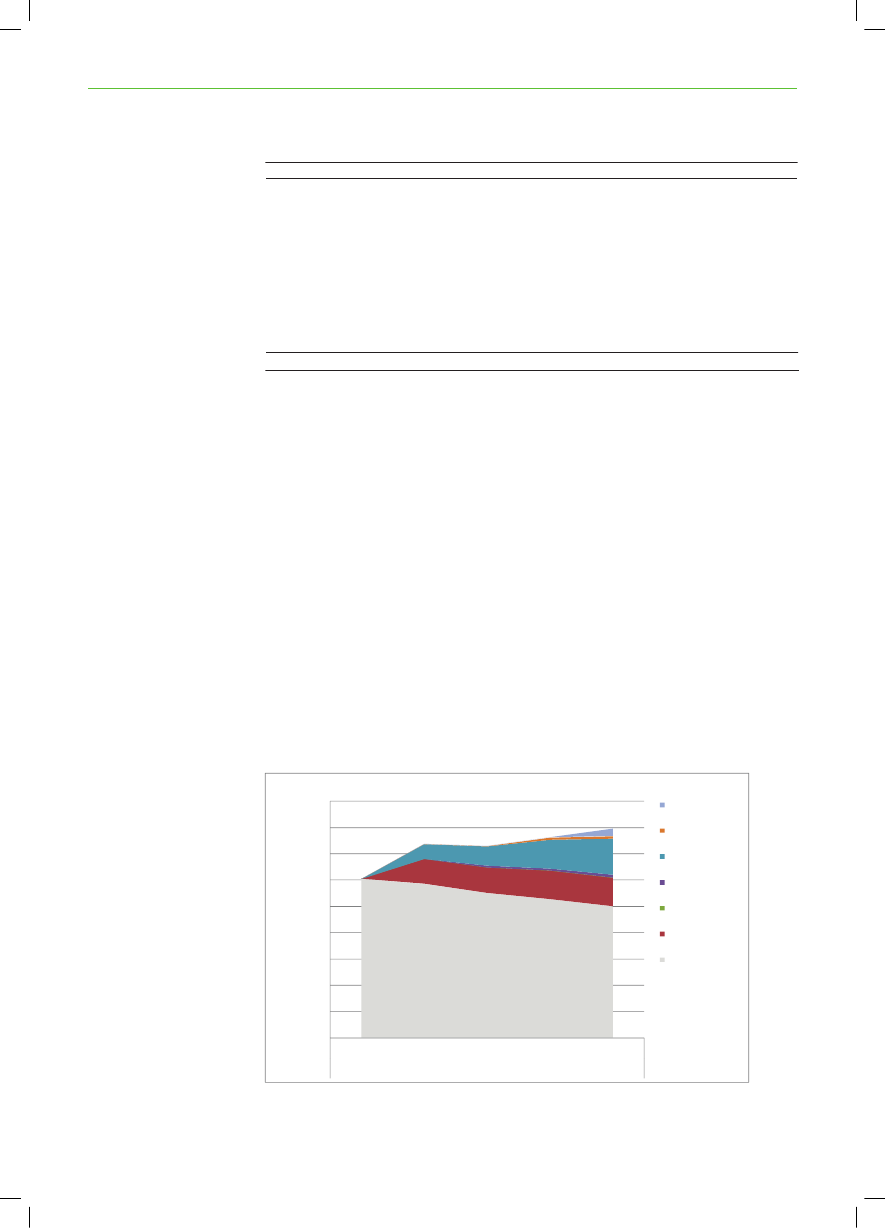

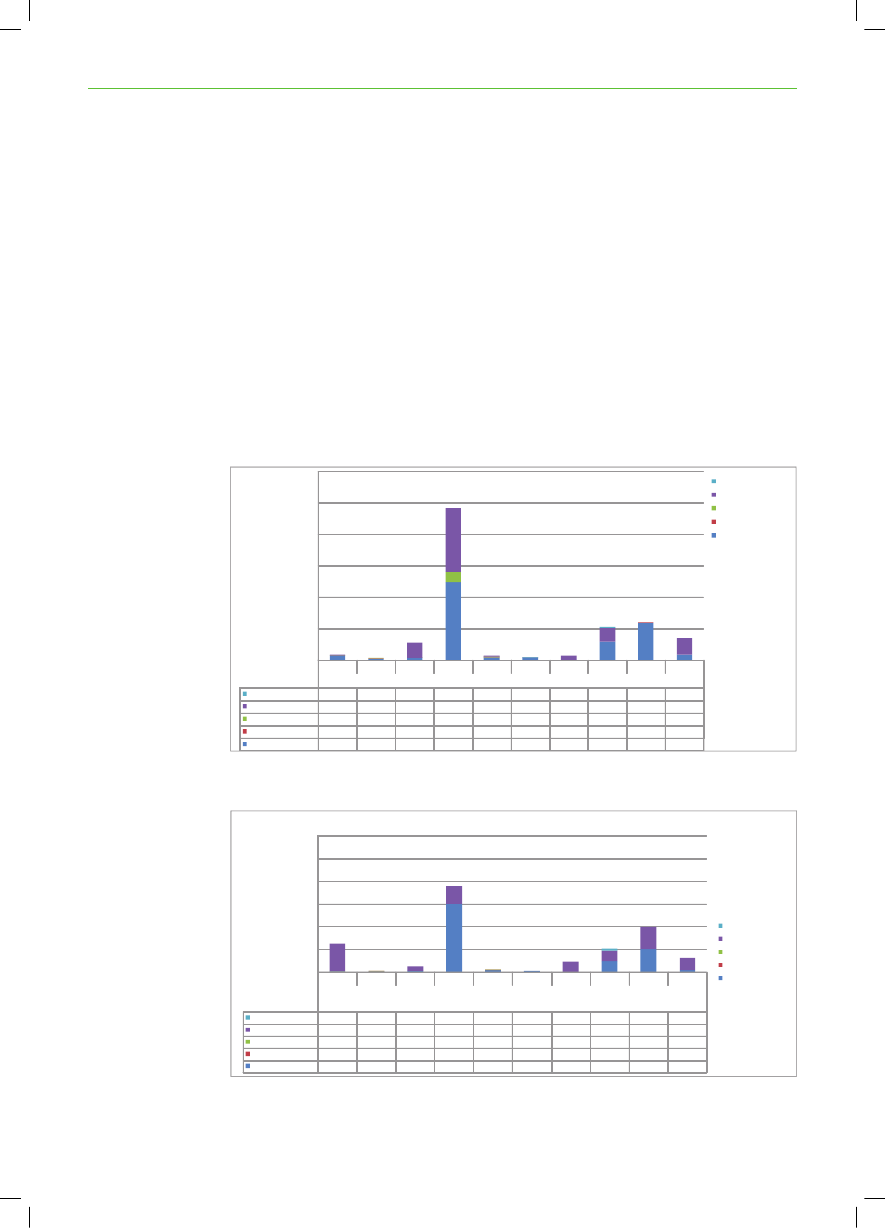

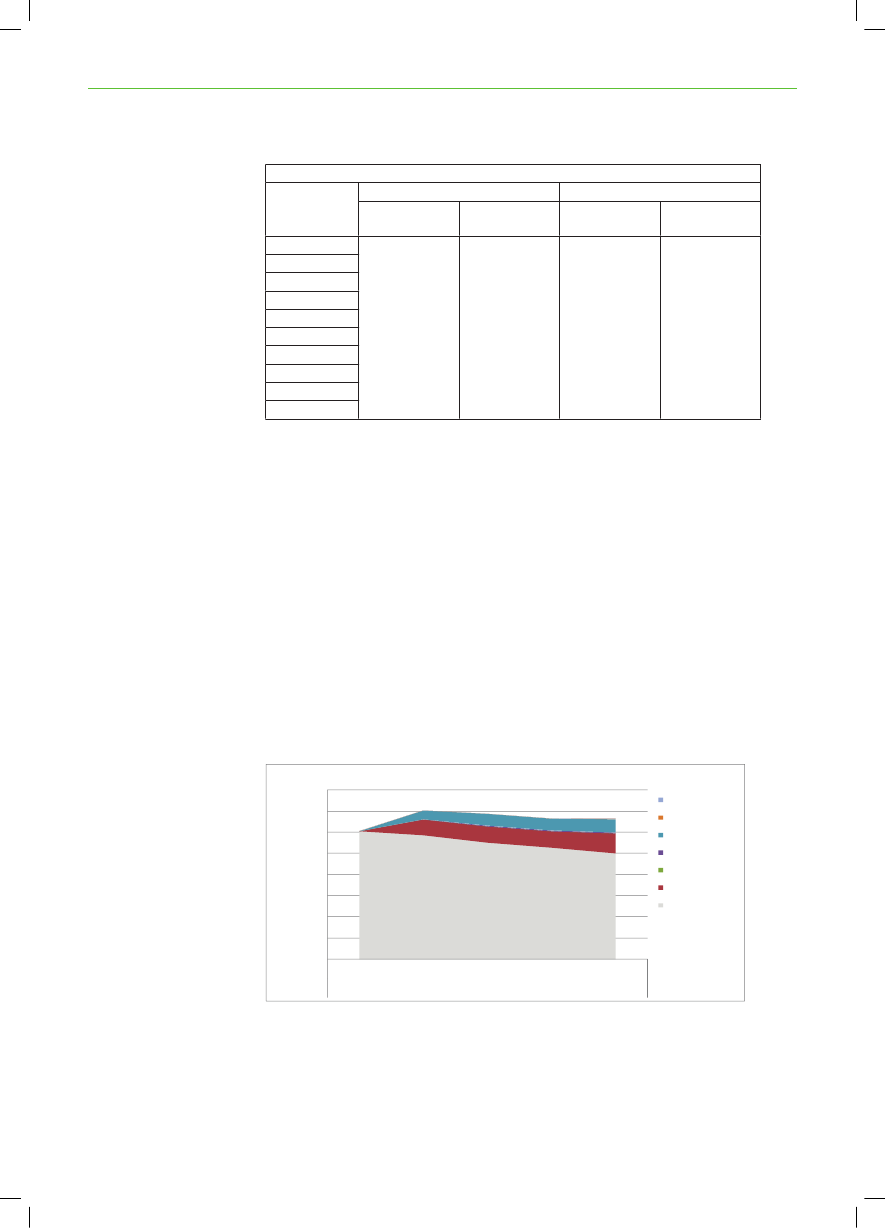

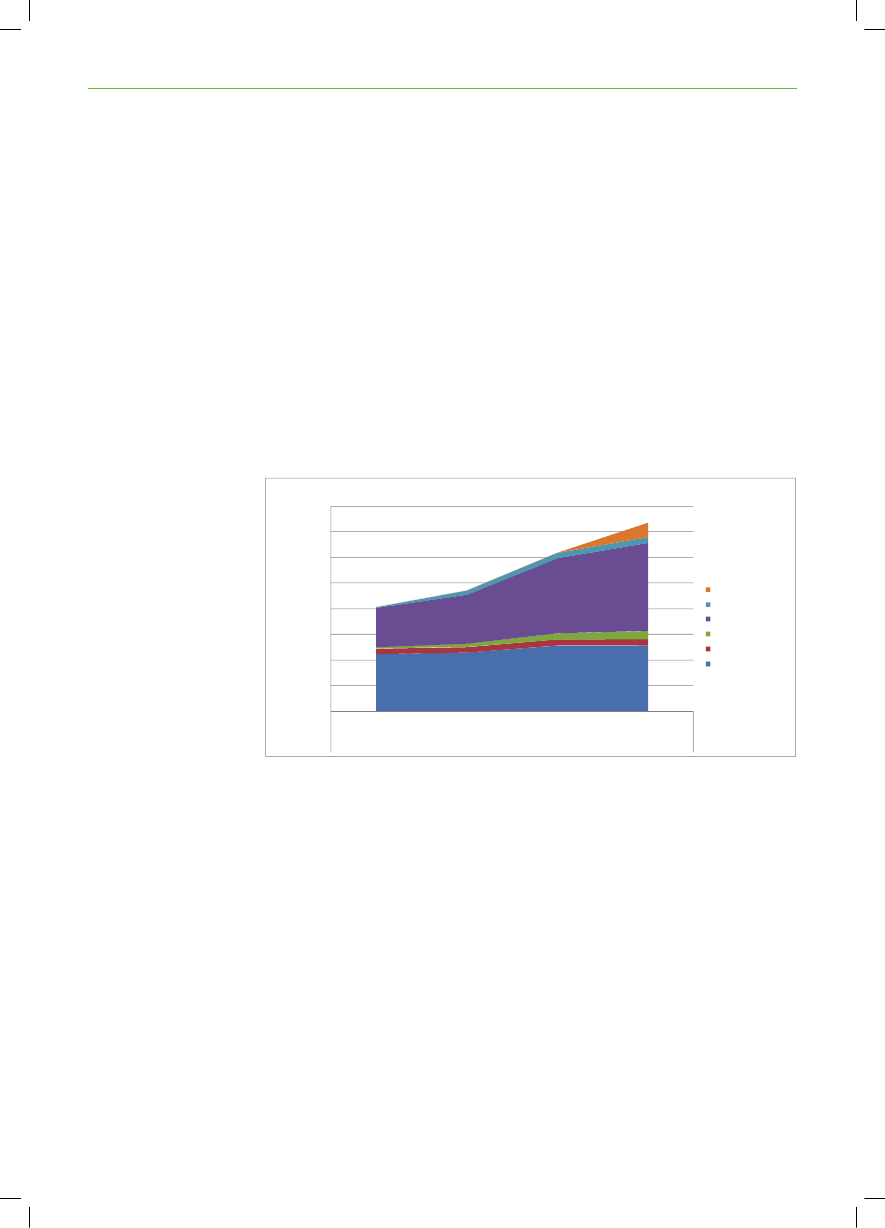

To illustrate the consequences of the two scenarios, the key indicators – thedevelopment in gross energy consumption and the emission of CO2– arecompared with historic data as well as with a reference for 2030 resembling themost recent projection from the European Commission.Gross energy consumptionPJ16.00014.00012.00010.0008.0006.0004.0002.000-NuclearRENatural gasCoalOil50% oil target

2005

Reference 2030

Small-Tech

Big-Tech

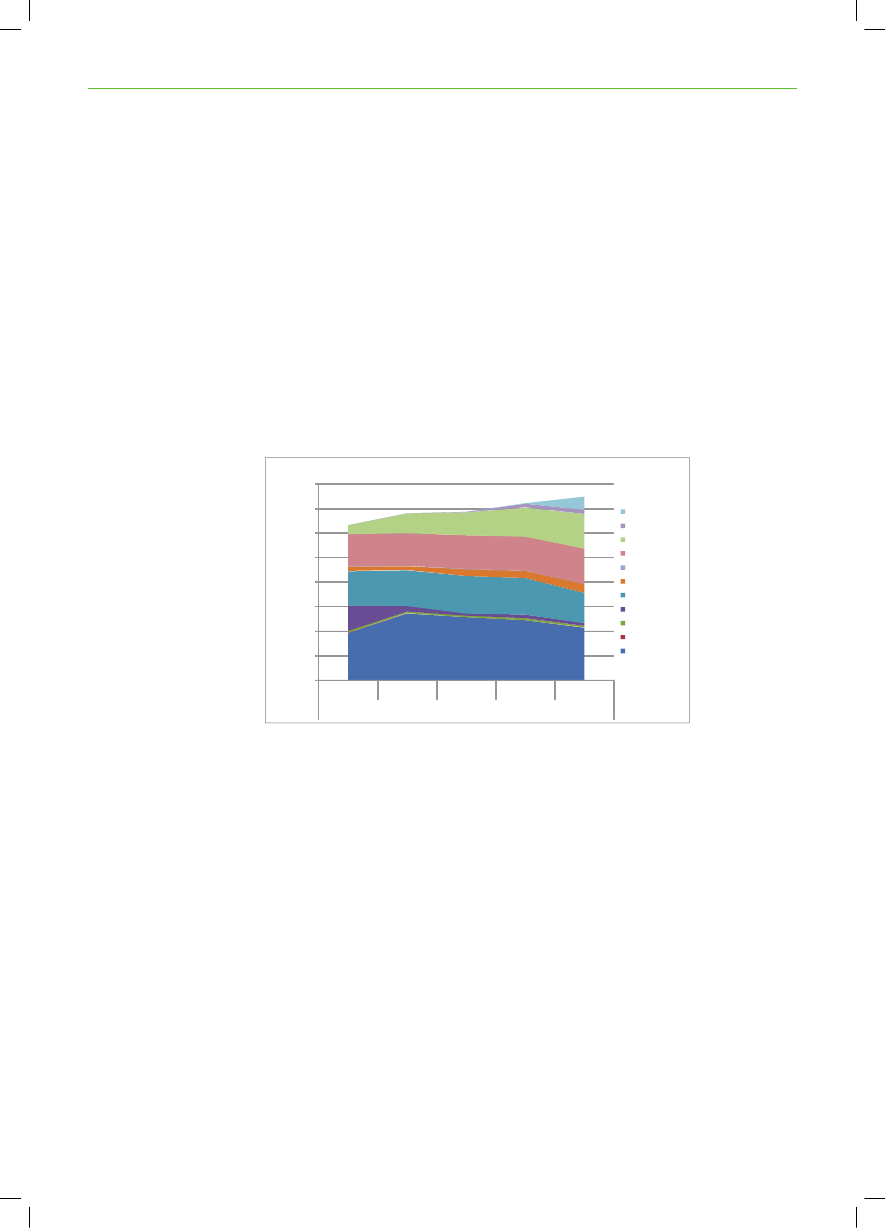

Figure 3: Gross energy consumption in 2005 and projections for 2030 (excluding fuels for non-energypurposes). Data is only included for North East Germany and North West Russia.Mt CO2 / year1.000

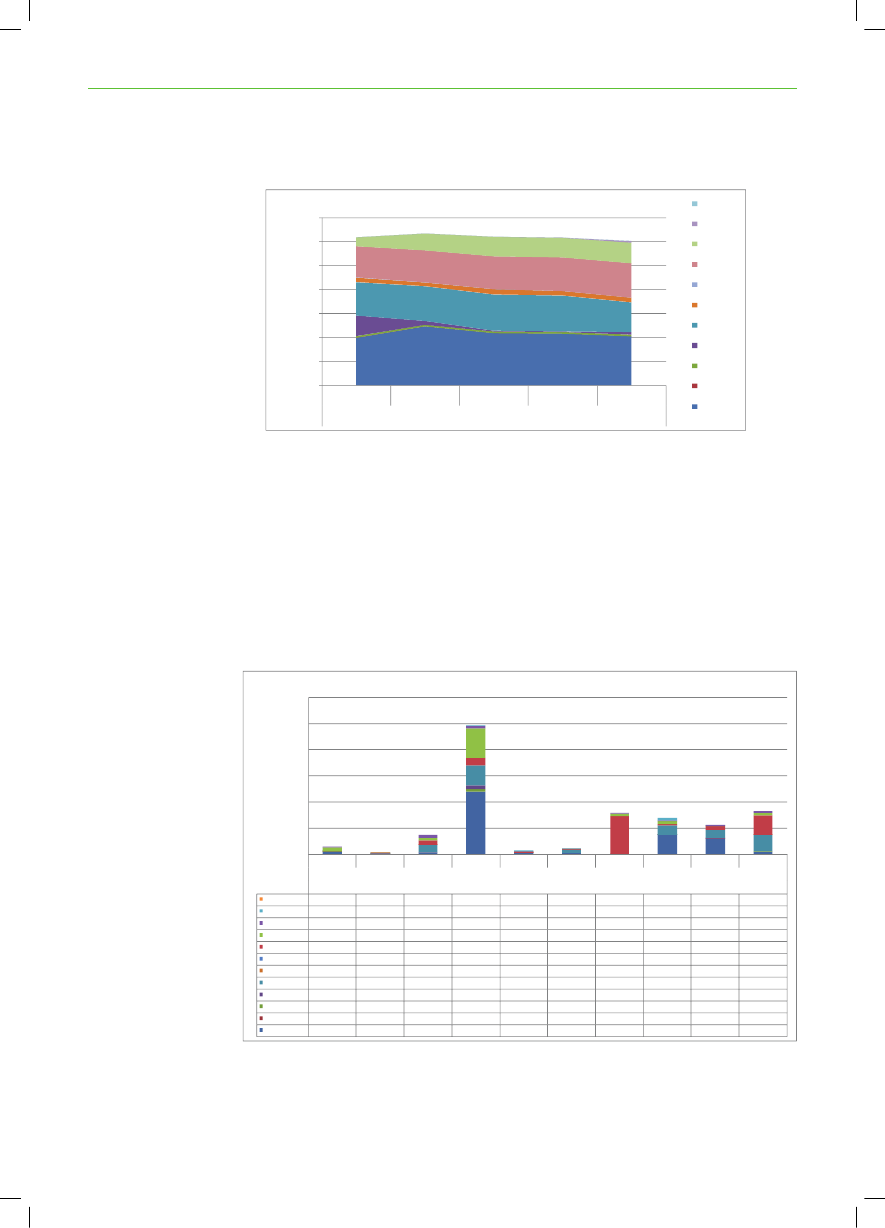

CO2- emissionsOther energyElectricity and district heat

800

TransportStored CO2

600

50% CO2 target

400200

-

-200

Figure 4: CO2emissions from the energy and transport sectors in 1990, 2005 and projections for2030.“Other energy” includes oil, gas and coal used in households, industry and the trade/service sector. Datais only included for North East Germany and North West Russia.

16

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

The scenarios show that resources and technologies are available to achieve thetargets set out. In the Small-tech scenario, it is foreseen that the gross energyconsumption is reduced by approx. 20 % in 2030 compared to 2005. In the Big-tech scenario, gross energy consumption increases by 13 % compared to 2005.This increase, which is slightly higher than in the 2030 reference projection, ismainly due to increased utilisation of carbon capture and storage technologiesthat are expected to require a considerable expenditure of energy, particularlyfor the capture and transportation of CO2. In the Big-tech scenario, compliancewith the CO2-reduction target is secured by yearly storing almost 150 Mt of CO2underground by 2030.

Phase II: Detailed scenarios for electricity and district heatingIn Phase II of the project detailed scenario analyses have been developed forthe power and district heating sectors in the region. Besides showing a pathwaytowards lower CO2-emissions and an improved security of supply, the scenariosexplore the benefits of closer cooperation around the Baltic Sea on energy policiesand specific projects, as well as shedding light on the value of establishing newinterconnectors in the region.The scenarios in phase II are analysed using the energy market optimisationmodel Balmorel. Data used in the scenarios are publicly available data. Themodel optimises the system as a whole, but the electricity and heating systemare modelled for the individual countries, making it possible to examine thedifferences between regional targets, and targets for the individual countries.The scope of the analyses in phase II is to:examine how the electricity and district heating systems may developin order to comply with medium and long-term policy objectives givendifferent developments in the framework conditions;show the value of establishing new electric interconnectors;assess the costs and benefits of a concerted off-shore wind power planningand interconnection at Kriegers Flak.In Phase II the geographical scope of the analyses has been expanded to comprisethe whole f Germany, whereas Phase I only included the North Eastern part ofGermany bordering the Baltic Sea.

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

17

1.3 The Baseline scenarioThe frameworkScenarios toward 2030A Baseline scenario has been developed to show how the electricity sector inthe Baltic Sea region may develop leading up to 2030. The baseline scenarioseeks to combine measures from the Small- and Big-tech scenarios elaboratedin the project’s Phase I. Three alternative scenarios have been developed. Thesescenarios are described in Chapter 4.TheBaseline scenariodiffers from the traditional passive business as usualprojection by showing a way forward to actually achieving the EU targets ofreducing CO2-emissions by 20 % in 2020 and increasing the share of renewableenergy to 20 %. Moreover, a project target of a 50 % reduction of CO2comparedto 1990 is applied for 2030. Compared to 2005 this corresponds to a reduction ofCO2-emissions by 38 %. The means to achieve the policy targets in the Baselinescenario are to a large extent determined by the modelling tool based on a leastcost analyses of supply side measures.CO2targets 2005 2030 (Mt)700600500400300200100

CO2-emission targets

2005

2010

2015

2020

2025

2030

Figure 5: Modelled targets for reducing CO2emissions from the electricity and district heating sectorsin the period 2005-2030 for the Baltic Sea Region. In 2020 CO2emissions from the electricity generatorsin the region are to be reduced by 21 % compared to 2005 as this is the general requirement for thecompanies encompassed by the EU CO2emissions trading system. In 2030, the target is to comply witha 50 % reduction of CO2compared to 1990 - compared to 2005 the target corresponds to a reduction by38 %. A linear development is assumed between 2005 and 2020 and between 2020 and 2030

EU renewableenergy targets

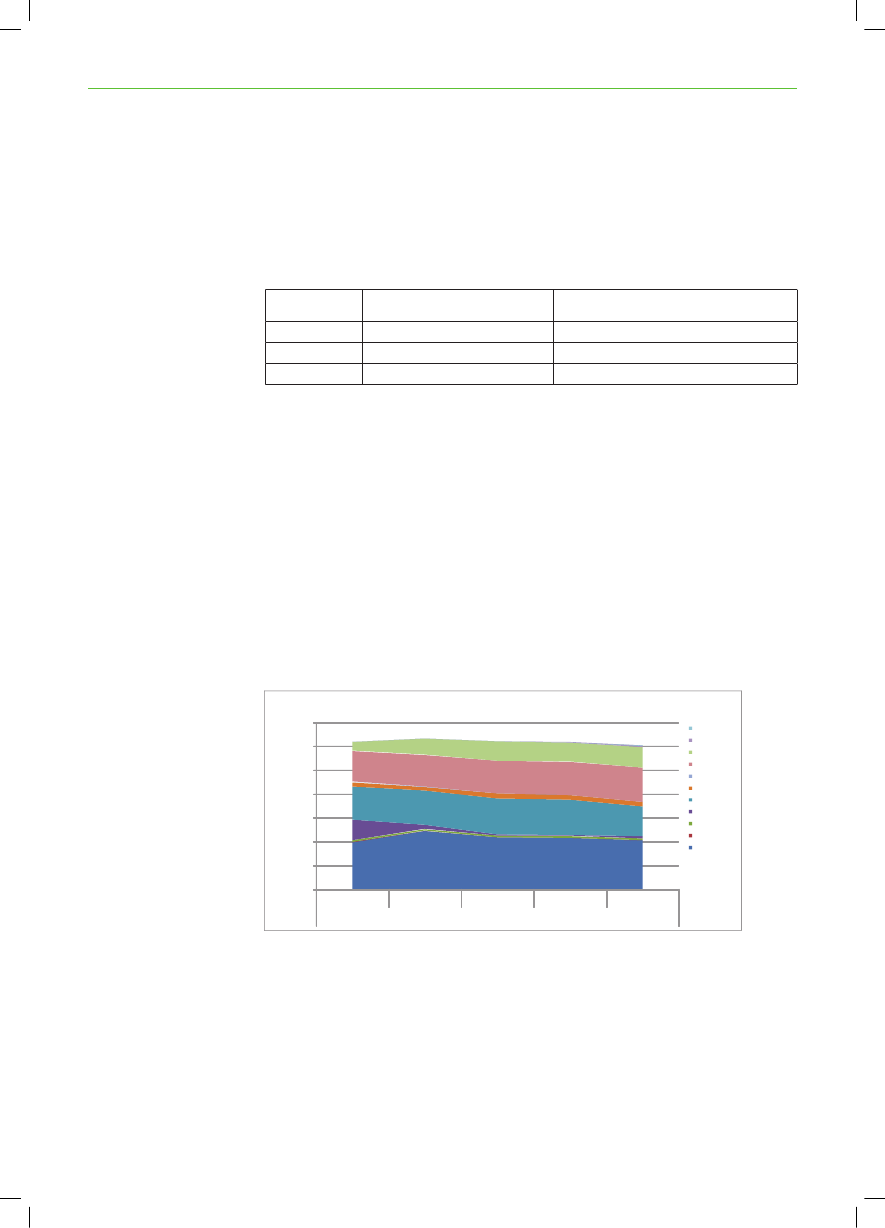

The targets for renewable energy are set in accordance with the renewableenergy directive endorsed at the EU Council Summit in December 2008. Therenewable energy directive provides a target for the share of RE of final energyin each member state, but not a separate target for the electricity sector.The level of renewable energy that will have to be introduced in the electricitysector will, among other things, depend on the economical and technicalopportunities compared to increasing renewables in other sectors such as thetransport sector and the industry. In the present analyses it is chosen to operatewith a target for the electricity sector corresponding to: RE share of electricityin 2005 + 1.5 * required increase in RE in overall final energy demand in thedirective.

18

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

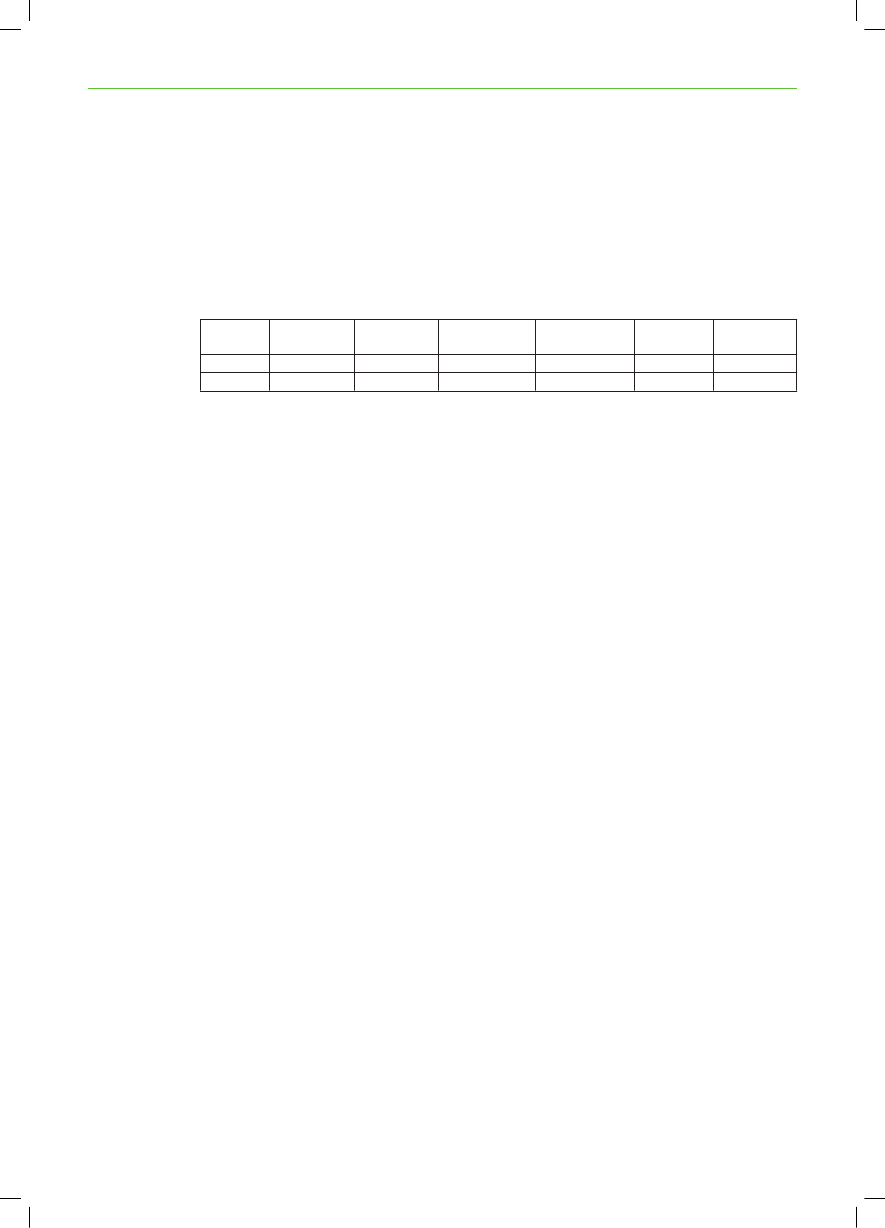

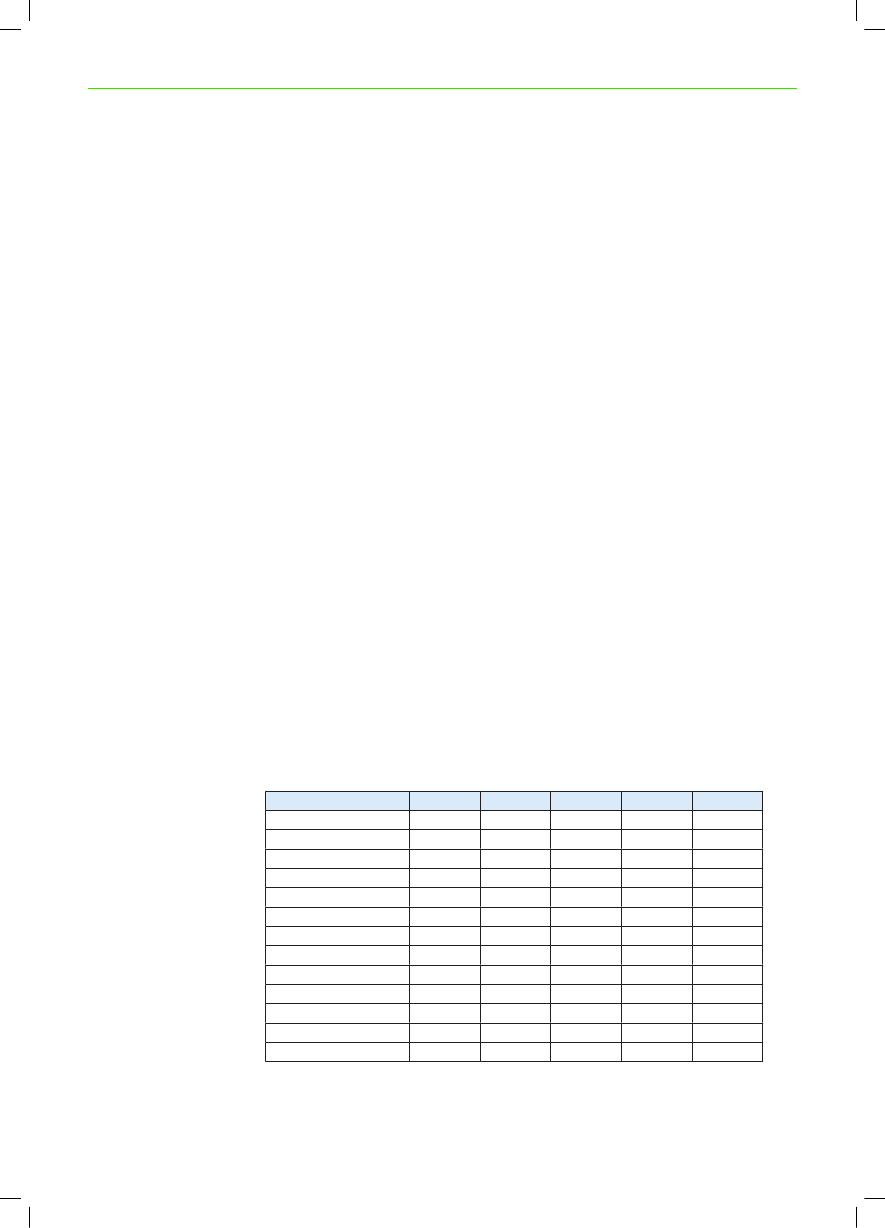

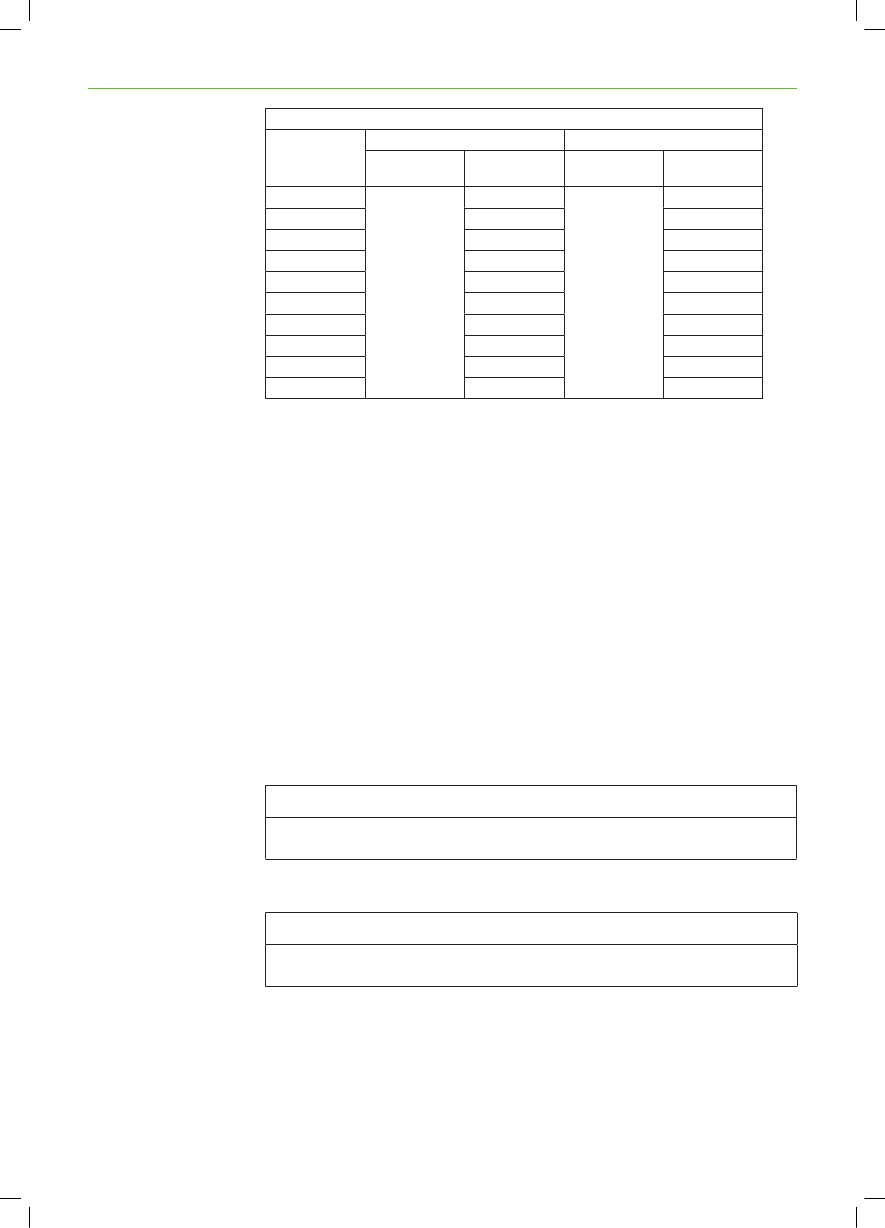

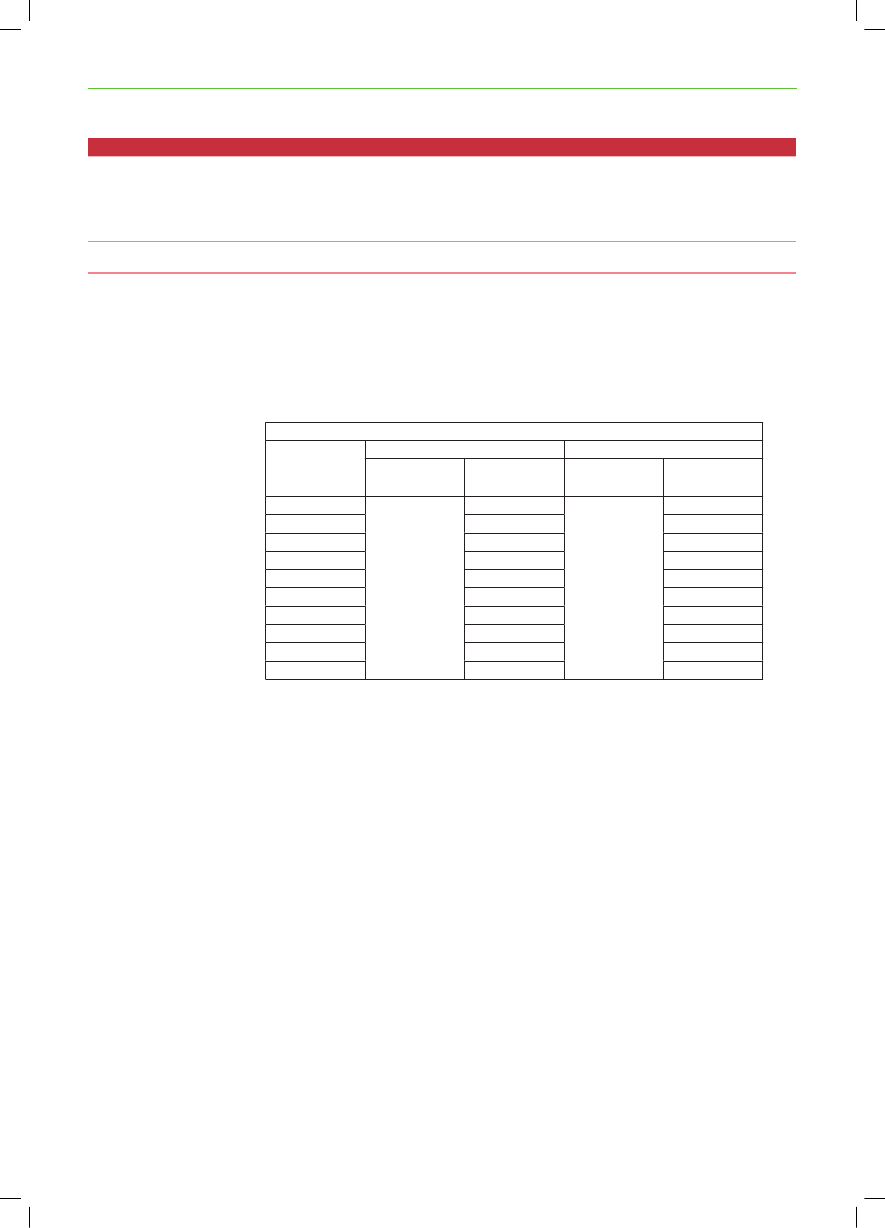

As an example, 28 % of electricity consumed in Denmark in 2005 was suppliedfrom renewable energy. The RE directive requires Denmark to increase its shareof RE in final energy demand by 13 percentage points from 17 % in 2005 to 30% in 2020. Hence, the RE target for the Danish electricity sector is set at 48 %in 2020 (i.e. 28 % + 1.5 * 13 %).For the Baltic Sea Region as a whole renewable energy electricity correspondedto 26 % of total electricity supply in 2005. For 2020 the target for the region is37 % based on the approach outlined above. The targets are shown in Table 1.Russia has no target for RE.Final energy2005 RE share2020 targetIncrease 2005-2020Electricity2005 RE shareExpectedincrease inelectricitysector2020 targetGermany Denmark Estonia Finland Lithuania Latvia Poland Sweden Norway6%18%12%0%11%18%29%17%30%13%0%28%20%48%18%25%7%0%1%11%12%29%38%10%0%27%14%41%15%23%8%0%4%12%16%35%42%7%0%48%11%59%7%15%8%0%3%12%15%40%49%9%0%54%14%68%60%60%0%0%100%0%100%NWRussia3%0%0%0%19%NANAREGION14%25%11%0%26%15%37%

Table 1: Renewable energy targets. No renewable energy target has been included for North WestRussia

Fuel prices

The development in prices of fossil fuels is based on the latest forecast fromInternational Energy Agency’s (IEA) World Energy Outlook 2008 (WEO-2008).According to this projection the price of crude oil will increase from an expected100 $/bbl in 2010 to 122 $/bbl in 2030. The price of natural gas is expected torise from just above 5 €/GJ in 2010 to slightly over 10 €/GJ in 2010.Phase II of the present study focuses on the least-cost ways of achieving thetargets from a socio economic point of view. Hence, the existing country specificpolicy measures for promoting renewable energy are not considered in thecalculations as they would tend to divert investments in renewable energytechnologies to the countries with the most favourable support scheme, ratherthan the countries with the best renewable energy resources.The model has a data catalogue with a set of new power station technologies thatit can invest in according to the input data. The investment module allows themodel to invest in a range of different technologies including (among others)coal power, gas power (combined cycle gas turbines and gas engines), straw andwood based power plant, power plants with CCS and wind power (on and off-shore). Assumptions regarding technology data are presented in the backgroundreport.Regarding nuclear power, it has been chosen to model the development basedon best available information about the future role of nuclear in the differentcountries in the region as opposed to letting the model make the “optimalinvestments”. The nuclear forecast is made with the intention to form acompromise between the strong views (pro and against) towards nuclear poweramong politicians and other stakeholders in the region. In Sweden for example,

Existingsupport-schemes

Technology data

Nuclear

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

19

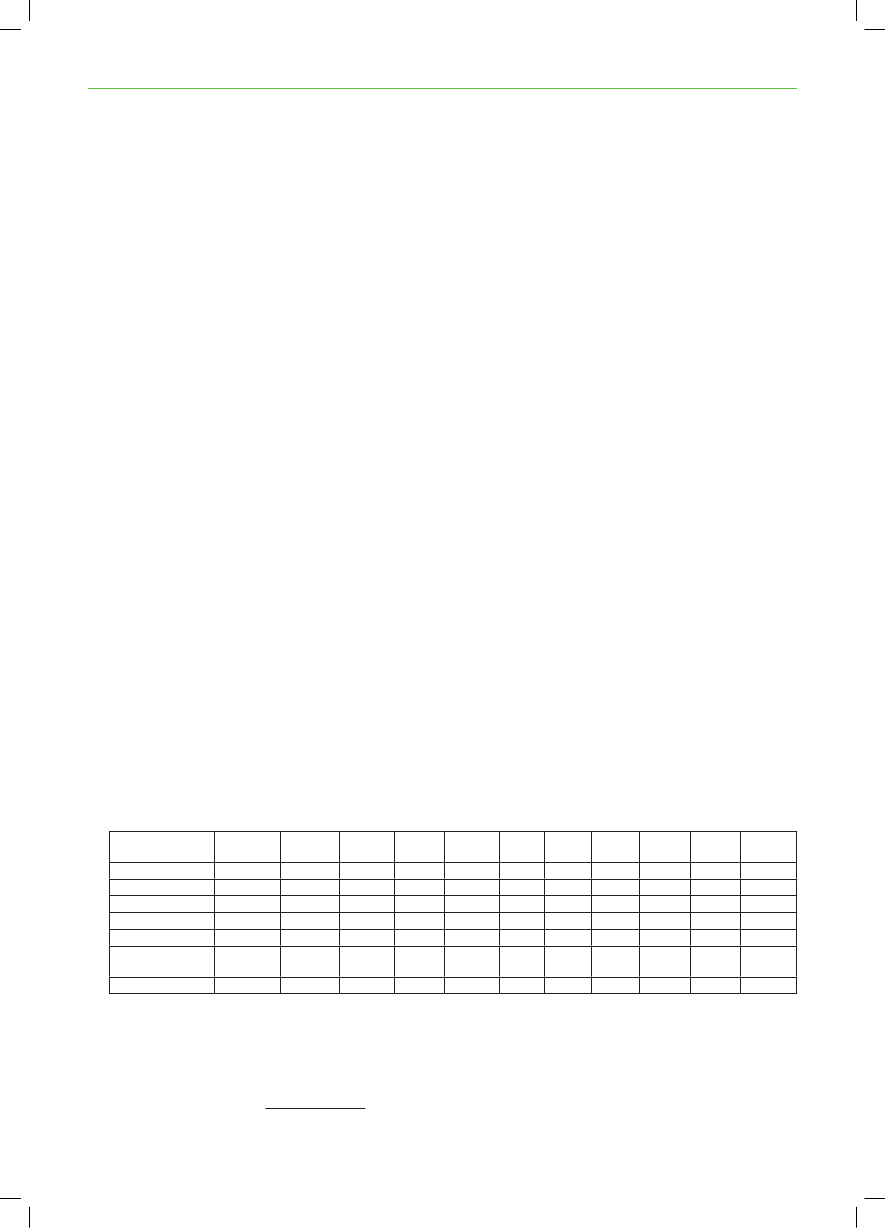

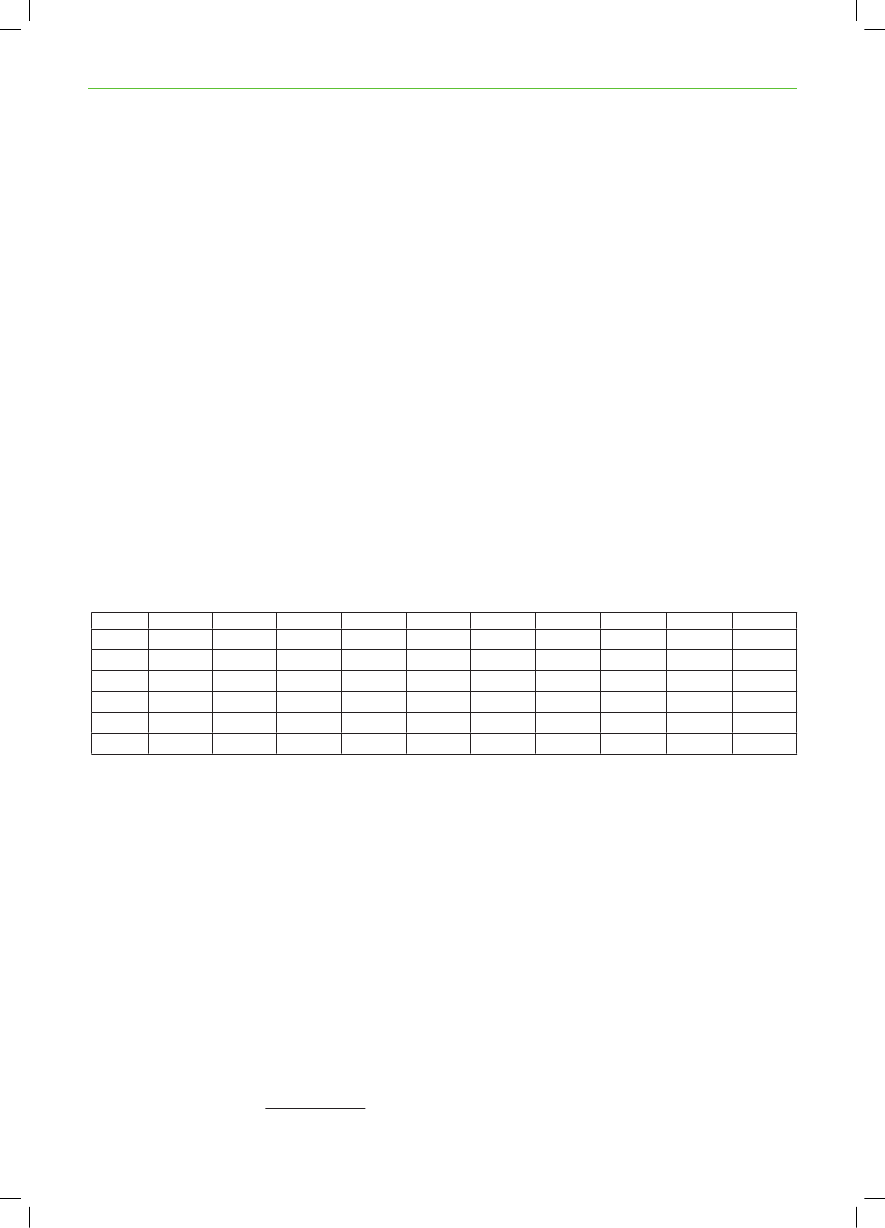

the nuclear capacity is assumed to remain at the existing level whereas a delayedphase-out is anticipated in Germany.MWDenmarkSwedenFinlandNorwayGermany2005-9,3722,656-20,2642010-9,3722,656-20,2642015-9,3724,256-20,2642020-9,3724,256-20,2642025-9,3724,256-17,8702030-9,3724,256-9,256

PolandLithuaniaEstoniaLatviaNW RussiaTotal

-1,200--5,76039,252---5,76038,052

----5,76039,652

-1,500--5,76041,152

2,0891,500--5,76040,847

4,3851,500--5,76034,529

Table 2: Assumed development in nuclear capacity in the Baltic Sea Region. This development is appliedin all scenarios.

With the exception of nuclear power and hydro power the investments in newpower producing units are determined by the model, based on informationabout the technical and economical data for each technology.A number of assumptions on the rate of decommissioning of existing plants areassumed. These assumptions are based on, among other things, the expectedtechnical life time of power plants, and in certain cases information about theconditions of specific power plants.

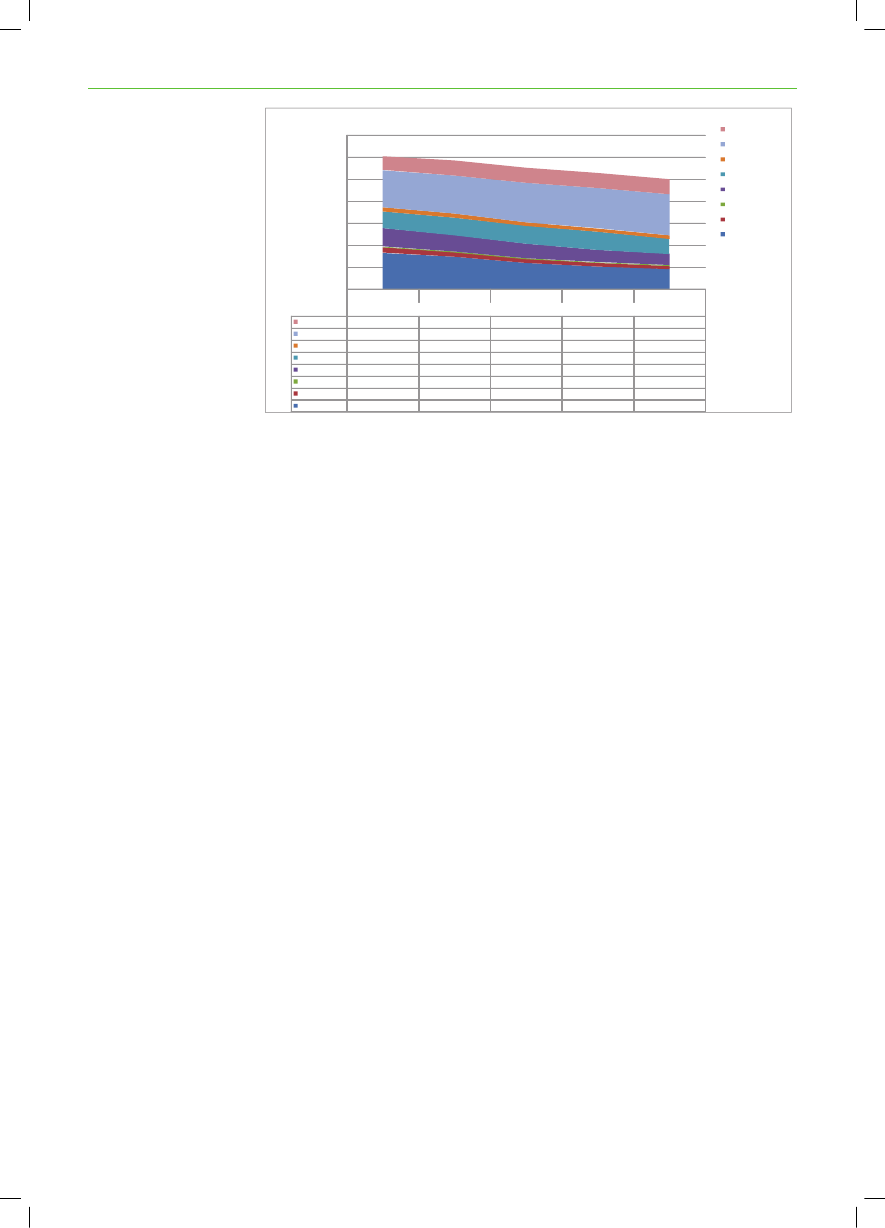

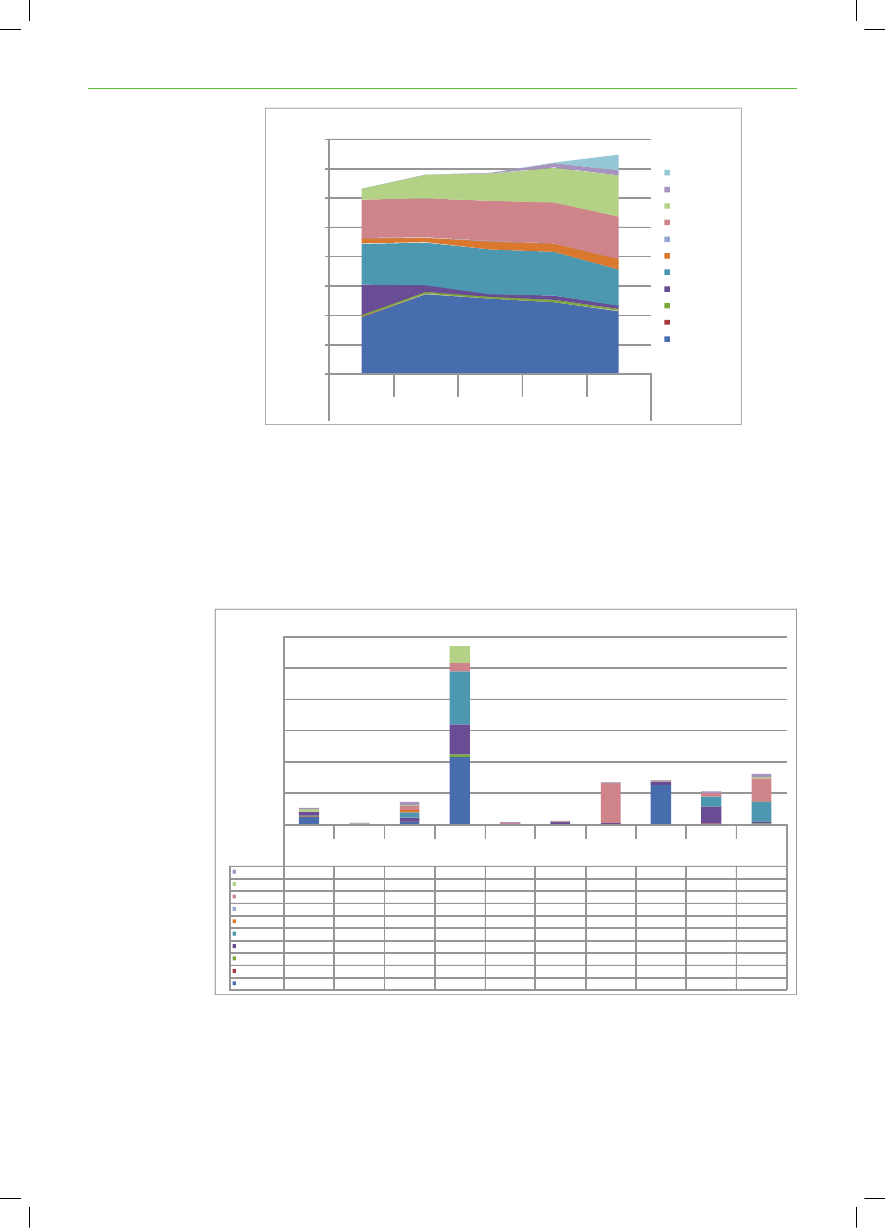

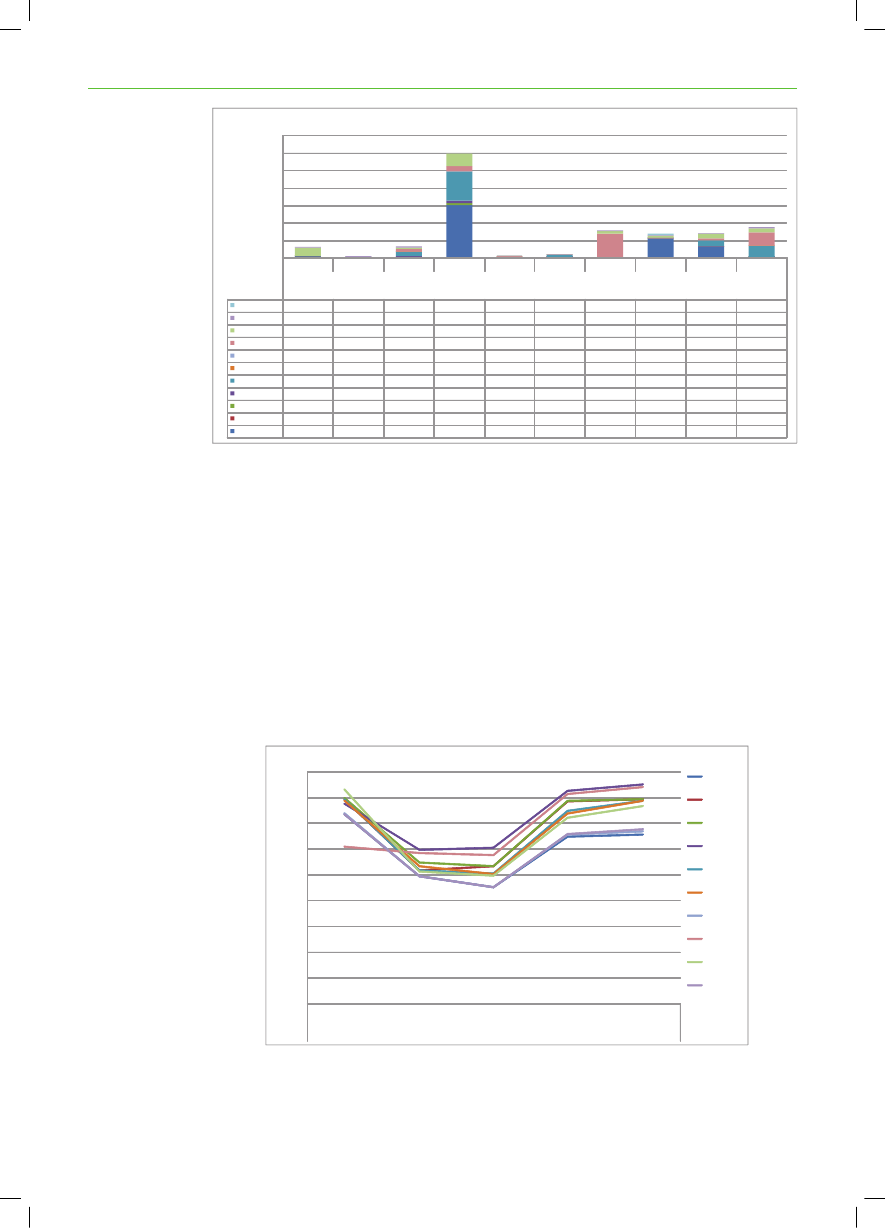

ResultsNew generation capacityFigure 6 shows the development in new generation capacity for the whole region– as determined by the model. Investments in new capacity are only allowedfrom 2015 due to the lead time of new generation facilities.Capacity by fuel450.000400.000350.000300.000250.000New - Coal CCSNew - BiogasNew - WindNew - Bio massNew - Natural gasNew - Coal and ligniteExisting capacity andplanned capacity

MW200.000150.000100.00050.000-201020152020Baseline scenario20252030

Figure 6: Total electrical capacity (MW) for Baseline scenario distributed on new and existing capacities

20Wind and coal

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

In the Baseline scenario it appears that the economically most attractivetechnologies are wind power and coal power. The coal fired power plants thatthe model chooses to invest in use new highly efficient technology with electricefficiencies of 48 % when running in condensing mode. The coal fired powerplants are primarily established in the beginning of the period while the windpower plants are established more evenly during the whole period from 2015 to2030.The model also invests in new biogas based generation capacity, new biomassfired capacity and coal fired power plants with CCS. The majority of theseinvestments are made in the period 2020-2030. Though the level of investmentsis fairly small compared to the investments in e.g. wind power, it indicates thatthese technologies are competitive.

Biogas and biomass

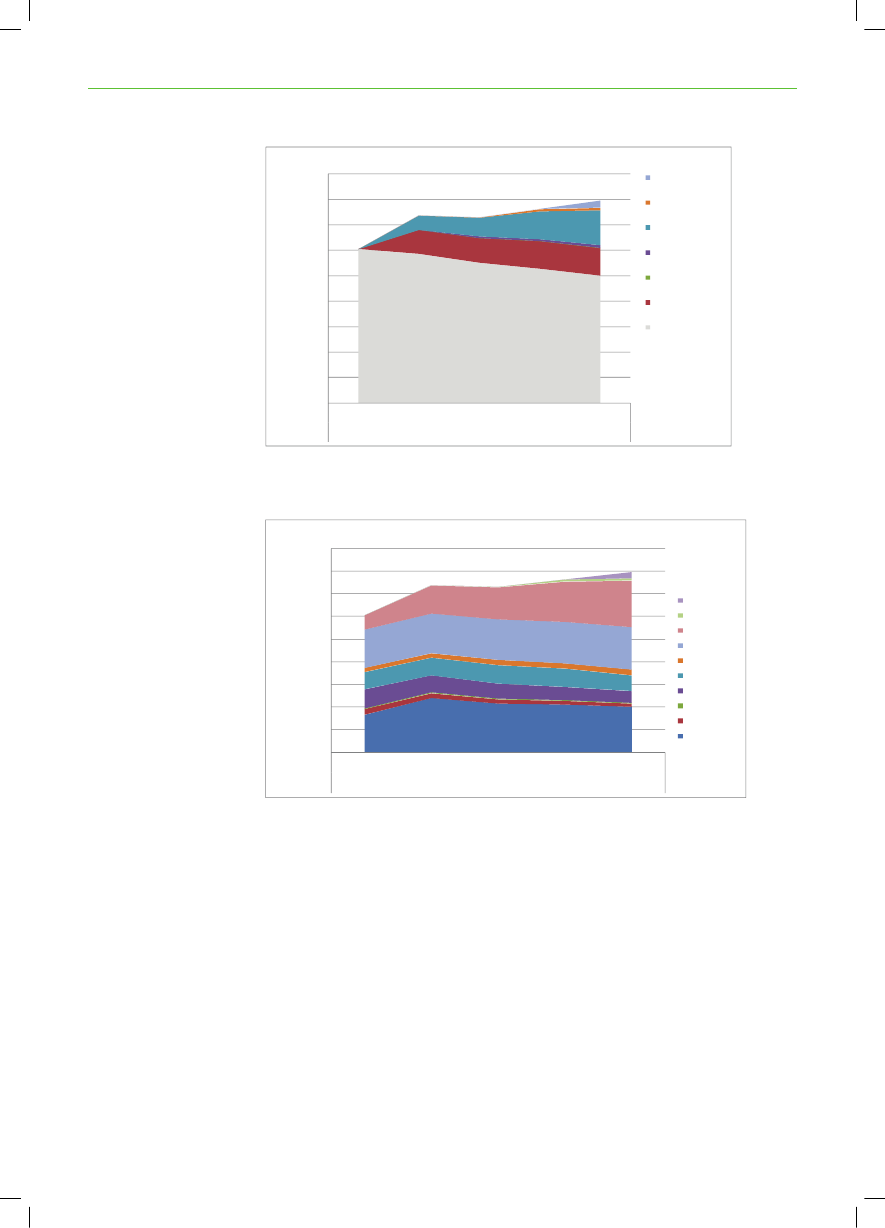

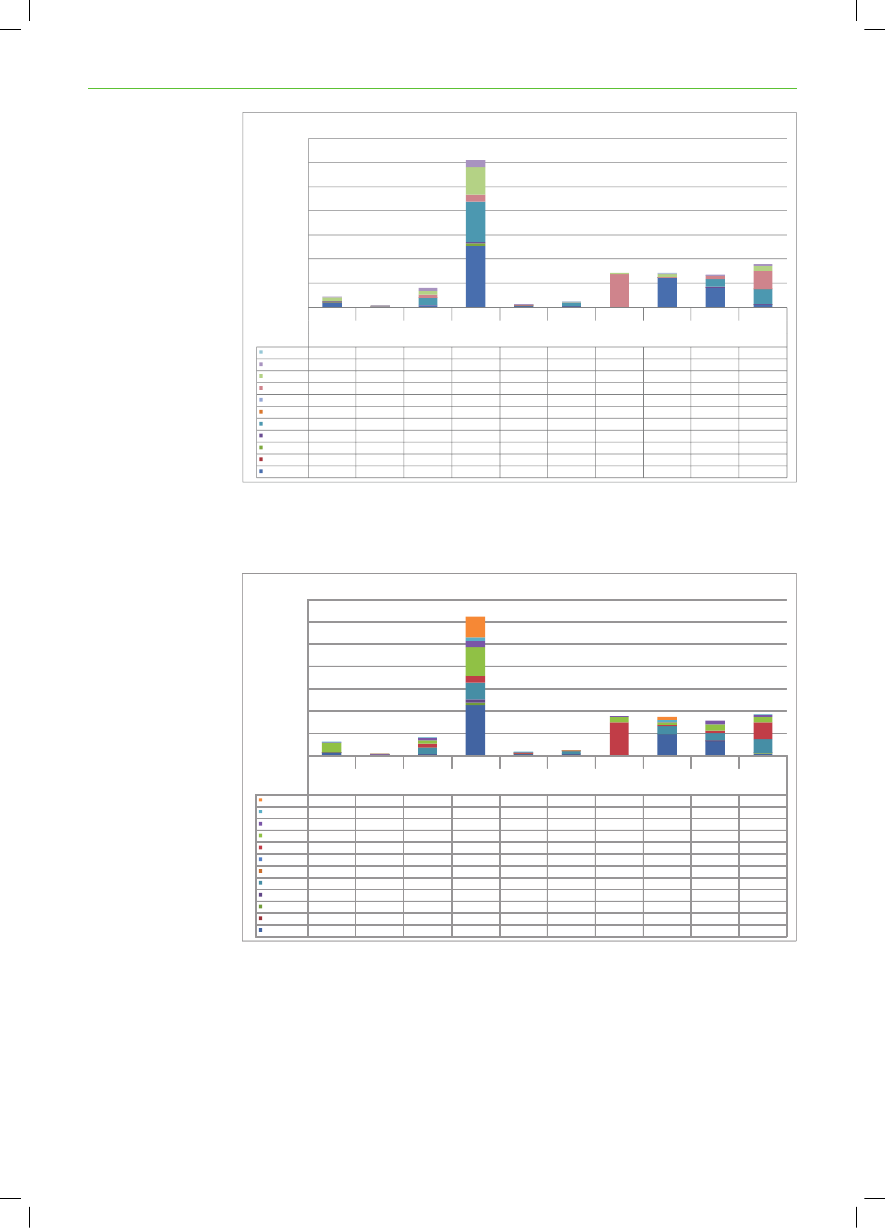

FuelsElectricity generation by fuel for all countries is shown in Figure 7 .Electricity generationElectricity genera on1.6001.4001.2001.000Coal CCSBiogasWindWaterOilshaleBiomassNuclearNatural gasWasteOilCoal and lignite

TWh

hW800T600400200-201020152020Baseline scenario20252030

Figure 7: Total electricity generation (TWh) by fuel for Baseline scenario.

Natural gasconsumption decreases

The utilisation of natural gas decreases very significantly between 2010 and 2015as a result of the investments in wind power and new efficient coal power plants.This development is particularly profound in Russia where approximately halfof the electricity is produced from natural gas in the 2010 simulation. It shouldbe mentioned that such a significant decrease in the demand for natural gas islikely to result in a drop in the regional natural gas price, which will to someextent moderate the overall impact. This correlation has not been quantified inthe model.The role of wind power is gradually increased over the period and by 2030 windpower is the largest source of electricity next to coal power and hydro. Biomassand biogas only gain some significance by the end of the period.

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

21

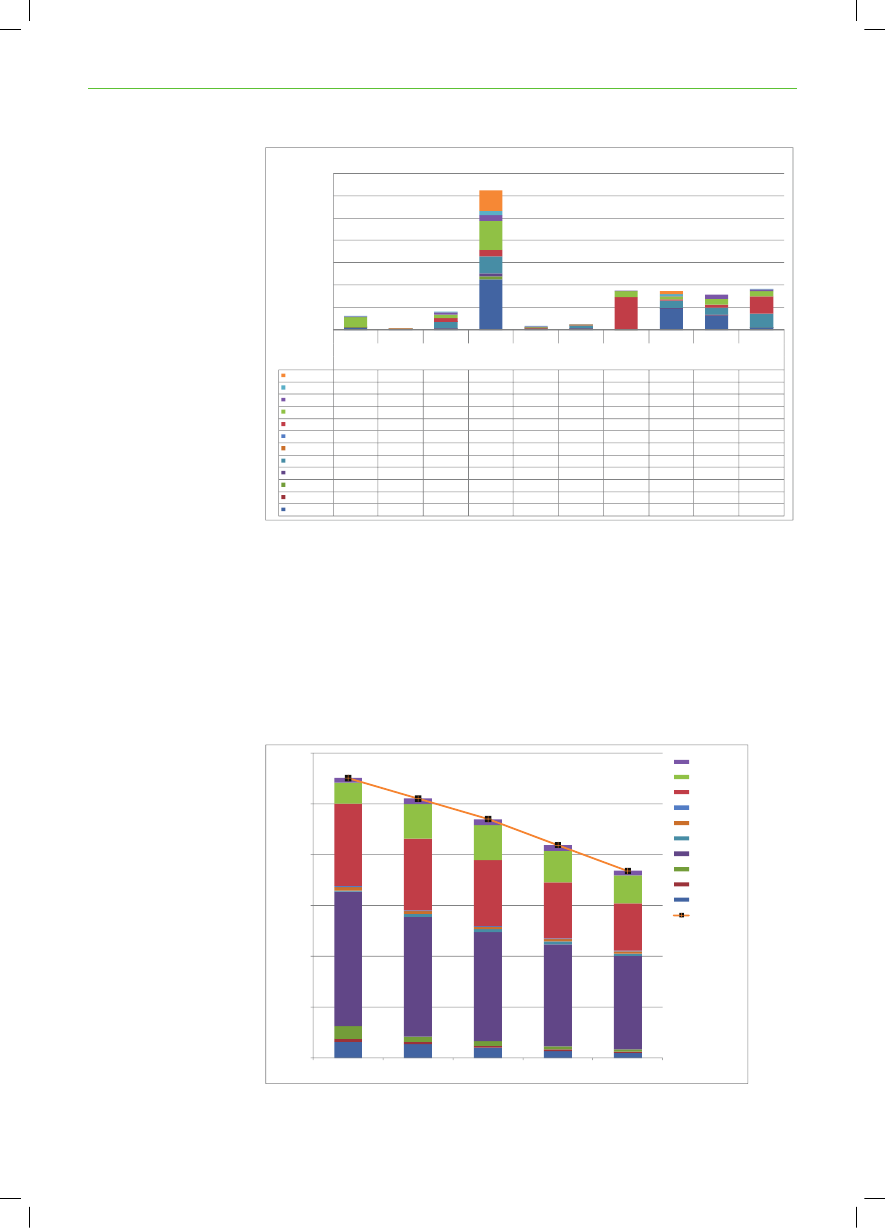

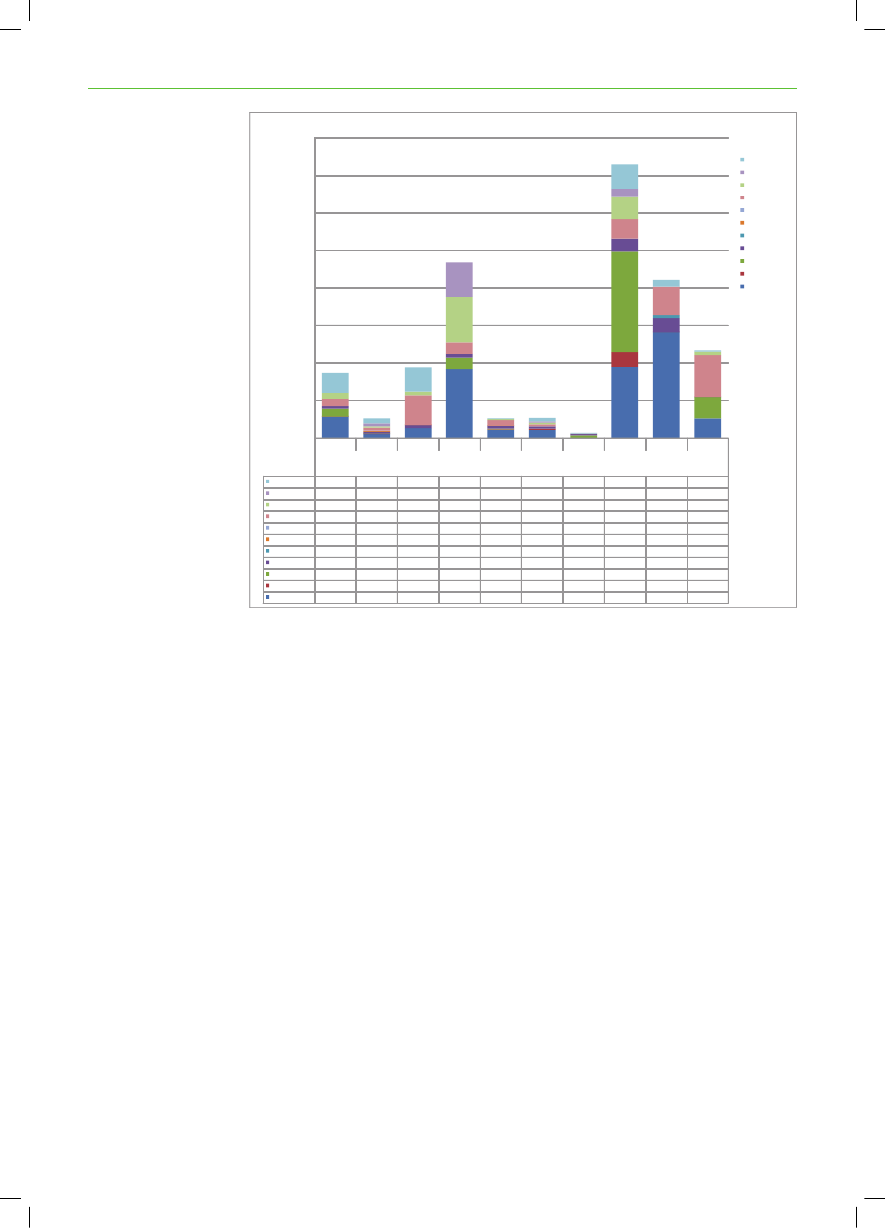

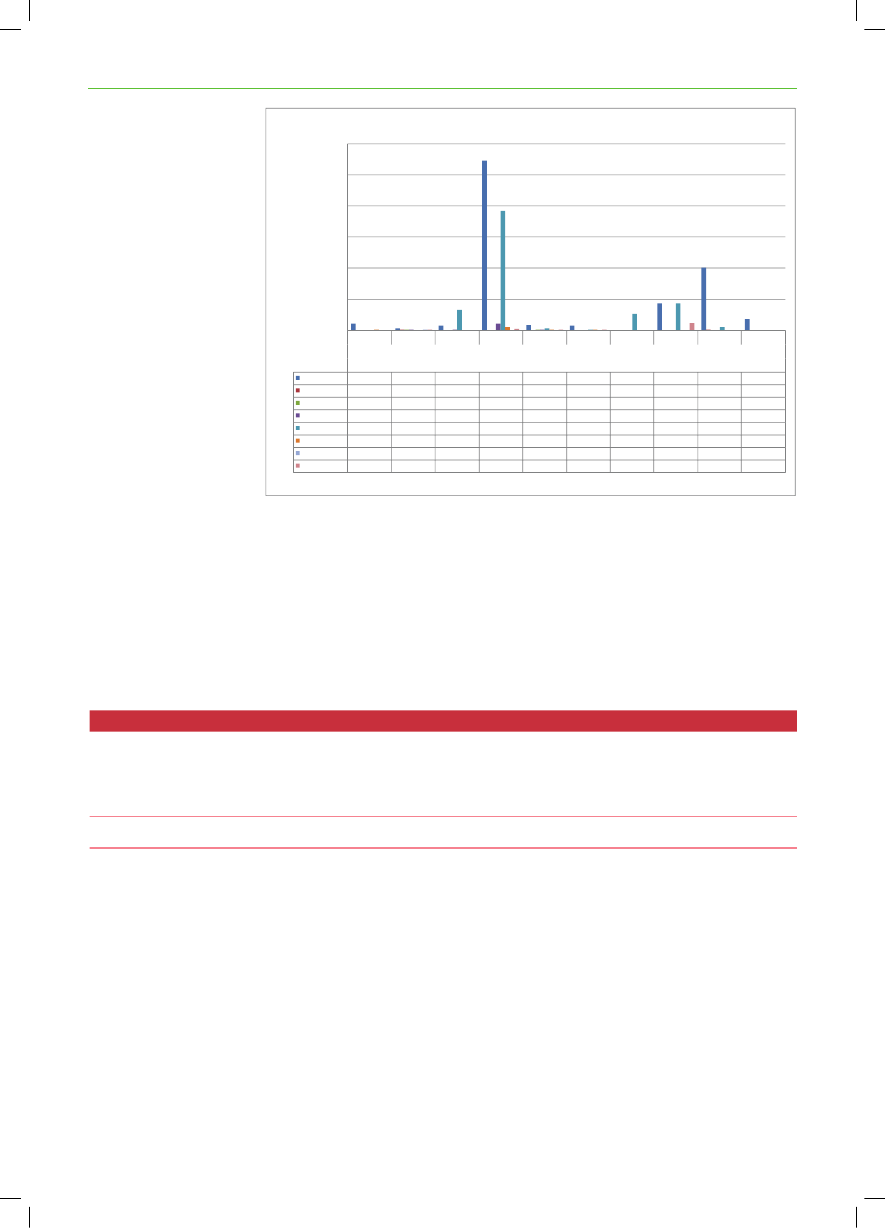

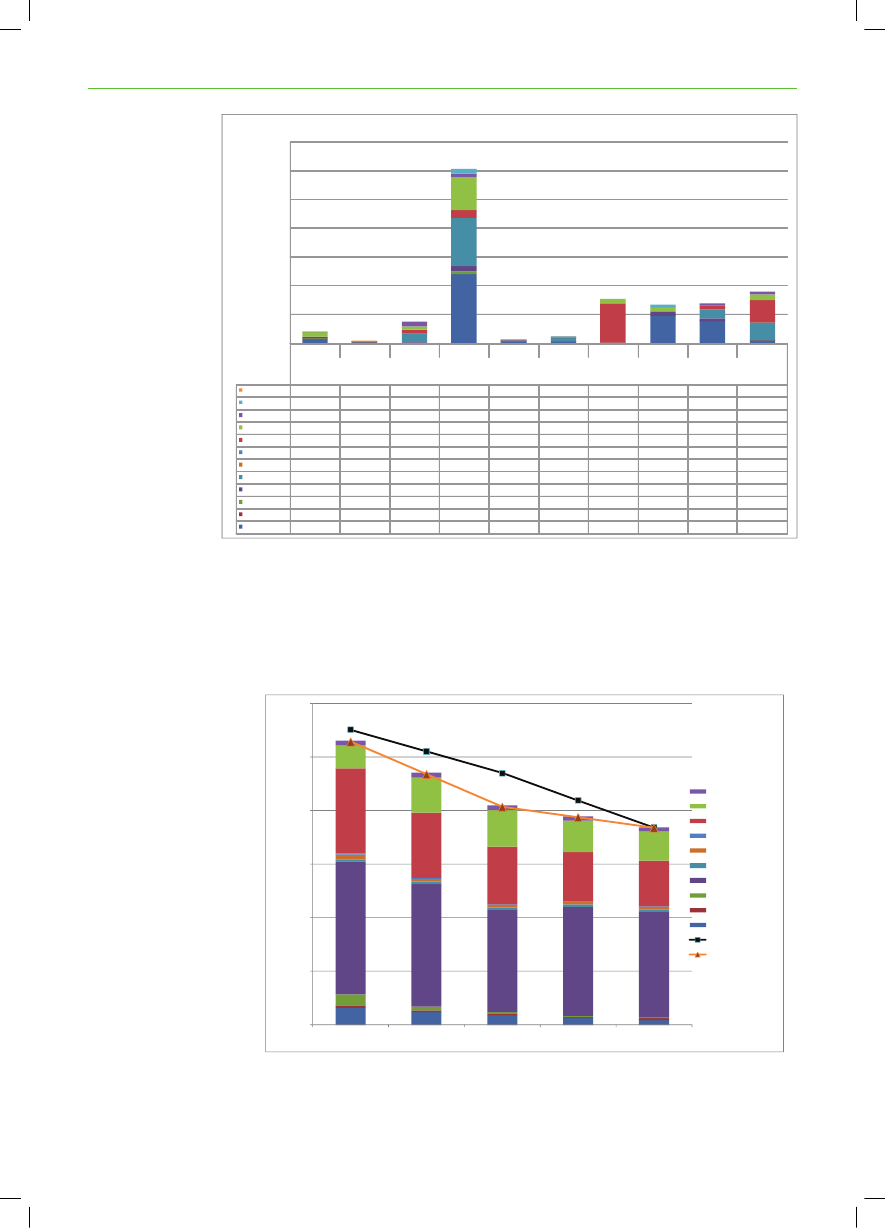

Figure 8 gives an overview of the electricity generation (TWh) for each countryin 2030 grouped byvfuel in the Baseline scenario.Electricity generationby countryElectricity genera onby country700600500400TWh

300200100-

DENMARK

ESTONIA

FINLAND

GERMANY

LATVIA

LITHUANIA2030

NORWAY

POLAND

RUSSIA

SWEDEN

Baseline scenarioC CSoal CBiogasBiomassWindWaterShalePeatNuclearNatural gasWasteOilC and ligniteoal120103100522760002917613111005950120103610065103146301224421112111616921826129301223110010251471492134172812192475

Figure 8: Electricity generation (TWh) for each country in 2030 grouped by fuel for Baseline scenario.

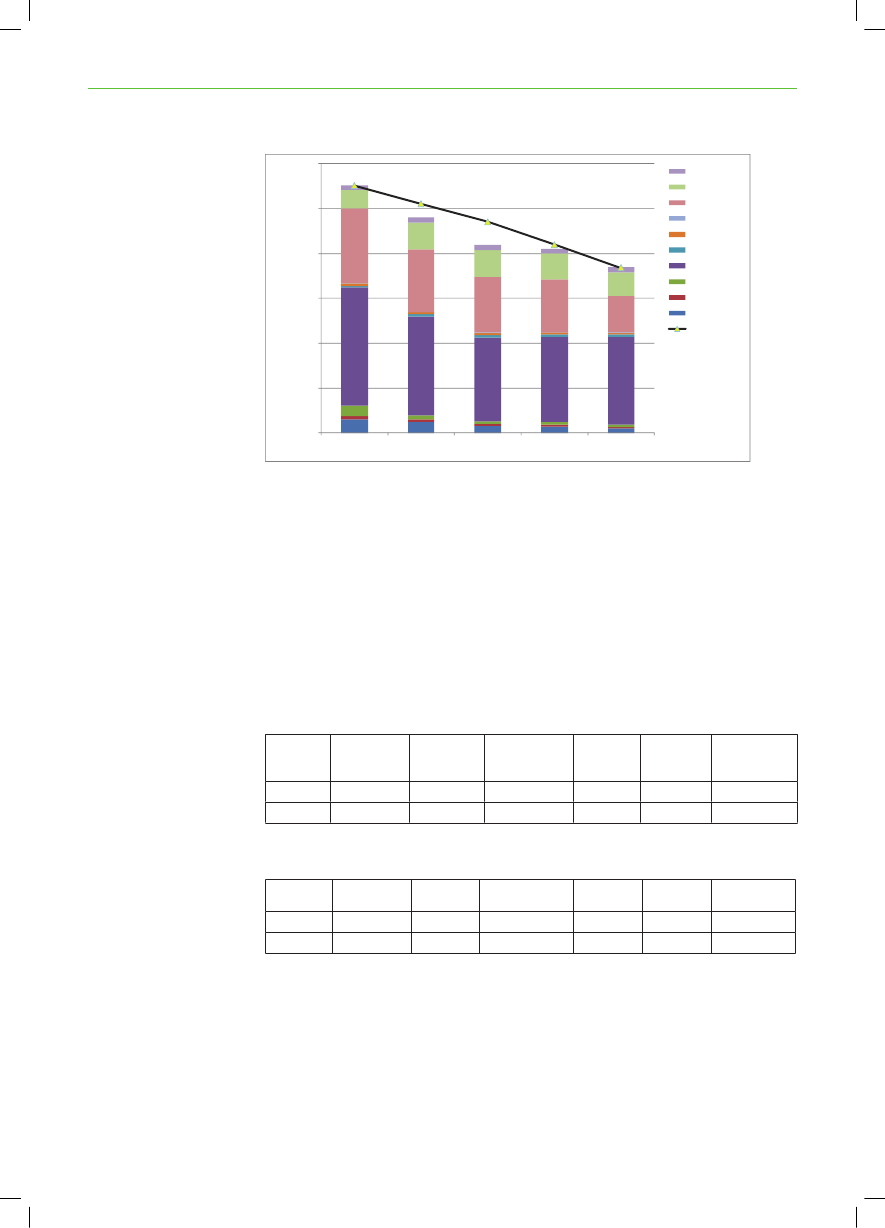

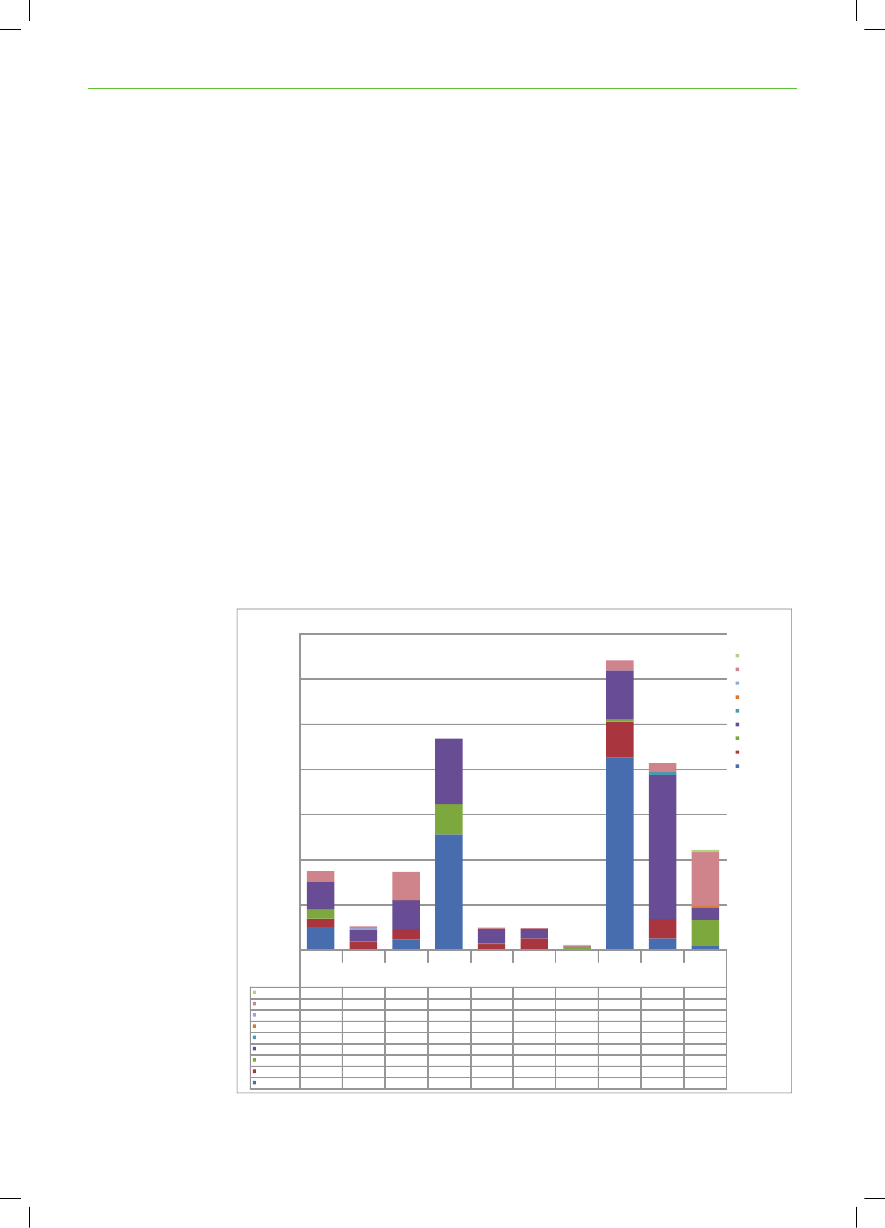

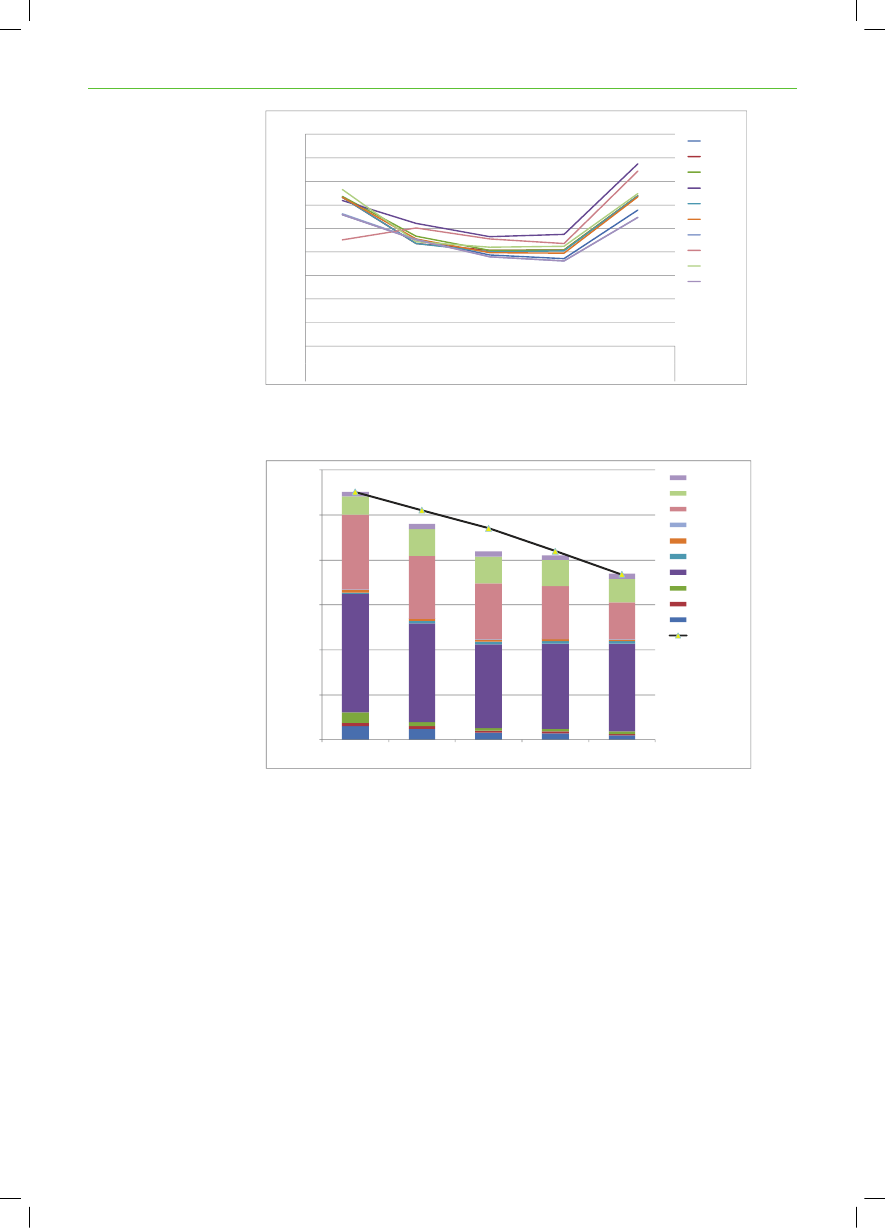

Figure 9 illustrates the development in CO2-emissions in the Baseline scenariocountry by country. The emissions are capped by the regional target indicatedby the yellow line.The simulations show that the marginal cost of abating CO2is approx. 7 € perton in 2020 and approx. 60 € per ton in 2030 for the electricity and heatingsector.Mt

CO2-emissions

600

S DEWE NRUS IASPOLAND

500

NORWAYLITHUANIALATVIA

400

GERMANYFINLANDE TONIAS

300

DENMARKRegional target

200

100

-20102015202020252030

Figure 9: Development in CO2-emissions (Mt) for the electricity and district heating sector by country inthe Baseline scenario

22

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

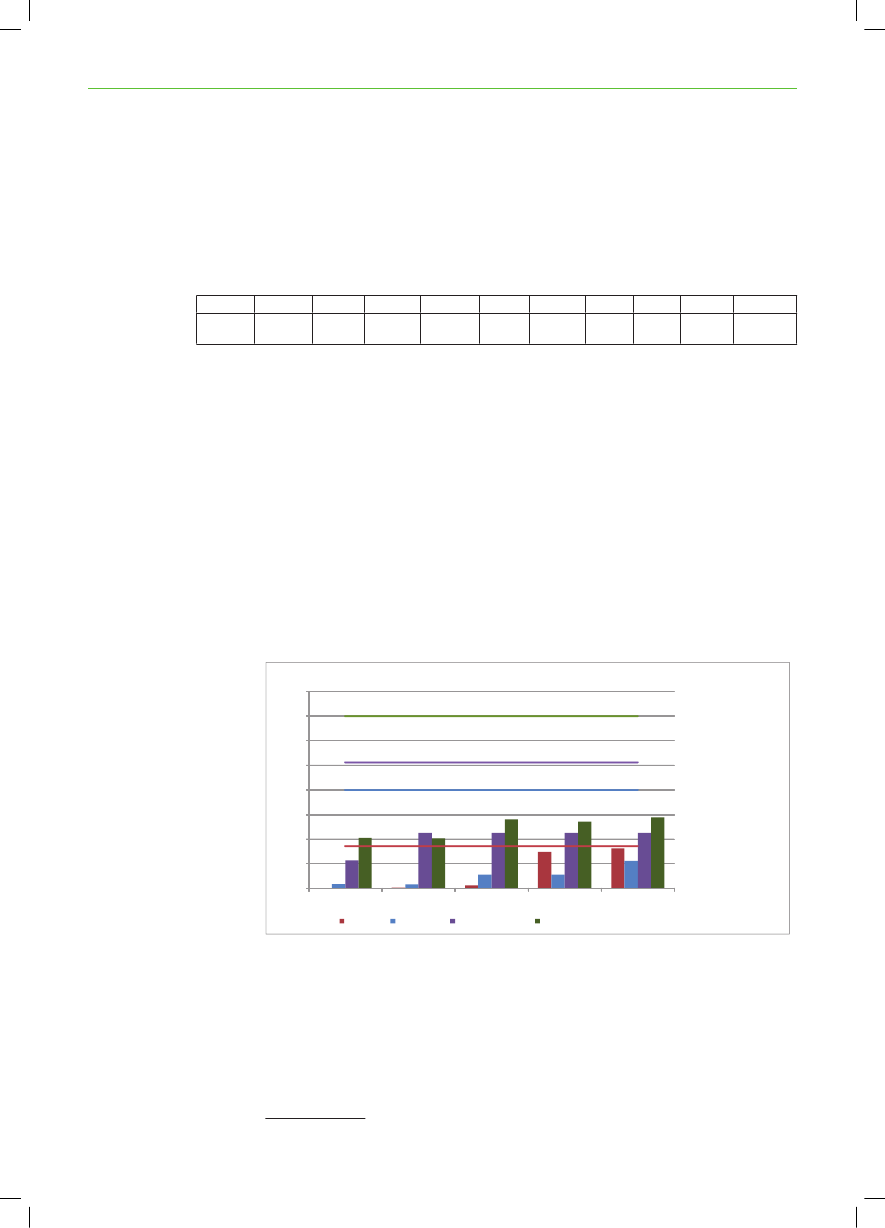

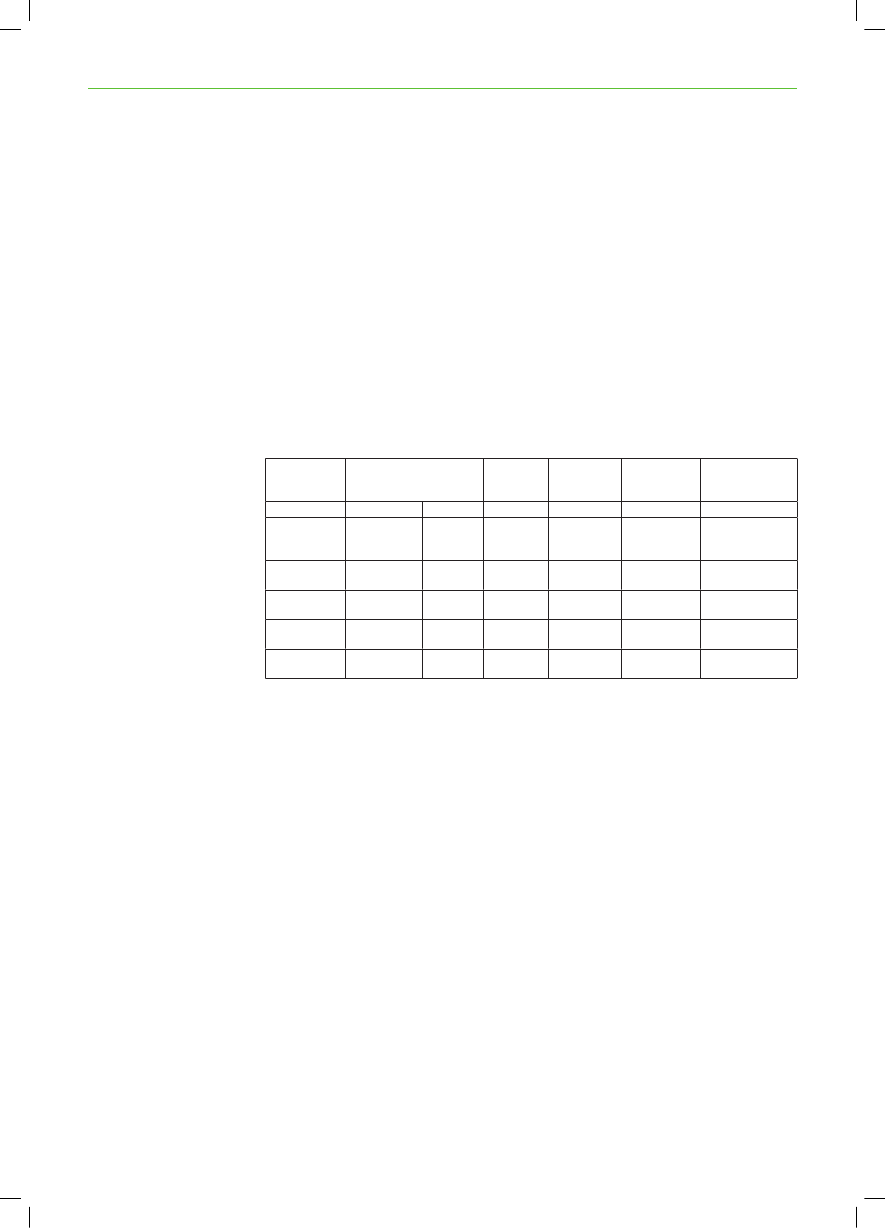

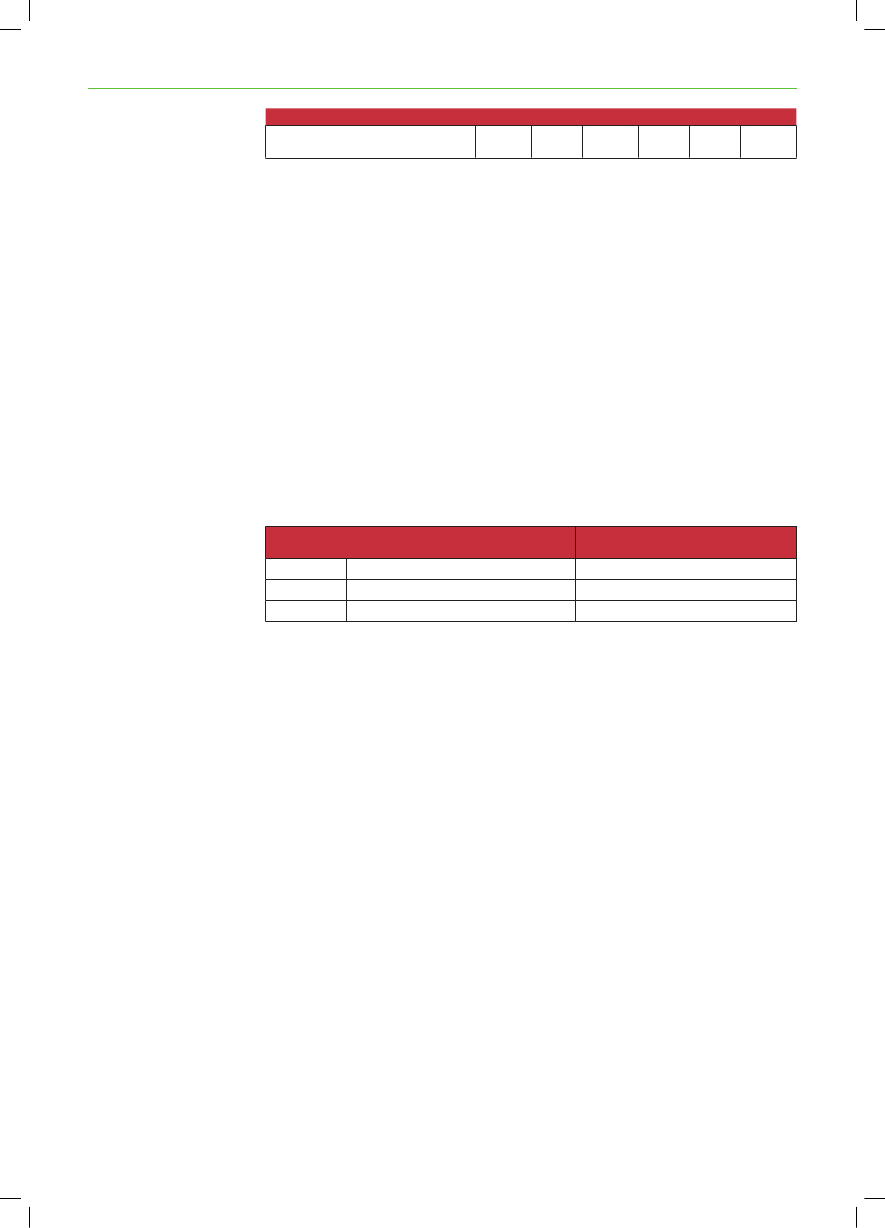

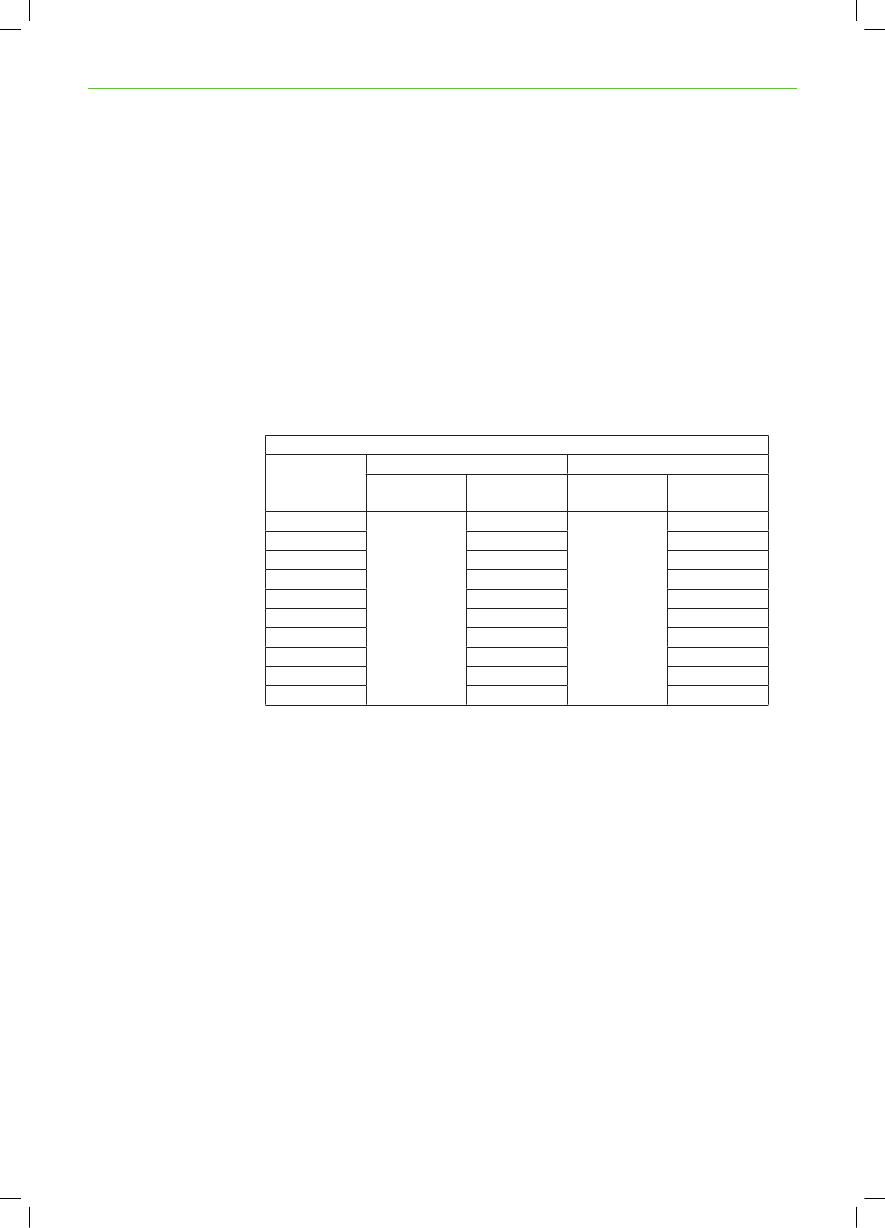

Renewable targetsAll countries succeed in complying with their national target, but the marginalcost of fulfilling the targets differs between the countries. In Russia there isno price of renewable energy because no national renewable energy target isassumed. In Norway the price of renewable energy is zero, because the expecteddevelopment of new hydro power leads to compliance with the national renewableenergy target. Lithuania, Latvia and Germany have the highest marginal costs ofexpanding renewable energy electricity generation in 2020, see Table 3.CountryBaselinescenarioDenmark16Estonia16Finland29Germany30Latvia31Lithuania Norway Poland Sweden NW Russia31-2416-

Table 3: Shadow prices for RE targets in 2020 in the different scenarios (EUR/MWhel)

The difference in compliance costs reflects the costs of new renewable energygeneration in each of the countries compared to the value of new renewableenergy electricity in the electricity markets.Bioenergy resourcesTo determine the potential and costs of expanding renewable energy generation,wind, biomass and hydro power resources have been mapped for each countryin the region4. Assumptions about potentials are available in the backgroundreport. Figure 10 shows the utilisation of biomass resources (columns) in thebaseline scenario (2010 to 2030) in the whole region compared to the long termpotentials (lines).By 2030, when CO2emissions have been reduced by 50 % compared to 1990,a very significant potential remains for further increasing the use biomass andwaste for electricity and heat generation.Utilization of biomass resources1.6001.4001.2001.000J800PLong term municipal wastepotentialLong term biowaste potentialLong term potential for forestryresidues and energy crops

PJ600400200-2010Biogas2015Biowaste2020Municipal waste20252030

Long term biogas potential

Forestry residuesand energy crops

Figure 10: Utilisation of biomass resources (columns) in the baseline scenario compared to the longterm bioenergy potentials available for power generation and district heating (lines). It has beenassumed that only 60 % of the total bioenergy resource in the region will be available for the power anddistrict heating sector, leaving 40 % to be used in industries, households and the transport sector. Themunicipal waste resource also includes the non-renewable energy fraction of the waste.

Of the different bioenergy fractions considered, biogas is the most attractive touse with an utilisation factor close to 100 % in 2030. The reason for this is thatthe utilisation of biogas for energy production leads to supplementary reduction4 Data on bioenergy potential is lacking for North West Russia.

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

23

of fugitive emissions (methane and nitrous-oxide) in the agricultural sector –related to the alternative use of the manure. Hence, a negative CO2emissionfactor (-43 kg/GJ) is used for biogas in the model making it a very attractiveCO2-reduction measure.

Conclusions from the Baseline scenarioThe Baseline scenario shows the following conclusions:The targets for reducing CO2and increasing the share of renewables can bemet given the resources and technologies available. The scenarios do notassume any technological leaps.Wind power is an economically viable technology that contributesconsiderable to reaching the renewable energy targets and to reducing CO2-emissions.The region has a number of old power plants with low efficiency. In theshort run, the model chooses to replace these old power plants with newcoal-fired power plants or combined heat and power plants with very highefficiency. This strategy could be reasonable to meet the CO2-targets in theshort run, but it may not be the most viable in the long run with more strictCO2-targets.New biomass-fired power plants, biogas plants and coal fired power plantswith CCS are close to being competitive with new conventional coal-firedpower plants. These technologies could be part of the region’s focus on newenergy technologies with a strong global potential. Further use of biomassin existing coal-fired power plants should be investigated further.Natural gas based power generation generally becomes uncompetitivegiven the assumed development in fossil fuel price and the policy targetsincluded. This issue deserves further investigation, specifically theconnection between regional gas demand and gas prices.Even in 2030, when CO2emissions are reduced by 50 % compared to 1990,there is a significant unexploited bioenergy and wind potential, signifyingthat further reductions of CO2emissions are possible.

24

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

1.4 Three alternative policy scenariosIn addition to the Baseline scenario, three scenario variations have beeninvestigated. These variations differ in the way policy targets are complied withand whether common solutions or national solutions are put in play.The scenario variations comprise:a scenario withregional targetsfor increasing the share of renewable energyinstead of national targetsanImproved efficiency scenariowhere electricity consumption is expectedto be reduced considerably compared to the baseline projectiona30%@COP15 scenarioshowing a situation where CO2-emissions from thepower and district heating sectors are reduced by an additional 10 percentagepoints in 2020The latter scenario variation reflects a situation where an ambitious internationalagreement is obtained at the Copenhagen Climate summit in December 2009committing the EU Member States to cut their overall CO2-emissions by 30 %in 2020.

Regional renewable energy target scenarioRelocation of windIn theRegional RE Target scenariothe model still chooses to invest mainlyin wind and coal power, but a large share of the investments in wind poweris relocated from Germany, Sweden and Finland to Denmark and particularlyNorway, where wind conditions are assumed to be somewhat better. Transferringthe national targets to a regional target thus means a better utilisation of theinvestments in wind power.The simulations show that the benefit of this relocation of investments is approx.5 billion € in net present value. However, this figure should be interpreted withcaution, because the country specific estimates of renewable energy potentialsand costs are associated with a significant degree of uncertainty, particularlyin the long-term. Moreover, it should be stressed, that the total generation ofrenewable energy in the Baltic Sea Region is approx. 8 TWh lower in the regionalrenewable energy scenario compared to the Baseline scenario. This may appearsurprising since the renewable target is the same in the two scenarios. Thereason for this is that, due to the expected development of new hydro powerplants, Norway over-complies in the Baseline scenario. In the scenario with aregional renewable target Norway’s over-compliance contributes to achieve theregional renewable target.In the situa on with a common RE target the cost of increasing renewable energy be-comes the same in all countries in the region, 19 € per MWh of renewable energyelectricity in 2020.The EU Directive on renewable energy, endorsed by the European Parliament inRE directive opens upfor regional cooperation December 2008, is built on national targets. However, Member States may agreeon the statistical transfer of specified amounts of renewable energy between

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

25

themselves and they may cooperate on any type of joint project relating to theproduction of renewable energy. Finally, Member States have the opportunityto join or coordinate their national support schemes in order to help achievetheir targets.Case: Kriegers FlakIn addition to the overall scenarios a case analysis has been made to illustrate thecosts and benefits of a concerted planning for wind power plants in the shallowwaters of Kriegers Flak in the Baltic Sea. Germany, Sweden and Denmark areall planning to build off-shore wind farms at Kriegers Flak (400, 600 and 600MW respectively).The case explores the consequences of a developing a common integrated off-shore grid, which could also serve as link between the Nordic and Germanelectricity markets. The area and a possible common international connectionare sketched in Figure 11.

Figure 11: Location and sketched connection of Kriegers Flak. The thinner dashed lines indicate theexisting connections between Denmark and Germany (Kontek) and Sweden and Germany (BalticCable). Source: Energinet.dk

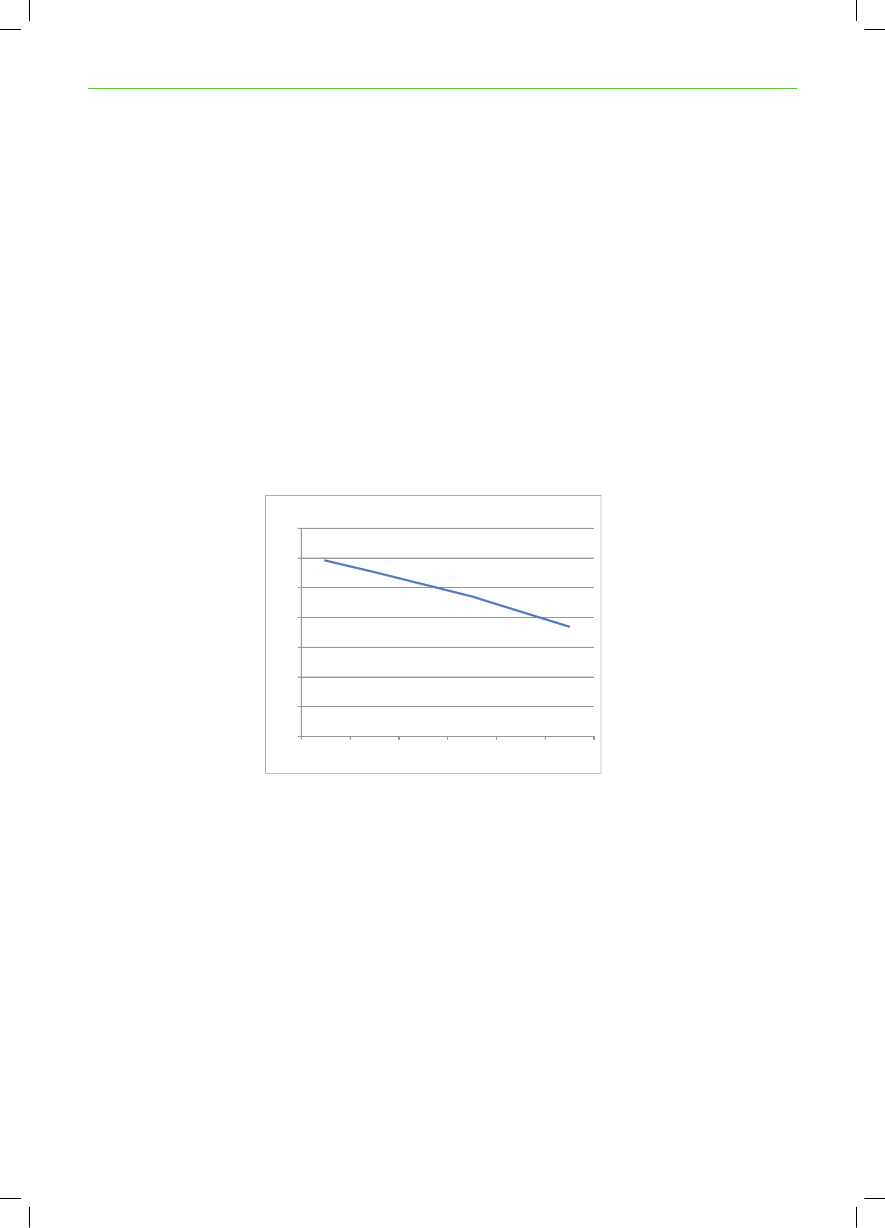

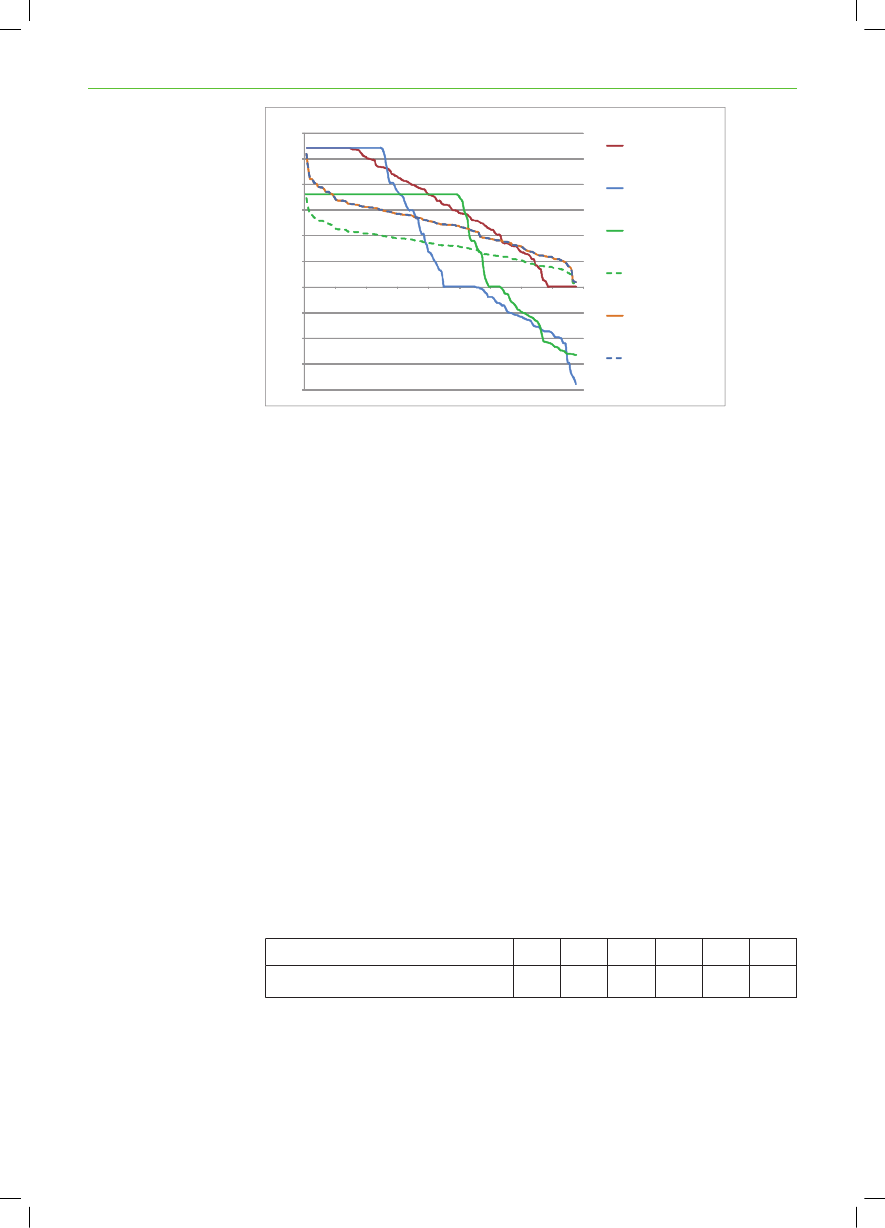

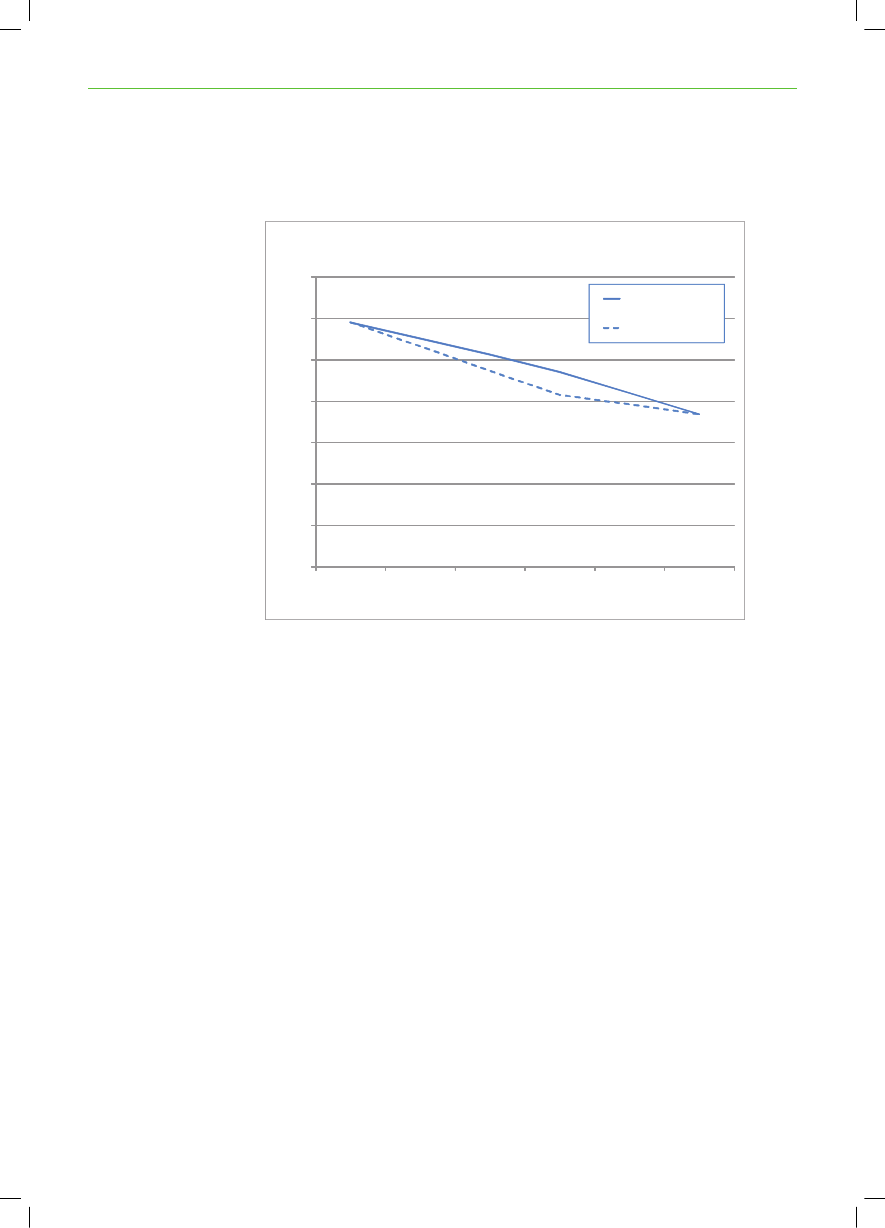

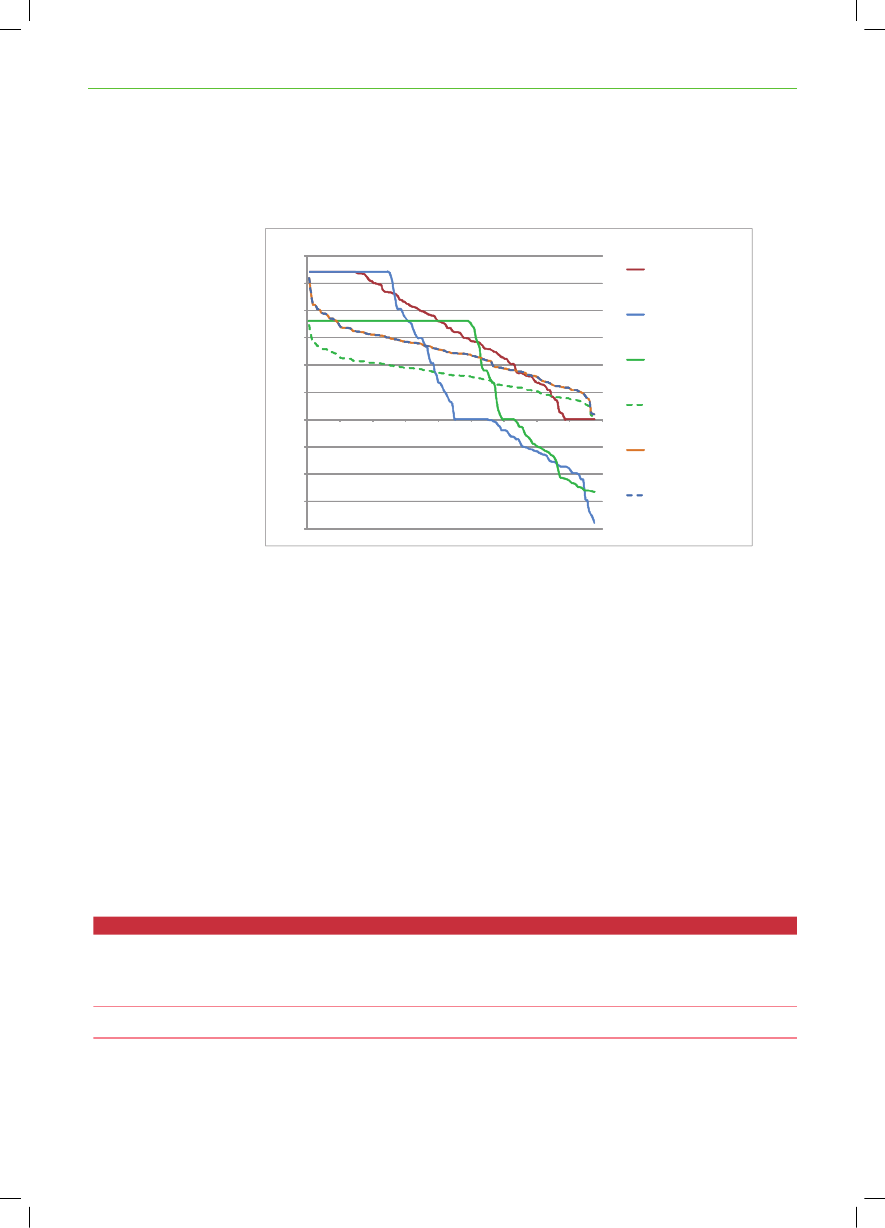

An integrated off-shore wind grid could serve a twofold purpose by connectingthe wind farms to the transmission grid at shore, as well as by linking theelectricity markets in the region. Kriegers Flak could serve as a pilot project foran integrated offshore grid.Transmission of powerat Kriegers FlakFigure 12 shows a duration curve of the transmission between the off-shore windfarms in Kriegers Flak and their respective countries in the Baseline situationwithout a common international connection (dotted lines) and a situation withcommon interconnection (full lines). In the first situation the cables are onlyused to transmit power from the wind farms to land. In the second case, the off-shore grid is also used as a mean to transport electricity to and from the threecountries. This leads to a significant higher utilisation of the cables.

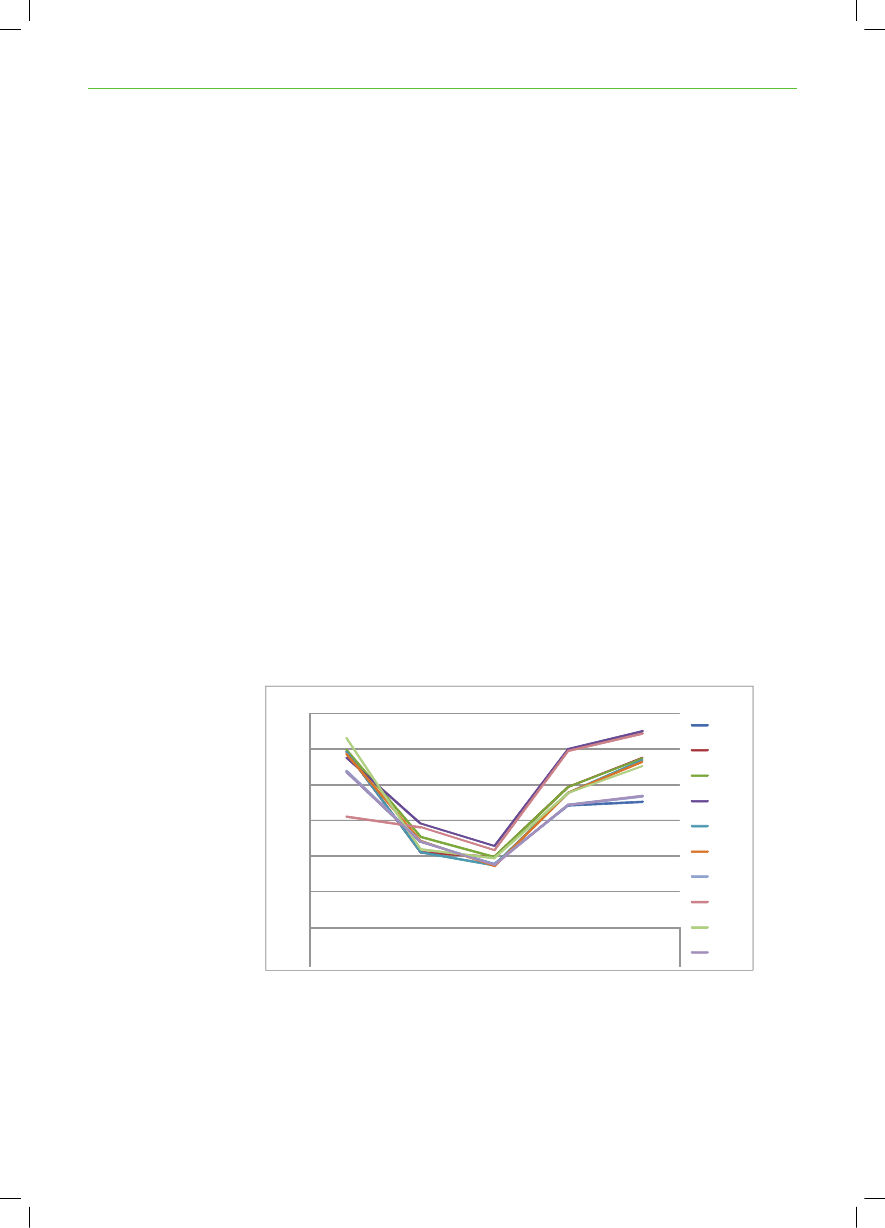

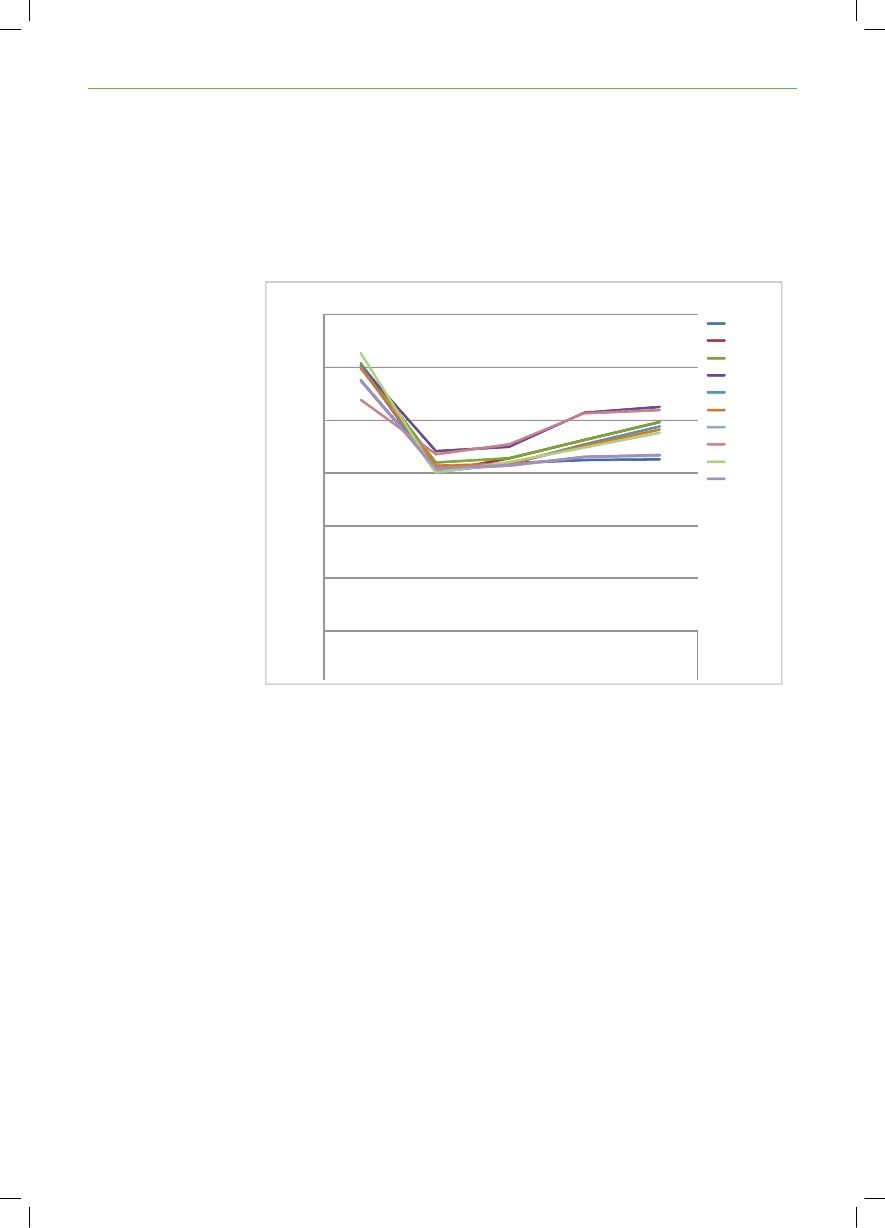

26600

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOSDuration curve for transmission at Krieger'sFlakKriegersFlak Sce. : Krieger -Denmark

500

400

KriegersFlak Sce. : Krieger- Sweden

300

200

KriegersFlak Sce. : Krieger -Germany

MW

W100M

Baseline: Krieger - Germany--1.0002.0003.0004.0005.0006.0007.0008.0009.000

-100

Baseline: Krieger - Denmark

-200

-300

Baseline: Krieger - Sweden

-400

Timestep

Figure 12: Duration curves showing the utilisation of the connections to Kriegers Flak in the BaselineScenario with individual on-shore connection and in the situation with a common interconnection atKriegers Flak.

The common interconnection at Kriegers Flak compared to a situation with nocommon interconnection shows a benefit a Net Present Value of €17 million.This figure does not include the possible higher capital cost associated with thecommon solution.The above calculation assumes only 400 MW of transmission capacity betweenGermany and Kriegers Flak. This is sufficient to connect the 400 MW of expectedwind power capacity at the German part of Kriegers Flak; however in connectionwith an integrated offshore grid it may appear more economic to establish astronger connection to Germany, particularly considering that the connectionsfrom Kriegers Flak to Denmark and Sweden are 600 MW each.

Improved efficiency scenarioElectricity savingsIn the “Improved efficiency scenario” electricity consumption is expected to bereduced considerably compared to the Baseline projection. This is a result ofstringent policies to make consumers use electricity in a more rational manner.In 2030 the general electricity consumption is approximately 20 % below theBaseline level. The same relative level of electricity savings is assumed to takeplace in all countries across the region.All countriesSavings in general electricity consumptionrelative to baseline2005020102%20157%202010 %202515 %203020 %

Reduced electricitydemand for heating

In addition to the general effort to reduce electricity consumption, a specificfocus is put on reducing electricity demand for conventional electric heating- through improved insulation of buildings and by converting to other forms ofheating with lower marginal CO2-emissions, such as electric heat pumps, districtheating, solar heating and boilers fuelled by biomass or natural gas.

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

27

Particularly in Norway, Sweden and Finland, electricity is a very importantsource of heating. Today’s high consumption of electricity in these countriesshould be seen in relation to the history of the energy systems, particularlythe access to cheap hydro power and base-load nuclear power. However, asthe electricity markets have been opened, and considering that the electricitymay alternatively be exported to neighbouring countries where the marginalgeneration comes from thermal power plants, using electricity for direct heatingbecomes expensive and unsustainable.CountryFinlandNorwaySwedenElectricity demand for heating2005, approx.9 TWh30 TWh21 TWhShare of total final electricity demand in200511%27%16%

Table 4: Electricity demand for heating in Finland, Norway and Sweden

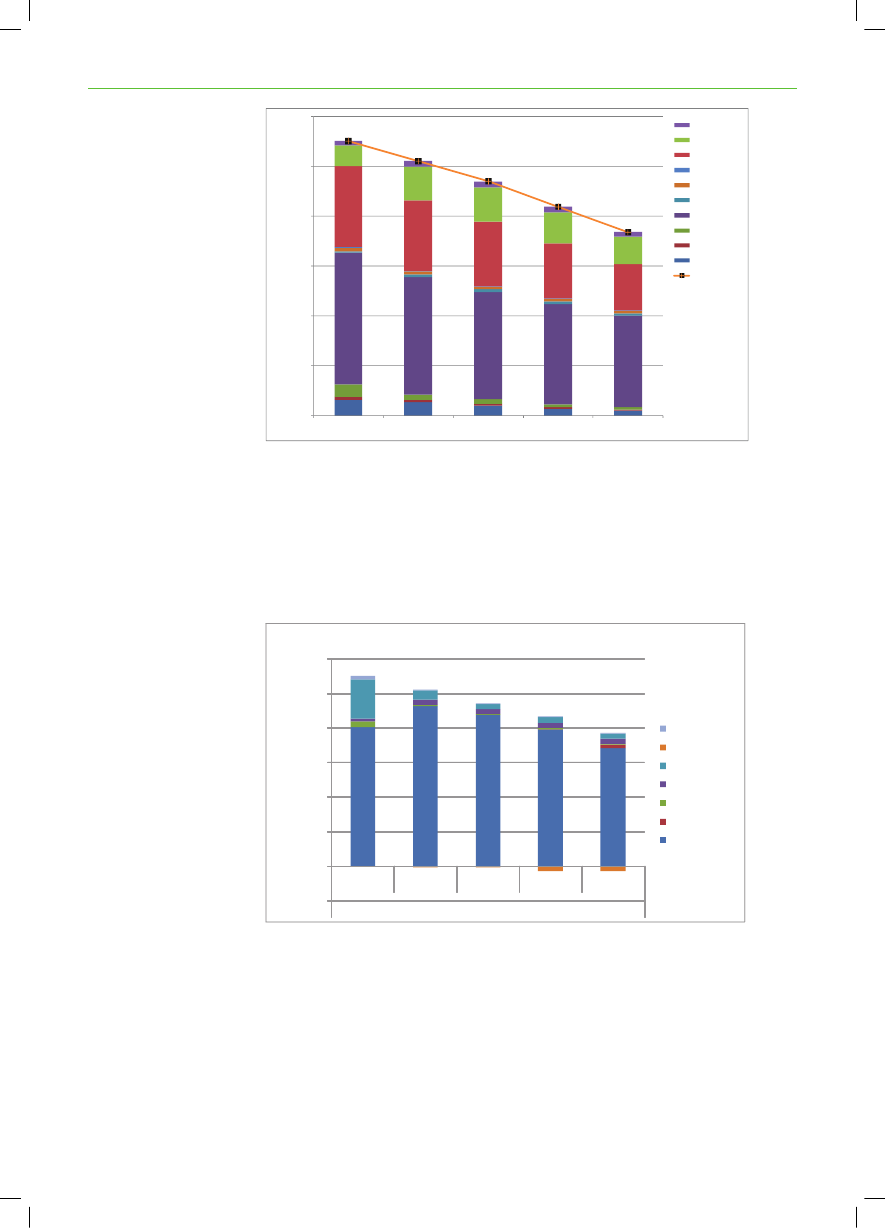

In the “Improved efficiency scenario” it is assumed that the demand for electricityfor heating in Finland, Norway and Sweden is reduced by 50 % towards 2030.When including the additional effort to reduce electricity demand for directelectric heating, the total electricity savings in 2030, in the improved efficiencyscenario are 22 % for the region as a whole compared to the Baseline scenario.In theImproved Efficiency Scenariowind power and coal power are still thepreferred choices by the model, but the level of investments is significantlylower than in the Baseline scenario.Electricity generation by Figure 13 shows the development in total generation in the improved efficiencyscenario. It appears that electricity generation (and hence demand) in this casefuelis more or less constant during the course of time.Electricity genera onElectricity generation1.4001.2001.000800600400200-201020152020Improved efficiency20252030Coal CCSBiogasWindWaterOilshaleBiomassNuclearNatural gasWasteOilCoal and lignite

Figure 13: Total electricity generation (TWh) by fuel for Baseline scenario

The lower demand for electricity, in combination with the targets for increasingthe share of renewable energy, results in an overachievement of the CO2targetsin the period 2015 - 2025. Only by 2030 the target on CO2becomes binding.At that time the marginal cost of reducing CO2emissions is 38 € per ton in thescenario compared to 52 € per ton in the Baseline scenario.This reflects that cheaper abatement measures are put into play at the supplyside in this scenario. By combining demand and supply side measures it will be

TWh

hWT

28

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

possible to achieve stronger CO2targets in the longer term when the most cost-efficient supply side measures will be used up.Mt600S DEWE NRUS IAS500POLANDNORWAYLITHUANIA400LATVIAGERMANYFINLAND300E TONIASDENMARKRegional target200

100

-20102015202020252030

Figure 14: Development in CO2-emissions (Mt) by country in the Improved efficiency scenario

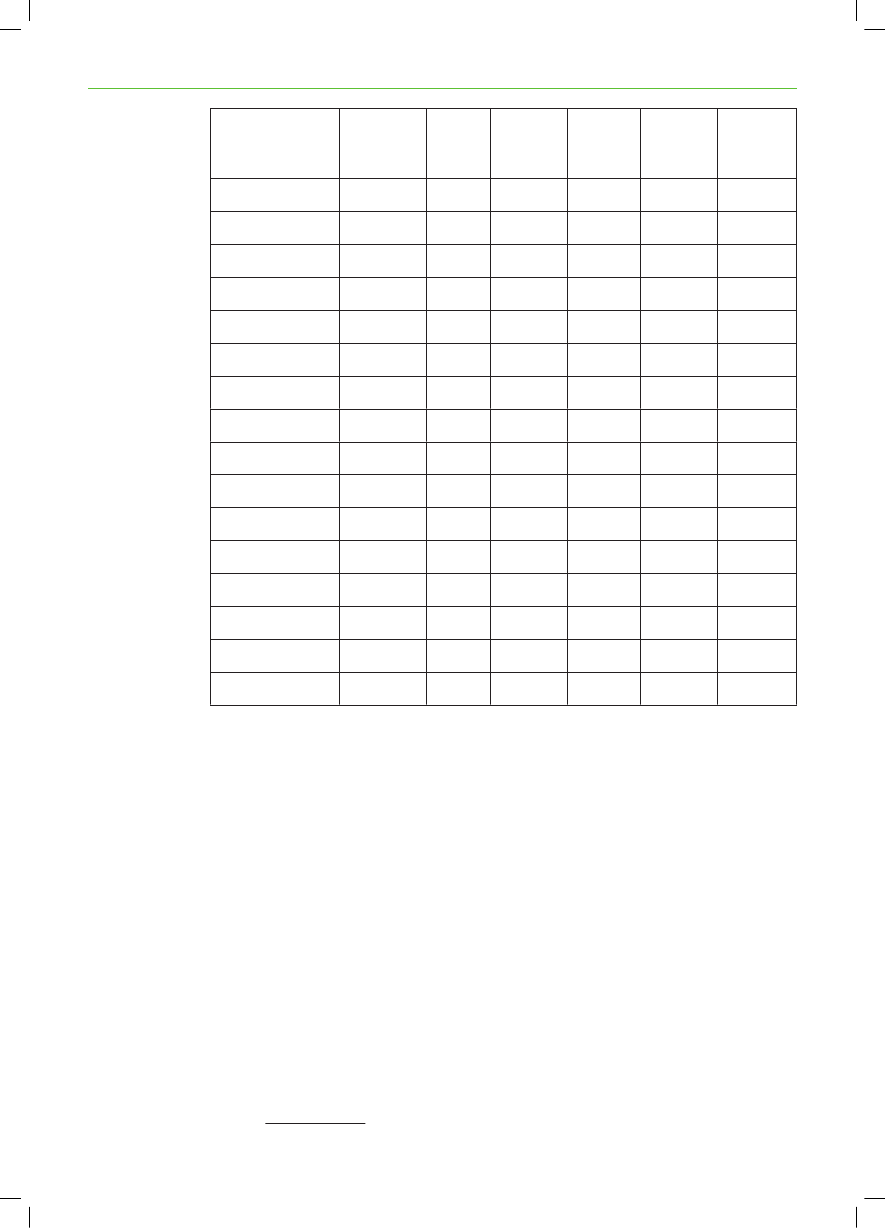

The scenario 30%@COP15The scenario explores a situation where CO2-emissions from the power anddistrict heating sectors are reduced by an additional 10 percentage points in2020. This reflects a situation where an ambitious international agreement isobtained at the Copenhagen Climate Summit in December 2009 committingthe EU Member States to cut their overall CO2-emissions by 30 % in 2020.The target for 2030 is s ll 50 %. The tables below shows accumulated investments inthe 30%@COP15 scenario compared to the baseline.30%@COP15MW20202030Coal andlignite45.99251.473Naturalgas4.0584.694BiomassWindBiogasCoal CCS

2.7806.623

38.10268.364

3.2584.512

3311.196

Table 5: Accumulated Investments in new electricity generation capacity in 30%@COP15 scenario

BaselineMW20202030

Coal andlignite48.26054.195

Naturalgas310541

Biomass3.6535.506

Wind36.67368.710

Biogas3064.455

Coal CCS

13.651

Table 6: Accumulated Investments in new electricity generation capacity the Baseline scenario

The stricter CO2target in 2020 leads to fewer investments in new coal firedpower plants in 2020, but more investments in natural gas fired capacity, windpower and biogas based capacity. The investments in biogas capacity are tosome extent made at the expense of a smaller amount of investments in biomassfired capacity.Biogas is more attractive in the 30%@COP15 scenario, because the negativeCO2-emissions factor of biogas becomes a greater benefit with the tougher CO2-

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

29

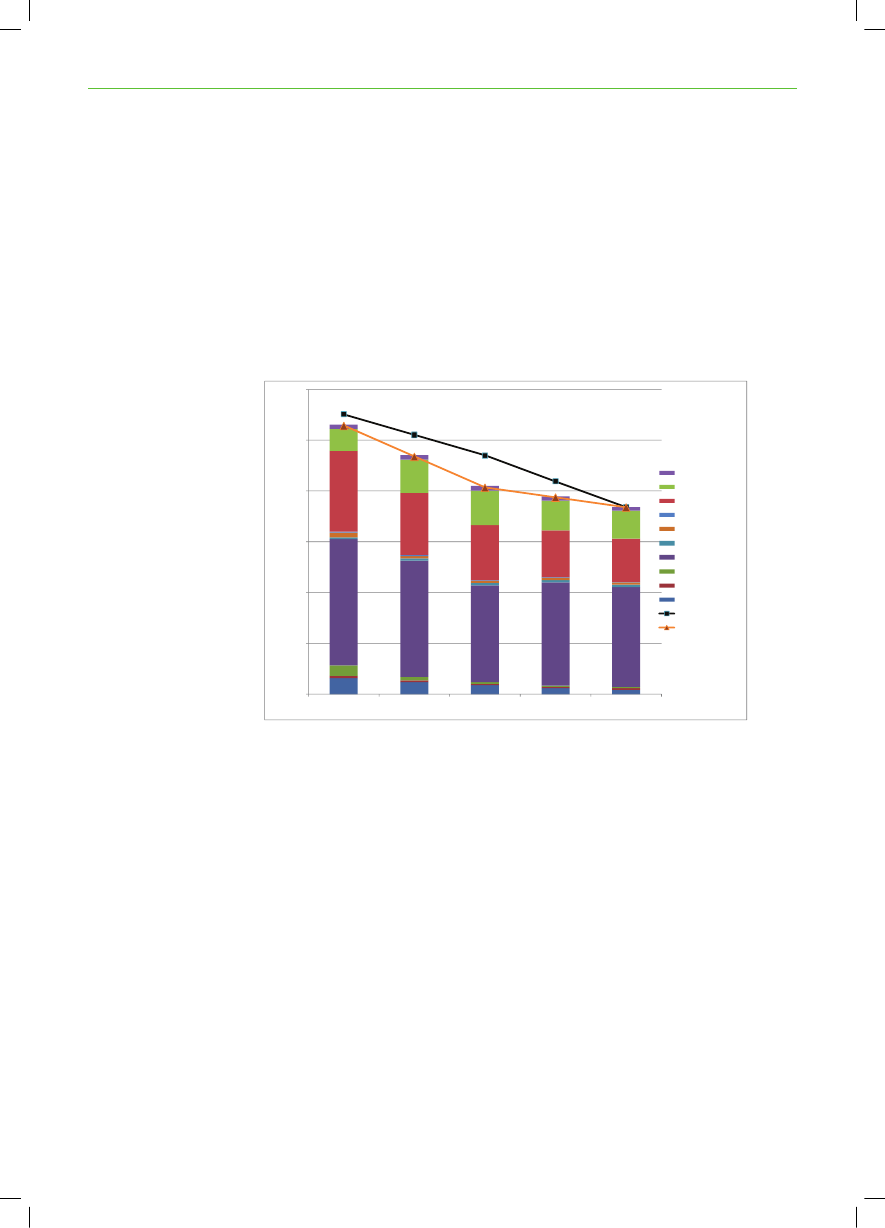

target. This should be viewed in the light of the CO2-price, which is 30 €/tonin the 30%@COP15 scenario in 2020 compared to only 7 €/ton in the Baselinescenario.The cumulated investments by 2030 also differ between the two scenarios eventhough the 2030-target is the same. The main difference is that higher level ofinvestments in natural gas up to 2020 in the 30%@COP15 scenario leads tofewer investments in new coal power and coal power with CCS in the subsequentdecade.CO2-emissionsAs intended, the CO2-emissions in the scenario follow a lower trajectory than inthe Baseline. Figure 44 displays CO2-emissions distributed on countries between2010 and 2030.Mt600

500

S DEWE N400RUS IASPOLANDNORWAYLITHUANIA300LATVIAGERMANYFINLAND200E TONIASDENMARKBaseline target30%@COP15 target100

-20102015202020252030

Figure 15: Development in CO2-emissions (Mt) by country in the scenario 30%@COP15. The scenariospecific CO2targets are shown by the orange line and the CO2target in the baseline by the black line.

Economicconsequences

Electricity generators have their profits increased as the higher CO2-prices leadto higher prices in the electricity markets, whereas the energy costs of electricityconsumers are increased considerably. The total cost for the region of followingthe lower CO2-emission path is estimated to be approx. €16 billion, measuredas net present value (2009).

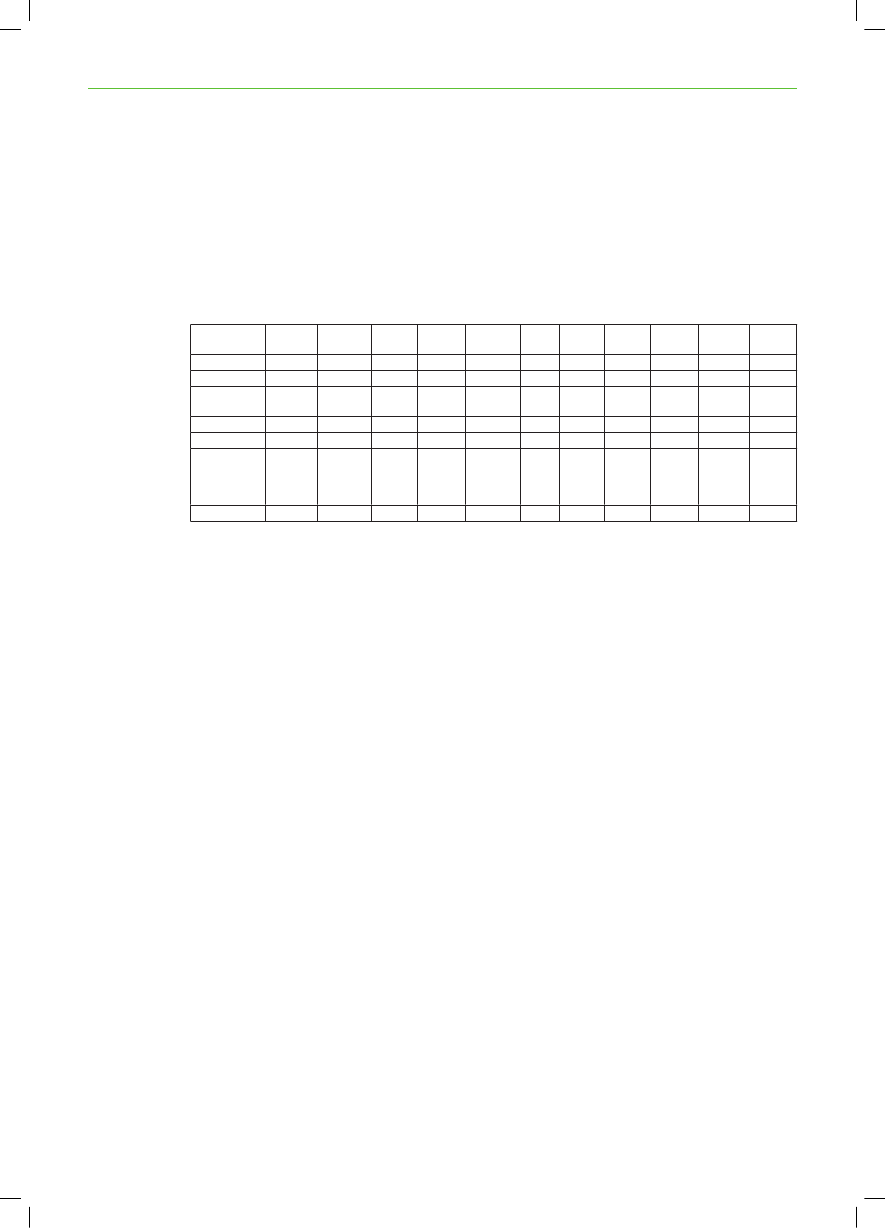

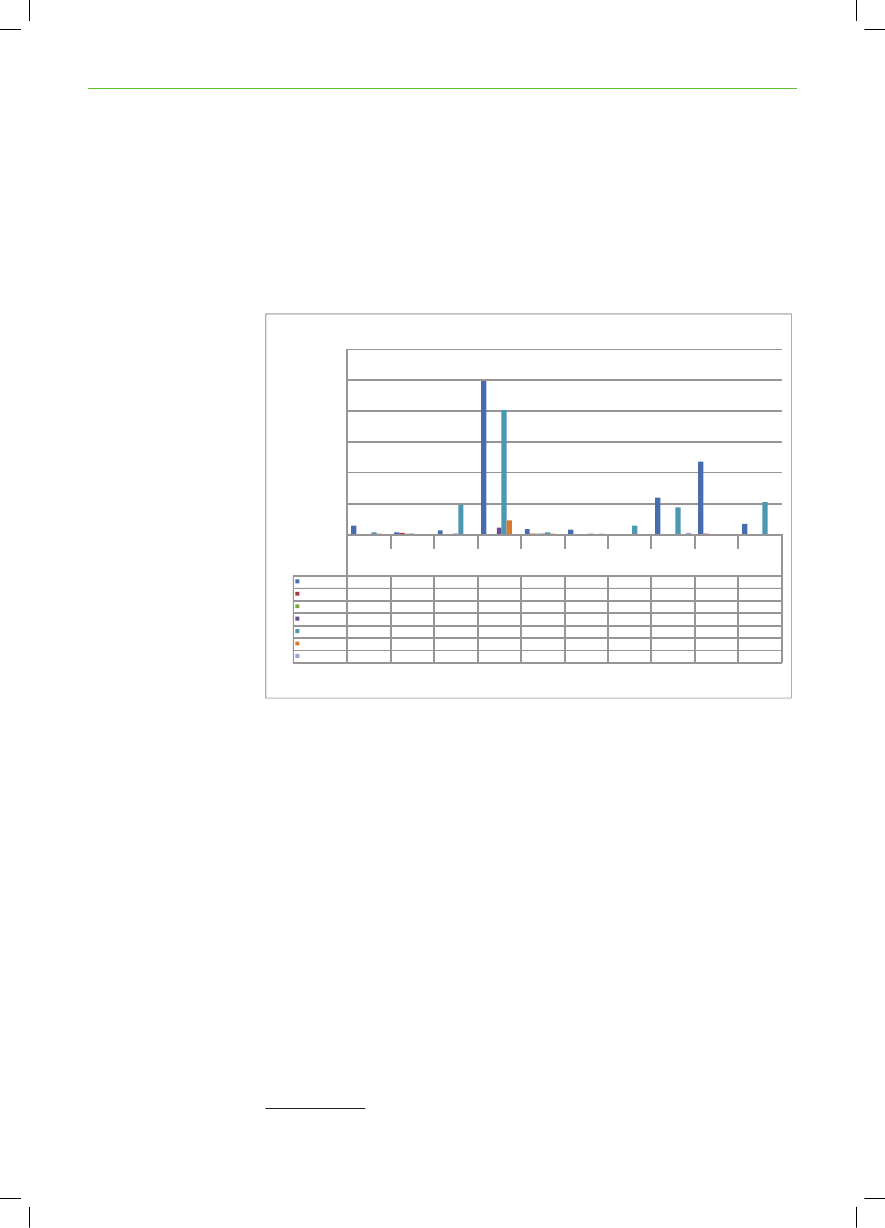

Screening of new interconnectorsThe study considers the existing interconnectors in the Baltic Sea Region. Inaddition, it is assumed that all five prioritized Nordic cross sections have beenestablished by 2015.The model takes into account the most important bottlenecks in the electricitysystems and is able to assess the utility to the electricity market (includingthe different stakeholders in the market) of expanding transmission capacity

30

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

between the different electrical areas. As part of the study a screening has beenmade to identify the most attractive new interconnectors.The simulations indicate that there will be benefits of strengthening theelectricity transmission grid in the region, particularly connections linking thethermal power based systems in Poland and Germany, and the Nordic powersystem dominated by hydro power. Strengthening connections between theBaltic countries and the Nordic countries may also be attractive.Selected results from the screening of new interconnectors:BaselinescenarioIn 2020In 2030Lithuania toSweden M36,000118,000Latvia toSweden M42,000105,000Germany NWto Norway S103,000223,000Germany NWto Denmark W94,000168,000Poland toSweden S50,000271,000Poland toKaliningrad54,000153,000

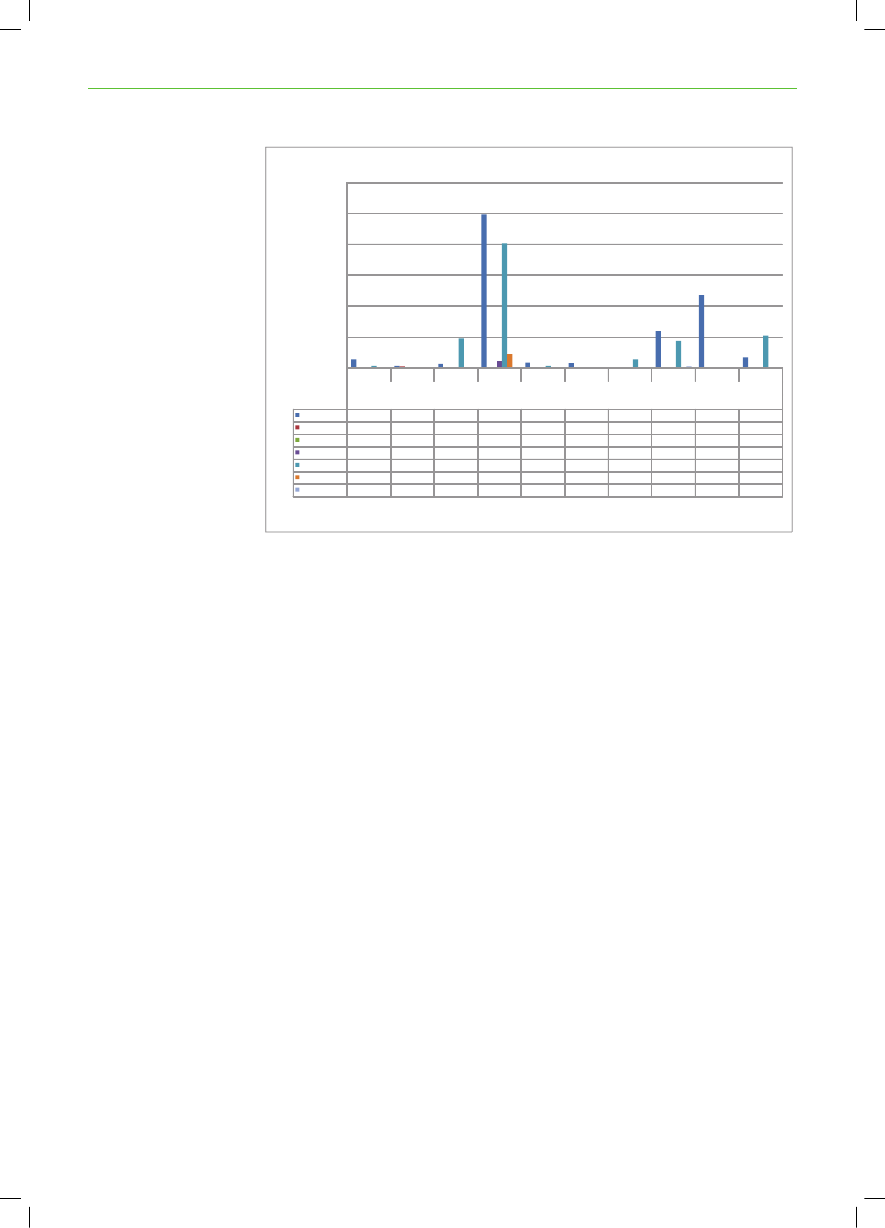

Table 7: Screening of new interconnectors. The table shows the total socio-economic benefit of adding1 MW of transmission capacity between the different transmission areas in the model

These results are based on marginal benefits in the electricity market ofincreasing the capacity on interconnectors linking the different electric areasin the model in the Baseline scenario in 2020 and 2030. It should be noted,that an expansion of the existing transmission capacities in the region has beenincluded in the Baseline scenario (see the Background Report).The value of new interconnectors increases significantly between 2020 and2030.The benefits indicated in the table above should be compared to the capital costsof the connections. These costs are site specific and have not been quantifiedas part of the present study. For comparison it could be mentioned that theannual capital cost of Skagerrak IV linking Denmark West and Norway havebeen estimated to be approx. 35,000 €/MW and for NordBalt linking Lithuaniaand Sweden costs have been projected to be approx. 70,000 €/MW.More comprehensive analyses are required to properly assess the value of newinterconnectors to the general electricity system.

ConclusionsThe alternative policy scenarios indicate some of the advantages of cooperationbetween the countries and between the stakeholders in the Baltic Sea Region:- Regional RE-targets instead of national targets reduce the costs of complyingwith the EU targets for RE in 2020.- Regional planning for new interconnectors and regional development ofenergy markets would ensure the most efficient use of the available energyresources and energy infrastructure in the region.- Joint planning for wind farms would ensure the best utilisation of thewind farms and the transmission lines connecting the wind farms to theelectricity grid.

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

31

- Biomass should be treated as a regional resource and a regional market forbiomass for energy purposes would be an advantage for the whole region.Furthermore the analyses illustrate that a long term planning horizon wouldbe needed in order to ensure sustainable investments in relation to the long-term CO2-targets. This includes the right timing in investments in e.g. coal firedpower plants.Finally the scenario analyses show that savings in the electricity consumptionwould reduce the costs of meeting the CO2target in the region.

1.5 Dialogue with stakeholdersThe dialogue processThe use of scenario technique in strategic policy formulation is very fruitful,particularly if the scenarios are developed via dialogue with the policy makersand the main stakeholders. The scenarios quantify the visions of the politiciansand illustrate how the targets could be fulfilled in the most efficient way.Dialogue with the stakeholders on the energy scene in the Baltic Sea Region hasbeen an important part of the study process. Preliminary results from the studyhave been presented and discussed at a number of occasions, comprising:Energy conference: “Energy and Climate Change: Global Challenges,Regional Solutions”, 21 May 2008 in Warsaw;Meeting of the Baltic Sea Parliamentary Conference’s Working Group onEnergy and Climate Change, 22 May 2008 in Tallinn;Dinner-debate hosted by the Baltic Sea Parliamentary Conference, 20October 2008 in Copenhagen;Meeting of the Joint Platform on Energy and Climate5, 22 October 2008 inCopenhagen;Baltic Development Forum’s Summit, 2 December 2008 in CopenhagenMeeting of the Group of Senior Energy Officials of BASREC, 3 December2008 in Copenhagen;Baltic Sea Region Energy Cooperation (BASREC) Energy Ministersconference, 17 – 18 February 2009 in Copenhagen with the participation ofthe European Commissioner Andris Piebalgs;Meeting of the Baltic Sea Parliamentary Conference’s Working Group onEnergy and Climate Change, 18 May 2009 in Berlin;Energy seminar and joint meeting with the Ministers of Foreign Affairs inthe Baltic Sea Region, 4 June 2009 in Elsinore;Energy workshop, 10 – 11 June 2009 in Kaliningrad.The dialogue process is described in details in Annex 1.5 Representing Baltic Development Forum (BDF), Baltic Sea Parliamentary Committee (BSPC),Council of the Baltic Sea States (CBSS), Union of Baltic Cities (UBC), Baltic Sea StatesSubregional Co-operation (BSSSC), Nordic Council (NC), Nordic Council of Ministers (NCM),CPMR Baltic Sea Commission Energy Workgroup, Baltic Metropoles (BaltMet), Baltic IslandsNetwork B7 and Baltic Assembly (BA).

32

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

Recommendations from stakeholders’ discussionsThis involvement of various stakeholders on different levels contributes to abetter shared understanding of the possibilities and interests in the region.The discussions have resulted in general recommendations on how to developthe Baltic Sea Region as a frontrunner on energy and climate issues:Develop a shared vision ‘A Green Valley of Europe’ in order to mobilize thestrong traditions in the region for public-private co-operation.Establish an energy stakeholders’ forum that includes different cross-border, cross-sector and cross-level actors. Not least the private sectorneeds a larger international platform in order to go beyond small markets.Develop regional projects that could benefit the region as a showcasefor comprehensive and sustainable energy systems including R&D anddemonstration activities.Develop a common interconnector strategy for the region to allow for ahigher level of renewable energy penetration including that from offshorewind power.Launch an action plan for efficient and sustainable heating, involving thelarger cities in the region and the district heating companies.Establish a common regional training program to strengthen the capacitiesin energy planning. Such a program should aim at developing the exchangeof experiences and best practices among officials at local and nationallevels.

1.6 Next stepsAs a key outcome of Phase II, the foundation has been laid for more comprehen-sive analyses and stakeholders’ discussions on the future development of theenergy systems in the Baltic Sea Region.Questions to be answered:The present analyses provide many answers as to how the energy sector inthe region may evolve in the future. However, it also raises new questions,includingHow will the energy systems develop if fuel prices or technology costs evolvedifferently than anticipated? This calls for sensitivity analyses in relation tothe existing analyses.How ambitious targets can be achieved in the region in the long-term if allmeasures are put into play? This calls for an analysis where the scope isexpanded to 2050 in order to show how the region can comply with long-term objectives of the reduction of CO2emissions by 80 %.How can the Nordic countries assist the other countries in the region inmeeting their policy targets? The results indicate that the Nordic countrieshave a potential in becoming large exporters of green electricity to othercountries in the region and potentially to other countries outside the BalticSea region, for example the United K and the Netherlands. How can the

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

33

energy systems and the regulation of the energy markets evolve to enjoy thepossible benefits?Next steps:Improve the quality of Russian data used in the model. A contact has beenestablished with the Energy Forecasting Agency in St. Petersburg.Develop analyses of different concepts for a common interconnection atKriegers Flak and for other regional offshore wind farms.Develop analyses of how to ensure the most efficient use of the heatproduction from the new power plants in the region, including a dialoguewith the central and local decision makers.Evolve the energy markets in the Baltic Sea Region.Evolve the markets for biomass in the Baltic Sea Region.Conducting the study on Energy perspectives for the Baltic Sea Region has beenan ongoing dialogue process. The establishment of the energy database by usingmodeling tools STREAM and Balmorel enables a further dialogue between thestakeholders with possibilities to detail the above-mentioned questions as wellas other questions related to the development of a sustainable energy system inthe Baltic Sea Region.

34

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

2 Scenarios and policy targetsOne Baseline scenario and three alternative policy scenarios are put together toshed light on the future energy situation in the Baltic Sea Region.TheBaseline scenariois developed in order to comply with the EuropeanUnion’s targets of reducing CO2-emissions by 20 % in 2020 and increasing theshare of renewable energy to 20 %.The scenario variations comprise:a scenario withregional targetsfor increasing the share of renewableenergy instead of national targetsanImproved efficiency scenariowhere electricity consumption is expectedto be reduced considerably compared to the baseline projectiona30%@COP15 scenarioshowing a situation where the EU commits itselfto additional CO2-reductions at the COP 15 meeting in December 2009.The means of achieving the policy targets are to a large extent determined by themodelling tool based on a least cost analysis of supply side measures.CO2-targetsThe targets mean that in 2020 CO2-emissions from the electricity generators inthe region should be reduced by 21 % compared to 2005 as this is the generalrequirement for the companies encompassed by the EU Emissions TradingScheme (ETS).The EU ETS covers the majority of fossil fuel power plants in the EU as wellas the energy intensive industry. Because of the significant biomass and windpower potentials in the Baltic Sea Region it is expected that on average theCO2abatement cost in the electricity sector in the region is lower than forcompanies encompassed by the EU ETS. This would give incentives to reduceCO2-emissions in the region beyond the targets. On the other hand, the EU ETSallows companies to import carbon credits from CDM projects6as a means tocomply with the targets. All things considered, it was chosen to apply 21 % as arealistic reduction target for 2020 for the electricity and district heating sectorin the Baltic Sea Region.For 2030 a project target to reduce 50 % of CO2-emissions compared to 1990 wasimplemented. However, compared to 2005 the target is only a 38 % reductionbecause of the significant reduction in CO2-emissions that took place in theEastern part of the region following the transition to democracy after 1990.RE targetsIn addition to the CO2-targets a RE target is included for the electricity sectortowards 2020. In all scenario variations, except “Regional RE target”, the RE6 The Clean Development Mechanism (CDM) is an arrangement under the KyotoProtocol allowing industrialised countries with a greenhouse gas reduction commitment(called Annex A countries) to invest in projects that reduce emissions in developing countriesas an alternative to more expensive emission reductions in their own countries.

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

35

targets are treated as individual targets for each of the countries in the region.The RE targets are set in line with the RE directive endorsed at the summit inDecember 2008.The RE directive provides a target for the share of RE of final energy in eachmember state, but not a separate target for the electricity sector.Renewable energy inthe electricity sectorThe level of renewable energy that will have to be introduced in the electricitysector will, among other things, depend on the economical and technicalopportunities compared to increasing renewables in other sectors such as thetransport sector and the industry. The EU Commission’s renewable energy roadmap7foresees that the penetration of renewable energy in the electricity sectorwill have to increase to 34 % in 2020 in order to comply with a general target of20 % renewable energy in energy consumption. Compared to 2005 this meansa 20 percentage point increase in the share of RE in electricity generation (from14 % in 2005) compared to only a 13 percentage point increase of renewableenergy in overall energy consumption (from 7 % in 2005). In other words, theabsolute share of renewable energy in electricity consumption should increase1.5 times more than the overall share of renewable energy.In the present analyses we chose to operate with a target for the electricity sectorcorresponding to: RE share of electricity in 2005 + 1.5 * required increase in REin overall final energy demand in the directive. As an example, 28 % of electricityconsumed in Denmark in 2005 was supplied from renewable energy. The REdirective requires Denmark to increase its share of RE in final energy demandby 13 percentage point from 17 % in 2005 to 30 % in 2020. Hence, we set the REtarget for the Danish electricity sector at 48 % in 2020 (i.e. 28 % + 1.5 * 13 %).For the Baltic Sea Region as a whole renewable energy electricity correspondedto 26 % of total electricity supply in 2005. For 2020 the target for the region is38 % based on the approach outlined above (see Table 8).Pertaining to the modelling of the energy systems it is assumed that the RE targetsdo not become binding until after 2010. Moreover, to simplify the analyses inthe model, the renewable energy targets do not apply to district heating.Final energy2005 RE share2020 targetIncrease 2005-2020Electricity2005 RE shareExpected increase inelectricity sector2020 targetGermany6%18%12%0%11%18%29%Denmark17%30%13%0%28%20%48%Estonia18%25%7%0%1%11%12%Finland Lithuania Latvia Poland Sweden Norway29%38%10%0%27%14%41%15%23%8%0%4%12%16%35%42%7%0%48%11%59%7%15%8%0%3%12%15%40%49%9%0%54%14%68%60%60%0%0%100%0%100%NWRussia3%0%0%0%19%NANAREGION14%25%11%0%26%15%37%

Table 8: Renewable energy targets. No renewable energy target has been included for North WestRussia; it assumed though that the present renewable generation will continue at least the same leveltowards 2030

In Table 9, the renewable energy targets are expressed in TWh of renewableenergy electricity generation.7 http://www.europa-kommissionen.dk/upload/application/89eba319/03_renewable_energy_roadmap_en.pdf (2009-02-04), see p. 11.

36TWh200520102015202020252030Germany Denmark5710971314016177191821918620Estonia001111

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOSFinland233036414344Lithuania012223Latvia346678Poland3815202325Sweden Norway761188812798135105135108142109147Russia171717171717REGION308386465525546562

Table 9: Renewable energy requirements (TWh of electricity generation) in the Baseline scenario. In thesensitivity scenario with improved energy efficiency the absolute values are lower because the RE targetis measured as a share of final energy consumption.

Norway

Even though Norway is not a part of the EU, the renewable energy directive willalso be applicable to Norway by virtue of the 1994 European Economic Area(EEA) Agreement, to which Norway is a party8. The electricity generation fromrenewables was 108 % of domestic electricity consumption in Norway in 2005,because of a greater than usual inflow to the Norwegian hydro power plants.However, for the present analyses it was chosen to use 100 % RE share in theelectricity as the starting point for Norway and it is assumed that Norway willstay at this level until 2030.The policy framework in Russia is very different compared to the other countriesin the region, which are all members of the European Union, except Norway.Obviously the EU targets on renewable energy and the EU ETS regulation donot apply to Russia. However, Russia is a party to the Kyoto Protocol and thisprovides Russia with incentives to reduce greenhouse gas emissions. Russia’scommitment under the Kyoto Protocol is to stabilise its emissions at 1990 levelsduring the five year period from 2008 to 2012. The economic recession afterthe break-up of the Soviet Union, as well as structural changes to the economy,have resulted in a massive reduction of Russia’s energy-related CO2-emissions.Therefore it is expected that Russia will have considerable surplus of quotas(so-called AAU) in the period from 2008-2012. Potentially, this surplus couldbe exported to other countries under the Kyoto framework. Moreover, studiesshow that Russia has a large cost-effective potential for further reducing energyrelated CO2-emissions mainly through energy-efficiency improvements in arange of industrial activities and end-use sectors9.For North West Russia we have included a target of 10 % CO2reduction in2020 and a 30 % reduction in 2030. These targets assume that an internationalagreement is reached at COP15 in December 2009, which will provide incentivesfor ambitious reductions. Because of the lack of statistical data on CO2emissions,the targets are measured against a model based on the simulation of North WestRussia in 2005 using the available data set.It is assumed that from 2015 a market for CO2-quotas will be formed allowingRussian power and heat producers to trade quotas with their counterparts inthe rest of the Baltic Sea Region.

Russia

8 “Europe agrees on much-anticipated renewable energy deal”, http://www.bellona.org/articles/articles_2008/europe_energy_deal,10/12-20089 http://www.iea.org/textbase/nppdf/free/2006/russiangas2006.pdf, 2009-03-17. IEA, 2006:“Optimising Russian Natural Gas - Reform and Climate Policy”

ENERGY PERSPECTIVES FOR THE BSR SUSTAINABLE ENERGY SCENARIOS

37

2.1 One Baseline scenario and three policyscenariosIn addition to the Baseline scenario a number of scenario variations are prepared.These variations differ in the way policy targets are complied with and whethercommon solutions or national solutions are put in play.By examining the results of the various scenario variations it is possible toexamine the costs and benefits of pursuing different policies. Moreover, thevalue of implementing specific projects in the region can be examined underdifferent scenarios for the future development of the sector.The table below shows the policy targets for the scenario, the variations, aswell as key assumptions with regard to interconnectors and development inelectricity demand.Regional CO2-target forelectricity sector(compared to 2005)20202030- 21 %- 38 %REtarget2020CountryspecificInter-con-nections2005-2030BAUElectricitydemand2005-2030BAU

New Generation2005-2030Modeldecides(-nuclear, hydro)

ScenarioBaselineScenariovariationsRegional REtargetImprovedefficiency30%@COP15

- 21 %- 21 %- 31 %

- 38 %- 38 %- 38 %

RegionalCountryspecificCountryspecific

BAUBAUBAU

BAU- 22 % in2030BAU

Model(-nuclear, hydro)Model(-nuclear, hydro)Model(-nuclear, hydro)

Table 10: Scenarios and variations towards 2030